The Risk Of Too Much Optimism

Authored by Lance Roberts via RealInvestmentAdvice.com,

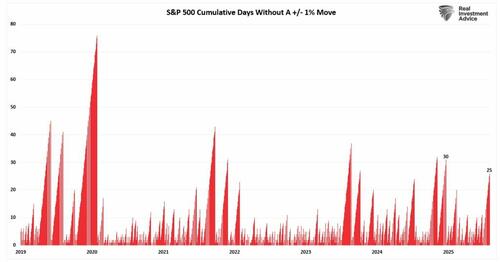

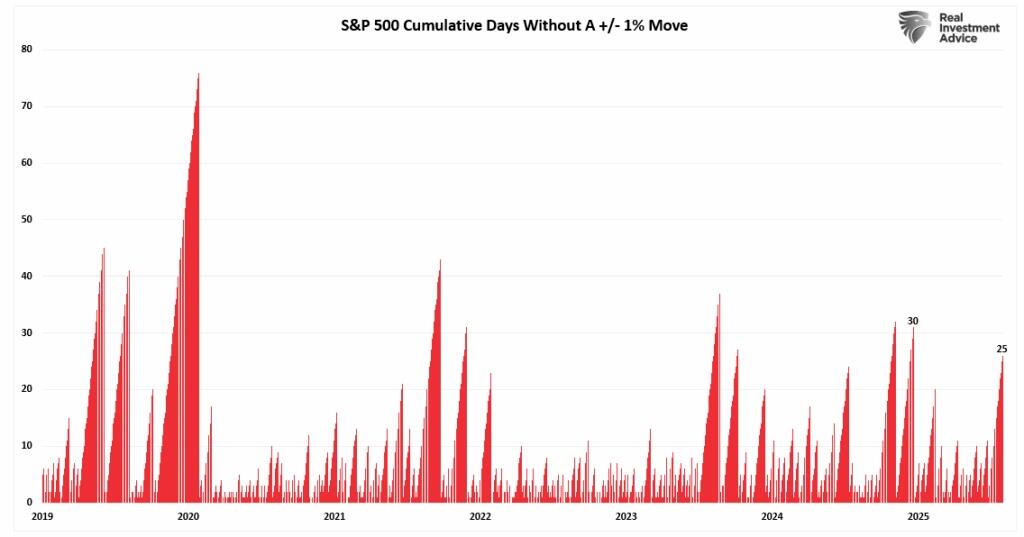

After a long period of “complacency” in the market, volatility finally returned on Friday, dropping more than 1%. As we noted Friday morning, before the market opened:

“While stretches have previously been longer, a consideration of such an event is that low volatility tends to beget high volatility. These “buying stampedes” typically last on average about 15 trading days, so at 25 and counting, we are certainly pushing a more extended duration.”

{kind=link}

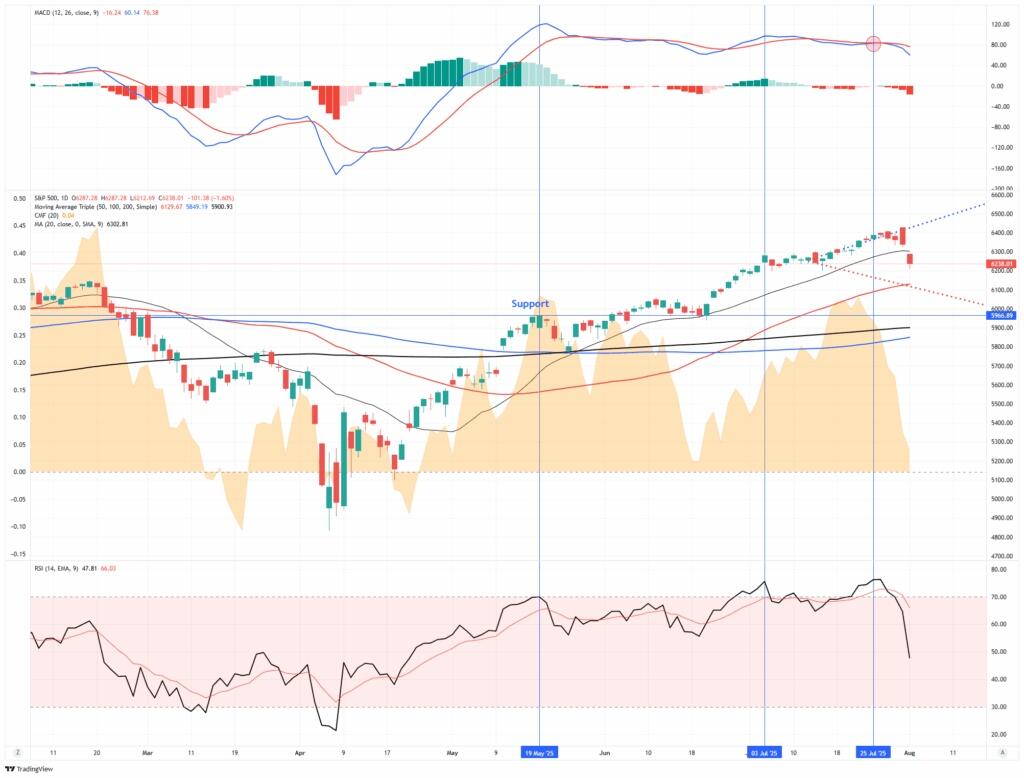

The market’s technical backdrop has shifted notably over the past week as the S&P 500 pulled back sharply from record highs, breaking below its short-term uptrend channel at the 20-DMA. While longer-term moving averages (50- and 200-day) remain positively sloped, the near-term price action reflects growing technical deterioration. The index failed to hold the 6,300 support zone, raising the risk of a deeper correction toward the 50-day moving average near 6,150.

{kind=link}

Momentum indicators are flashing caution. The Relative Strength Index (RSI) has rolled over from overbought levels and is now testing neutral territory (~50 level). MACD has produced a bearish crossover, confirming the loss of upside momentum. Additionally, market breadth has weakened; only ~58% of S&P 500 constituents remain above their 50-day moving averages, down from over 70% two weeks ago. Furthermore, money flows are deteriorating sharply as buyer pressure fades. Also, the heavy selling in small-cap stocks and the sharp rise in volatility (VIX spiking above 17) further signal risk aversion under the surface.

That said, the primary uptrend remains intact, with the market still well above its 200-day moving average, which currently sits near 5,900. Large-cap technology continues to provide index-level support, with earnings momentum in AI-leveraged names mitigating broader weakness. This remains a consolidation within an ongoing uptrend until the S&P 500 breaks below its 50-day.

Outlook: Neutral-to-Bearish. The market appears vulnerable to additional downside pressure soon, especially if upcoming economic data (like ISM Services and productivity reports) disappoint. However, unless selling accelerates through key support at the 50-day moving average, this pullback could ultimately serve as a reset for an overbought market. Investors should remain cautious, tighten stops, and look for stabilization signals before re-engaging aggressively on the long side.

🔑 Key Catalysts Next Week

After last week’s sell‑off driven by weak payrolls and escalating trade policy, investors now focus on a modest U.S. economic slate. Key activity reports, including ISM services, trade balance, factory orders, and productivity, will help refine growth and monetary expectations..

{kind=link}

Overall Risk Outlook: Neutral

With no inflation prints and a lighter U.S. data week, the direction hinges on ISM services and productivity readings.

Unless those surprise meaningfully, markets may remain range-bound, awaiting the following week’s CPI/PPI for stronger directional cues.

💰 Analysts Turn Bullish

Since April, Wall Street has become markedly more optimistic about the future of corporate earnings. Analysts have been revising earnings estimates higher for the second half of 2025 and well into 2026. At first glance, the rationale seems sound. Economic data has remained surprisingly resilient, the labor market hasn’t cracked, and the AI narrative continues to fuel dreams of margin expansion and productivity gains. But under the surface, we should ask whether analysts are getting too far ahead of themselves.

There’s no denying that the current market narrative is powerful. The economy continues to muddle through at a moderate pace. GDP growth hasn’t collapsed, unemployment is still historically low, and inflation, while sticky, hasn’t reaccelerated enough to panic the Fed as tariffs have yet to show any real impact. At least not yet. This has been enough to keep analysts busy revising forward EPS estimates higher. Much of that optimism is concentrated in the usual suspects, large-cap tech, AI-related plays, and discretionary names that have weathered the storm better than expected.

{kind=link}

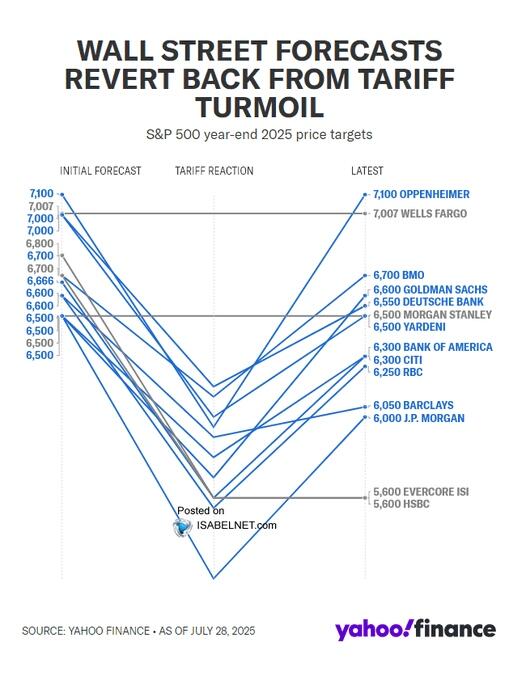

The belief now is that artificial intelligence will unleash a wave of productivity, compress costs, and expand margins for years to come. Add in the hope for rate cuts later this year or early next, and suddenly, we have a recipe for higher valuations. A weaker dollar has also helped multinationals, leading to rosier estimates across global-facing sectors. From this lens, the optimism seems justified. This view has also led to a rapid reversal by Wall Street analysts to push year-end targets for the S&P 500 index higher, with one Wall Street firm upping its year-end price target to 7100.

Oppenheimer Asset Management on Monday raised its year-end target for the S&P 500 index to 7,100, the highest among major Wall Street brokerages, betting on easing trade tensions and strong corporate earnings. Its current target implies an 11.13% upside to the benchmark index’s last close of 6,388.64. Oppenheimer previously set a target of 5,950 for the index.” – Reuters

{kind=link}

How significant would that be?

If the S&P 500 hits 7,100 this year, it would represent a gain of about 21% for 2025, marking a third straight year with a surge of more than 20%. That hasn’t happened since the late 1990s, when the U.S. economy and the stock market boomed.” – Fortune

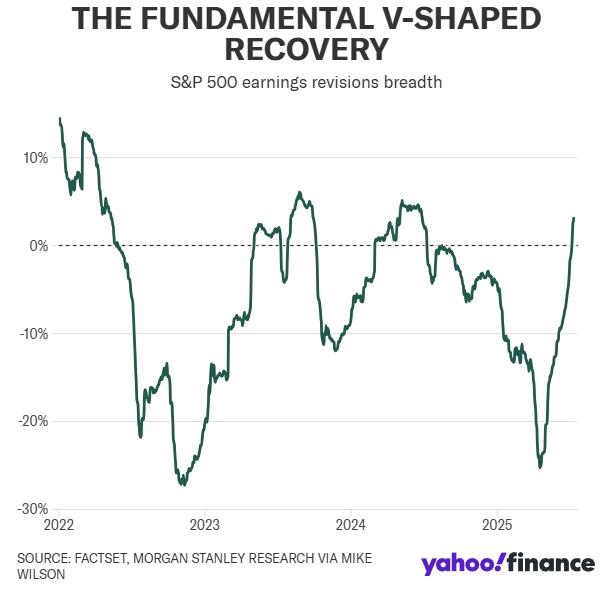

Of course, the late 1990s continue to be a point of discussion, with the more bearish crowd looking for the next market crash. Nonetheless, analysts’ optimism has turned sharply bullish in a very short period. As shown, earnings sentiment not only returned to where it was in December but has surged to new highs for the S&P 500, but not so much for the rest of the world, which brings into question the whole “loss of US exceptionalism” meme.

{kind=link}

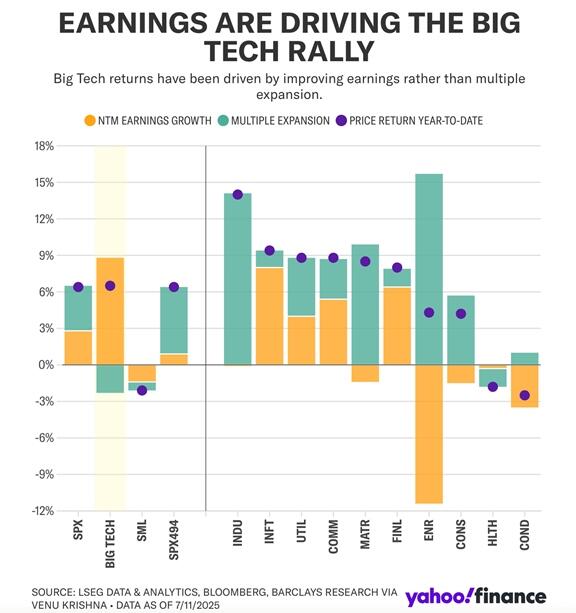

Furthermore, as Yahoo Finance noted on Wednesday, Barclays’ head of US equity strategy, Venu Krishna, shows that Big Tech has been the primary market cohort this year, with earnings growth outperforming its actual price return. Krishna argues that this supports “Big Tech’s” lofty valuations and is a key reason to remain bullish on the sector.

{kind=link}

So, what’s the problem with optimism?

As Bob Farrell once penned: “When all experts agree, something else tends to happen.”

📈 The Risk Of Too Much Optimism

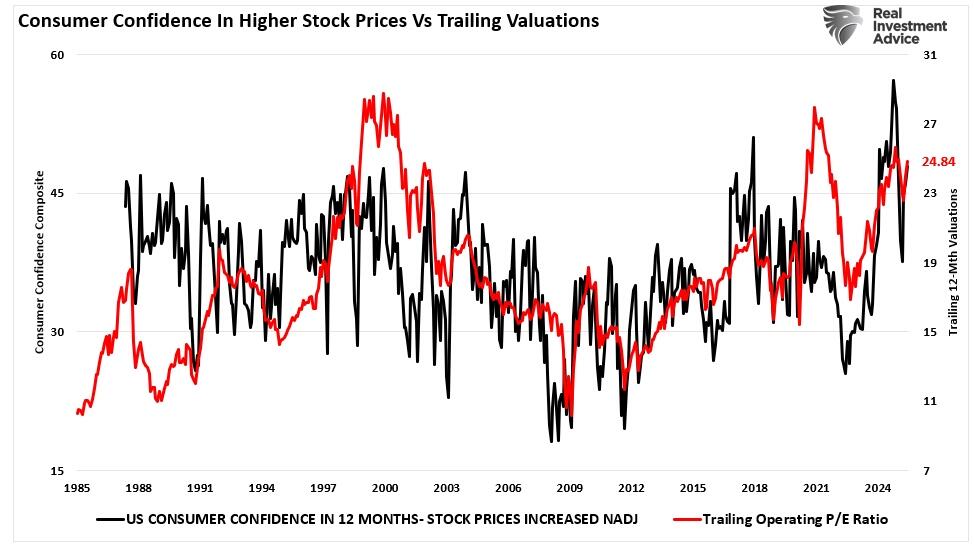

The problem with the current level of optimism is that it is mostly narrative. As noted above, valuations are a “terrible timing indicator.” However, valuations are a very reliable indicator of current sentiment.

{kind=link}

We’ve seen this story before. Analysts are often slow to downgrade estimates when the macro deteriorates, but they’re quick to raise forecasts when sentiment turns. That’s precisely what’s happening now. S&P 500 forward earnings estimates are now growing at double-digit rates for 2025, even though revenue growth expectations remain low single-digits. That math only works if margins expand significantly, something that’s far from guaranteed in an environment of still-elevated input costs and slowing productivity growth.

More troubling is the narrowness of the revisions. While a handful of tech giants drive headline EPS upward, earnings breadth remains poor. Strip out the “Magnificent Seven,” and the earnings picture looks far less exciting. This is classic late-cycle behavior, markets price in perfection while ignoring growing imbalances underneath the surface.

Investors should remember that sentiment shifting too far in one direction tends to overshoot. Despite the current optimism, the risks to earnings are not insignificant.

For one, economic growth is already showing signs of stress. Consumer spending has been propped up by excess savings and credit, both of which are eroding. Credit card delinquencies are rising. Student loan repayments are back. And wage gains have started to slow. If the consumer cracks, corporate revenues will follow.

Input cost pressures haven’t entirely gone away either. While inflation has cooled, labor costs remain sticky, and geopolitical shocks, whether energy markets, supply chains, or foreign conflicts, can reignite margin compression. If inflation persists or reaccelerates, it would prompt the Fed to delay rate cuts or raise rates again. That’s hardly the backdrop for sustained multiple expansion.

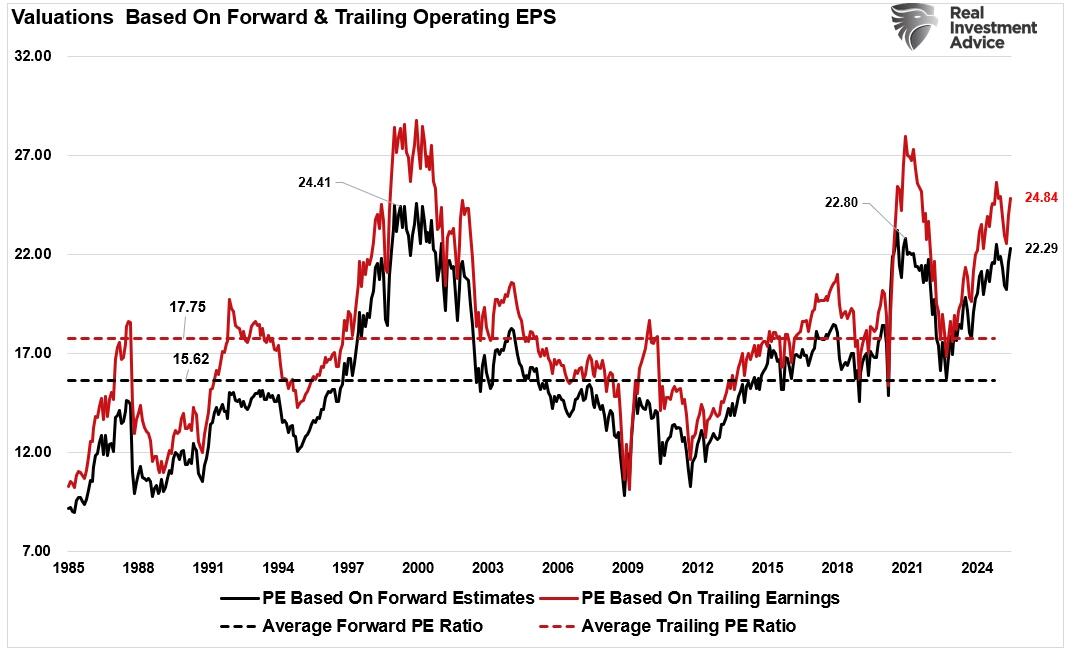

Valuations themselves are stretched. The S&P trades well above its long-term average on forward earnings, which means the bar for earnings surprises is high. And with so much optimism priced into tech, even a modest disappointment could spark sharp reversals. As noted last week,

“…this surge in optimism comes with risks. Notably, valuations, while a terrible timing indicator, have surged to previous highs over the last month as prices are increasing faster than earnings. As is always the case, investors often overlook valuations, but valuations tell us much about sentiment and expectations.”

{kind=link}

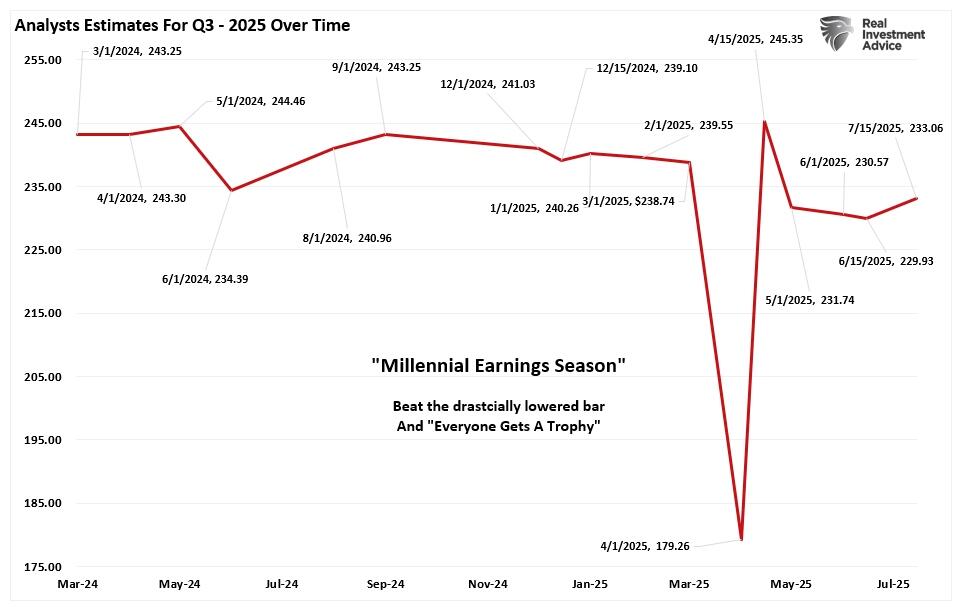

That bullish turn is seen in earnings estimates for Q3, which have jumped over the last two months back to pre-“Liberation Day” tariffs. It should be noted that while those estimates have jumped sharply, and Wall Street analysts are turning more optimistic, the expectation is still $10/share lower than in March 2024.

{kind=link}

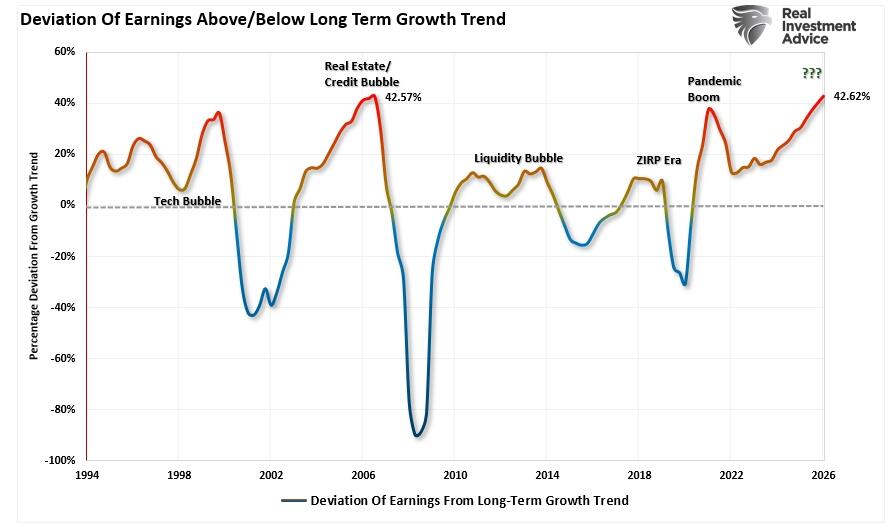

However, even with that “mild” tempering of expectations, earnings’ current deviation from long-term exponential growth (1900-present) is at the highest level on record. Previous deviations from long-term growth trends tended to precede more important reversal events.

{kind=link}

Does this all go “pear-shaped” at some point? The answer is yes. When and what causes it are unknown.

Therefore, as investors, we must realize that we can’t predict the future, but we can control our risks in the present. As we noted last week, limit speculative exposure, tighten risk controls, and don’t chase the market.

As we discussed in “Investing Awards You Will Never Get,”

“Even the most simplistic of risk management strategies can improve returns over time while maintaining a focus on investment goals. Instead of fixating on beating the benchmark, focus on building a portfolio that aligns with your financial goals and personal risk tolerance. Ultimately, true investing success isn’t measured against a broad index. No one will ever give you an award for beating an index from one year to the next. However, they will measure your success by what matters most: whether you achieved your objectives, like securing a comfortable retirement or funding important goals.”

It is crucial to remember that no one will hold Wall Street analysts accountable when they are eventually wrong. However, you will be the one who suffers the consequences.

Ignore the noise, stay disciplined, and remember: no one hands out awards for reckless investing, only consequences.

Tyler Durden

Mon, 08/04/2025 – 06:30