10Y Yield Extends Rise After Surge In ISM Manufacturing Prices

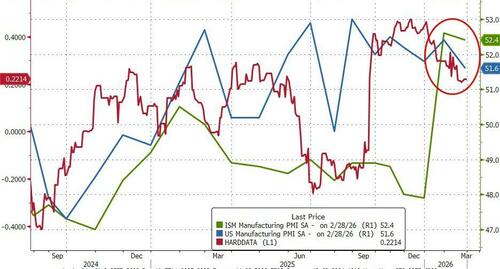

After ISM’s almost unprecedented bounce higher in January, US Manufacturing dipped in February:

S&P Global Manufacturing PMI fell from 52.4 to 51.6 – weakest in seven months

ISM Manufacturing PMI fell from 52.6 to 52.4 (better than expected)

And this is occurring as ‘hard’ data ebbs lower…

{kind=link}

“February saw US manufacturers report the weakest expansion since last July, in a further sign that the overall pace of economic growth has moderated in recent months,” according to Chris Williamson, Chief Business Economist at S&P Global Market Intelligence.

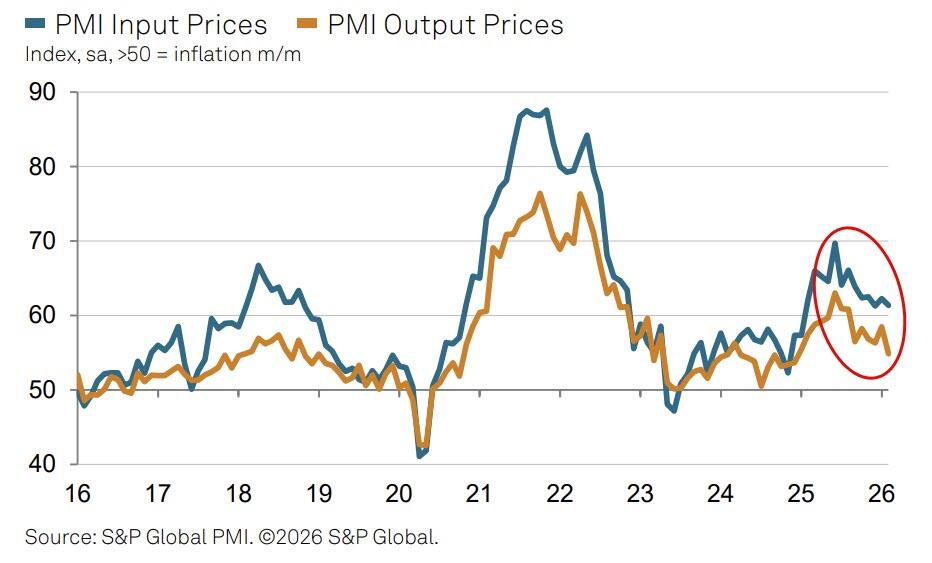

Under the hood we see the usual mixed bag of malarkey in surveys with S&P Global seeing input and output prices declining…

{kind=link}

…but ISM seeing Prices explode higher…

{kind=link}

ISM saw new orders decline, in line with S&P Global’s view:

“Production growth slowed in response to a near-stalling of orders from customers, with exports falling especially sharply. Factory payroll growth was also barely changed, as concern over order book health caused a growing reticence to add to workforce numbers.”

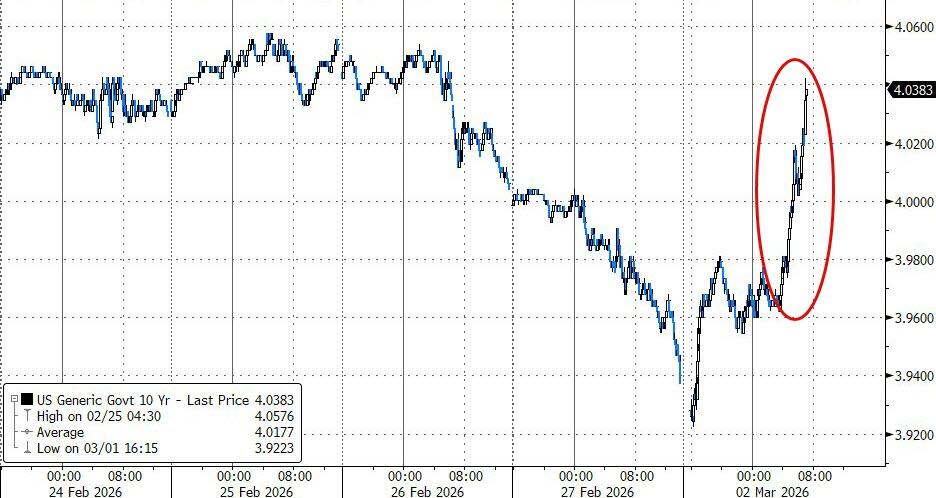

Rising oil prices – on the back of the military actions over the weekend – had already lifted UST yields early on but the surge in ISM prices (despite decline in S&P Global’s) prompted further pain in bonds…

{kind=link}

Businesses were reportedly disrupted by extreme weather, “which has clouded insights into the underlying strength of economic growth and suggests we may see some rebound once the weather clears, and it is encouraging to see manufacturers reporting improved optimism about the outlook.”

However, Williamson notes that uncertainty over the political environment, and the tariff picture in particular, remains a drag on confidence, hiring and investment, which looks likely to persist in the coming months.

Tyler Durden

Mon, 03/02/2026 – 10:07