{kind=link}

QUESTION: Your model has projected a recession into 2028. ZeroHedge publishes “If everything is going to be just fine, why are thousands of stores closing all over the country? So far this year, the total amount of retail space that has been permanently closed has surpassed 120 million square feet. We have never seen anything like this before. Store closings spiked during the early days of the pandemic, but in 2025, stores are being permanently shuttered at an even faster pace.”

Do you agree with this? You have also written that in part this is a paradigm shift like Schumpet’s waves of Creative Destruction. Could you address this paradox?

Ronnie

{kind=link}

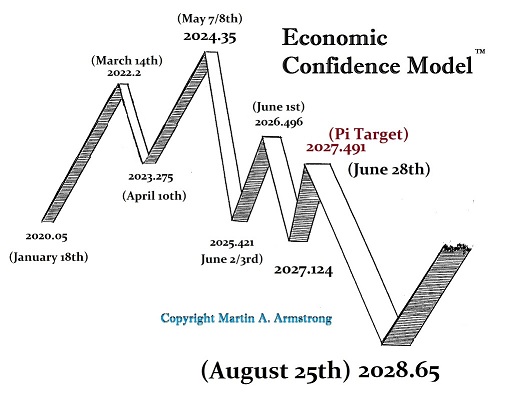

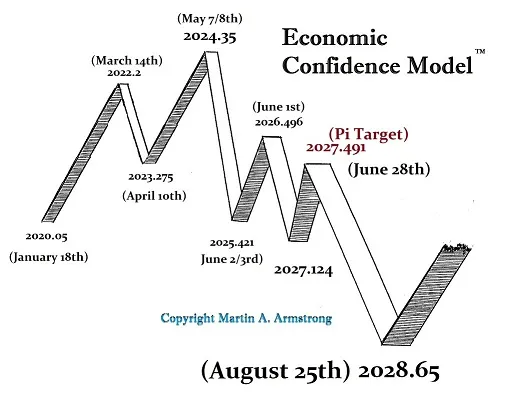

ANSWER: Zero Hedge’s statement is a little misleading, but certainly not intentional. Yes, we have a recessionary trend globally into 2028, which has also been set in motion within the EU by the pounding of war drums. The EU is more likely to experience a DEPRESSION, whereas the USA will have a recessionary atmosphere with STAGFLATION, more like the 1970s, with inflation outpacing GDP growth primarily due to rising costs and wars globally.

{kind=link}

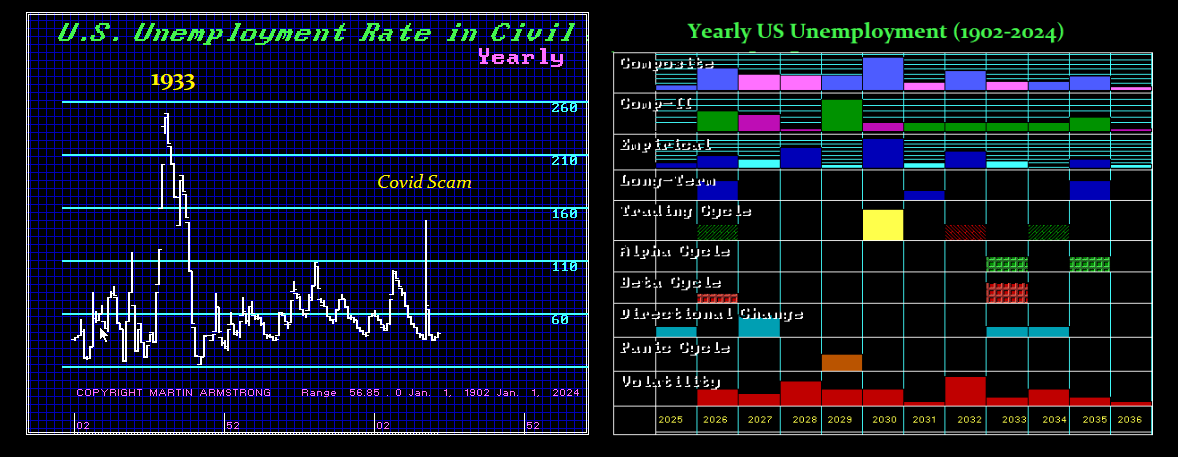

Our computer is demonstrating that volatility in Unemployment will rise from 2026, peaking first in 2028 with a Panic Cycle in 2029. This also confirms our War Cycles for 2026. What we MUST come to grips with is that there is far more to understanding the economy from a single statistic perspective. However, we are also undergoing two significant factors that the classic economic models fail to incorporate, aside from the fact that 99% of the rhetoric and the economic models overlook the leverage in the banking system that creates money outside of the Federal Reserve through lending:

TWO SIGNIFICANT FACTORS OMITTED IN CLASSIC ECONOMIC MODELS

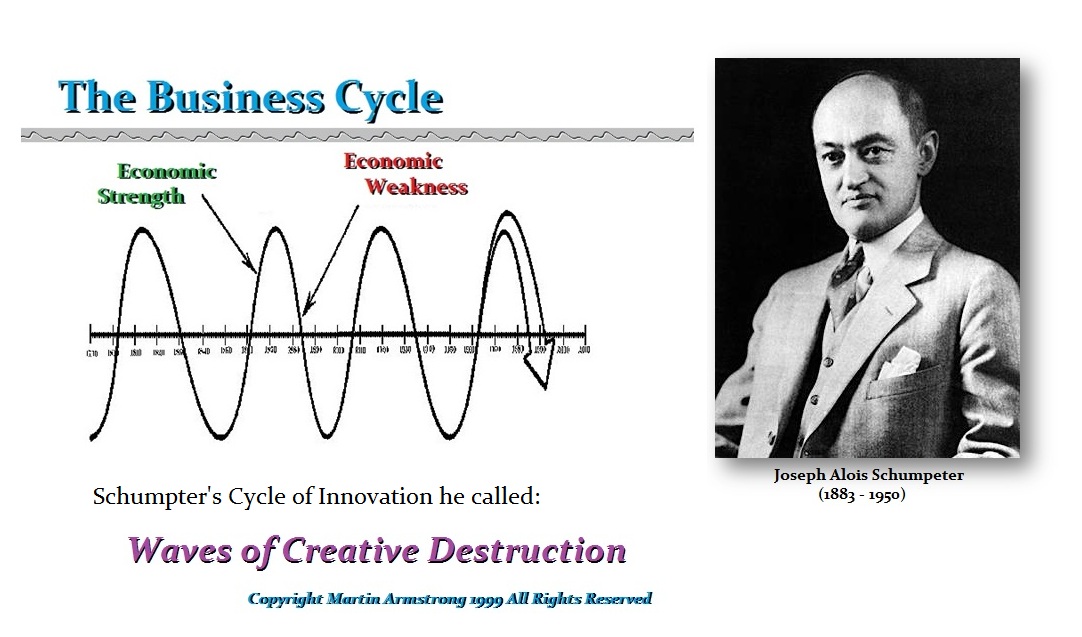

(1) a shift to independent contractors/freelancers thanks to COVID, and (2) a wave of Creative Destruction.

(1) INDEPENDENT CONTRACT:

I stumbled into this issue when the Florida Revenue Department wanted to audit our company. Florida has no income tax, so I was a bit befuddled. I discovered they were auditing to see if we had independent contractors or freelancers who would qualify as a full-time employee, and as such, we were not collecting unemployment taxes, etc. I have NEVER had such an audit – EVER!. So I began to investigate why I was being audited for such an issue. It turned out that the COVID-19 pandemic significantly contributed to the rise in independent contractors and freelancers.

1. Job Losses & Economic Uncertainty

Many traditional employees were laid off or furloughed during lockdowns, pushing them into gig work or freelancing to make ends meet.

Companies downsized and relied more on contract workers to reduce long-term labor costs.

2. Remote Work & Digital Acceleration

The shift to remote work made location-independent freelance roles more viable.

Platforms like Upwork, Fiverr, and TaskRabbit saw increased demand for freelance services (e.g., digital marketing, programming, consulting).

3. Business Adaptations

Small businesses and startups turned to freelancers for flexibility instead of hiring full-time staff.

The “Great Resignation” led many workers to seek autonomy, choosing self-employment over traditional jobs.

4. Government & Policy Influences

Stimulus checks and unemployment benefits (e.g., PPP loans, CARES Act) provided temporary support, allowing some to transition into freelancing.

In some states, labor laws evolved to accommodate gig workers (e.g., California’s Prop 22 for ride-share drivers).

Upwork (2021) reported that 59% of freelancers started during or after COVID.

MBO Partners (2021) found a 34% increase in independent contractors in the U.S. compared to pre-pandemic levels.

OECD data showed a global rise in gig economy participation, especially in delivery (e.g., Uber Eats, DoorDash) and remote freelance roles.

Long-Term Impact:

While some workers returned to traditional jobs post-pandemic, many stayed independent due to flexibility, higher earnings potential, and hybrid work trends. The shift toward a more contract-based workforce is likely here to stay.

States with Higher Unemployment Than Pre-COVID (Feb 2020)

Nevada

Pre-COVID (Feb 2020): 3.7%

Mid-2024: 5.2% (fluctuating due to slower tourism recovery)

Reason: Heavy reliance on hospitality and leisure sectors.

California

Pre-COVID: 3.9%

Mid-2024: 4.8%

Reason: Tech layoffs, high cost of living, and slower rebound in entertainment/hospitality, illegal aliens, and the highest income tax in the nation.

California Income Tax – 13.3% (on income over $1,000,000)

New York

Pre-COVID: 3.7%

Mid-2024: 4.5%

Reason: Slow office sector recovery (NYC), reduced business travel, and Wall Street moving to Florida.

New York Income Tax – 10.9% (on income over $25,000,000)

Illinois

Pre-COVID: 3.4%

Mid-2024: 4.4%

Reason: Outmigration, slower manufacturing recovery.

Illinois Income Tax – 4.95%

New Jersey

Pre-COVID: 3.3%

Mid-2024: 4.3%

Reason: Lingering effects in service sectors, high living costs, abusive taxes, extreme environmental regulations.

New Jersey Income Tax – 10.75% (on income over $1,000,000)

Connecticut

Pre-COVID: 3.5%

Mid-2024: 4.2%

Reason: Slower white-collar job recovery, excessive taxation.

Hawaii

Pre-COVID: 2.4%

Mid-2024: 3.8%

Reason: The economy is highly dependent on Tourism and high taxation

Hawaii Income Tax – 11.0% (on income over $200,000)

States with No Income Tax:

Alaska, Florida, Nevada, South Dakota, Tennessee (repealed investment income tax in 2021), Texas, Washington (but has a capital gains tax over $250,000), Wyoming

States That Have Recovered or Improved

Texas, Florida, Utah, Idaho, and South Carolina have unemployment rates at or below pre-pandemic levels due to strong job growth in tech, manufacturing, and migration trends.

Remote Work Trends: NYC and San Francisco, more than the Sun Belt states, have lost office work. This, in part, has also resulted in the commercial real estate crisis that was part of the objective of the COVID Scam to force people to work from home and stop commuting to save the planet.

Migration Shifts: States like Texas and Florida gained workers, while some Northeast/Midwest states lost population. This is the Great Migration from the BLUE to the RED states. I met people who moved to Florida because their children were becoming suicidal in the Blue States as they shut down sports, and many children thought their dreams in life were over.

Because of that strange audit that still costs you $25,000 in legal and accounting fees for something we did not owe, I began to dig. I found that the rise in independent contractors and freelancers was a side-effect of COVID, in addition to the Great Migration. States were looking for spare change. I would not have been surprised if they didn’t start searching cars for coins left in the ashtrays.

(2) Waves of Creative Destruction:

{kind=link}

{kind=link}

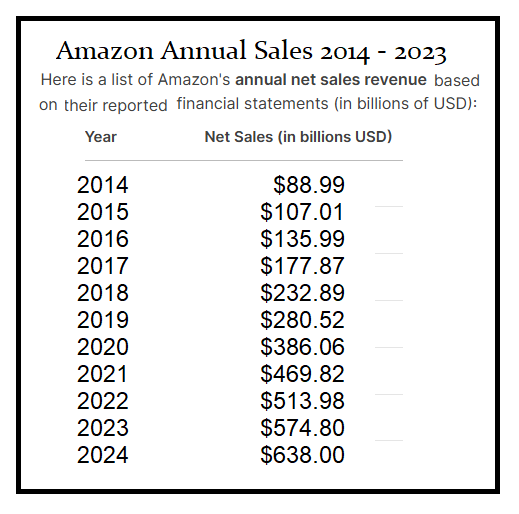

Simultaneously, the plot behind COVID was to create 15-minute cities and have people work from home, virtually ending commuting. What also took place was that people were locked down, and instead of shopping or even going out for dinner, they ordered from Amazon and took out from restaurants. COVID set in motion a new dynamic that the economic models are failing to comprehend. Unemployment can rise while commerce expands. Just look at the sale of Amazon. In the past 10 years, Amazon has expanded by 625%. I know a guy who had a camera shop. I closed after 30 years because he could no longer compete with only sales from Amazon. This is the story nationwide. But COVID was clever. The goal was to save the planet, and that has resulted in a cascade of small stores and even some chains closing stores. Now you have UBER.EATS, Door Dash, etc, to facilitate food being delivered to you within minutes. People closed offices and employees shifted to home, and commercial real estate is going into crisis liquidation. This is all not part of a normal recession – it is a Creative Destruction Wave where unemployment rises, but commerce can expand.

{kind=link}

My firm became the highest paid analyst ever, and we were an institution with some individuals who had a ton of money. Our reports used to go out of telex, and the cost could be up to $75 in telex fees per report, which would go out 3 times a day per currency. That was why I began opening offices around the world so we could bring down the costs for clients by sending one set of reports to our London or Asian offices and they would then redistribute it to the clients in that region. This would reduce costs from $200,000-$300,000 per client just in communication costs. We were Western Union’s biggest client.

{kind=link}

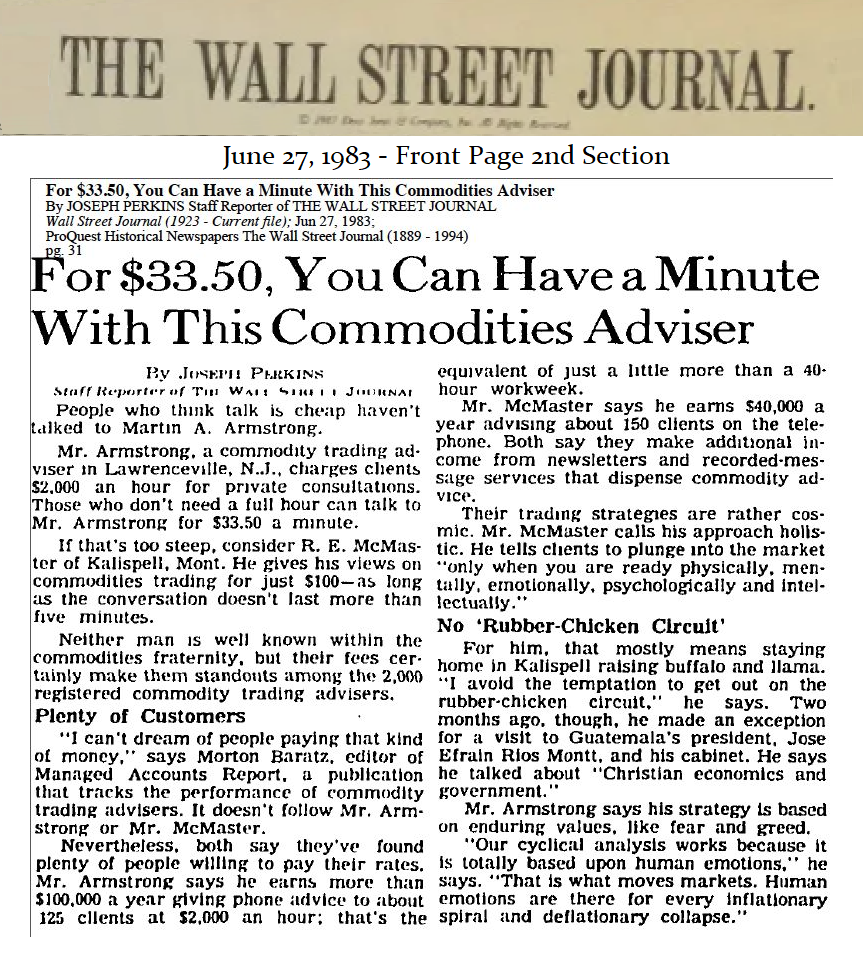

In 1983, the Wall Street Journal wrote a piece that I was charging $2,000 an hour for phone advice. The journalist, after talking to our client who agreed to participate in their review, told him that if I charged $10,000 an hour, they would pay it. He called me back and was stunned. I was advising on a billion-dollar transaction in 1983. $2,000 or $20,000 did not make much difference.

By the mid-to-late 1980s, fax machines were a standard office appliance, peaking in the 1990s before email and digital scanning began replacing them. We started sending reports out by FAX, and that reduced the communication costs dramatically. So personally, I have lived through the technology cycle and saw the price of transmitting a report from $75 to email, which is now basically free. That took the business away from Western Union, and has been a wave of Creative Destruction.

{kind=link}

When the East and West Coasts were connected by train in 1869, the Railroad era put out of business the wagon train industry. The United States expanded and as train tracts were laid around the country, it was first the Railroad Boom which really came to an end with the Panic of 1907.

{kind=link}

The Industrial Revolution expanded, and the Industrialists, led by the auto stocks, drove the 1929 boom. The invention of the combustion engine led to tractors for farmers disproving the theories of Malthus that humanity would starve as population increased. He never understood the cycles of technology. As farmers had tracked tractors, production increased while employment declined.

{kind=link}

The horse & buggy was replaced with automobiles. As they expanded, so did the suburbs expand. Suddenly, people could live in places without trains. The town I grew up in flourished because we had a train station, which enabled people to buy land and move out of the cities. The town I grew up in expanded further from the train station with the automobile.

{kind=link}

The first commercial airline was the St. Petersburg–Tampa Airboat Line, which began operations on January 1, 1914. They flew a Benoist XIV, a small flying boat (seaplane). The distance was only 23 miles (37KM). It reduced the travel time from 2+ hours by boat or car to just 23 minutes.

{kind=link}

Therefore, while the ECM has turned down, these types of forecasts that focus on one aspect are always wrong. Economists omitted from their models not only the creation of money but the banking sector by lending money, which leverages the money supply. Those who believe shutting down the Fed and handing money creation to the Treasury will cure inflation do not know their monetary history. The discovery of gold in the New World flooded Europe and resulted in massive inflation. during the 15th-16th centuries. The gold-silver ratio has always fluctuated because the discovery of silver relative to gold has never been confined simultaneously.

{kind=link}

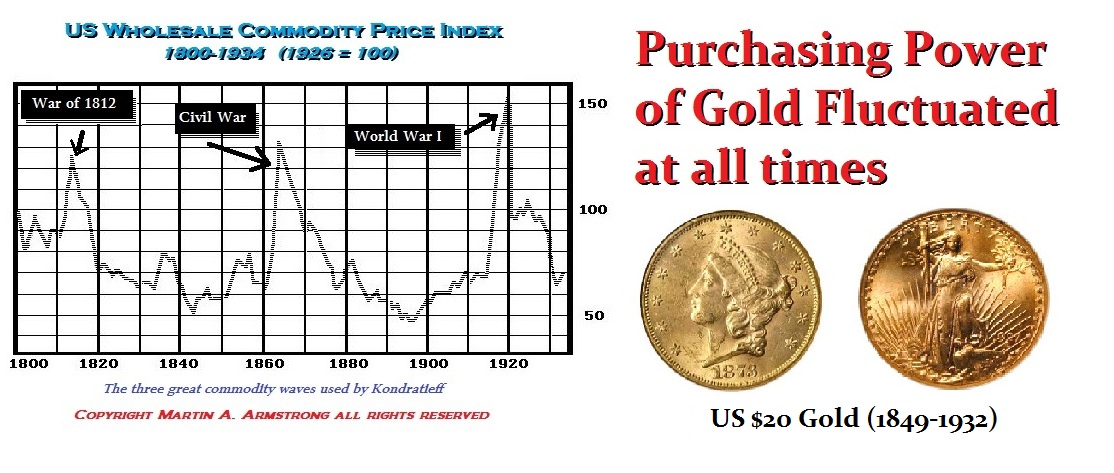

The vast gold discoveries in California, Australia, and Alaska created waves of inflation. Just because gold is money does NOT eliminate inflation. All the nonsense oh paper currency is FIAT and that is the problem, is just stupid sophistry. It has NEVER mattered what the money is from gold, cowrie shells in China, to sheep skins, Bronze, or cattle.

{kind=link}

Assets rise in value regardless of what the money might be, and the purchasing power of money declines even when it has been gold. This is the business cycle that DID NOT simply appear when paper money started in the USA.

{kind=link}

The economic models are DOMESTIC because economists want a job to advise governments that they are all-powerful if they listen to them. I am sorry. As a trader, you lose your shirt, pants, your house, and your family if you trade based on economic theories. They are entirely useless. They never consider external factors.

(1) All banks create money with loans (I deposit $100 and they lend you $100, and both our accounts reflect a money supply of $100)

(2) They have never been able to account for sudden increases in the money supply that have been caused by:

(a) new gold or silver discovery

(b) A war in another region diverted capital seeking shelter as European money flowed to the US for WWI & WWII

(c) Capital concentration where foreign capital sees a profit in another economy driven by currency values

(d) Capital flight from your economy based upon a sudden collapse in confidence, be it mismanagement or war

(3) Economic technological evolution (trains, cars, airplanes, internet, etc…)

{kind=link}

This is not even a complete list. I only met one academic who thought out of the box, and that was Milton Friedman. Milton came to listen to me at a trading convention in Chicago. I was explaining capital flows and currencies. When I was finished, Milton stepped forward to shake my hand and said I was doing what he had only dreamed about. We became friends, and then I understood what he was talking about. He had theories that a floating exchange rate system would impose checks and balances upon the fiscal policies of the government. He had written that theory down in 1953.

{kind=link}

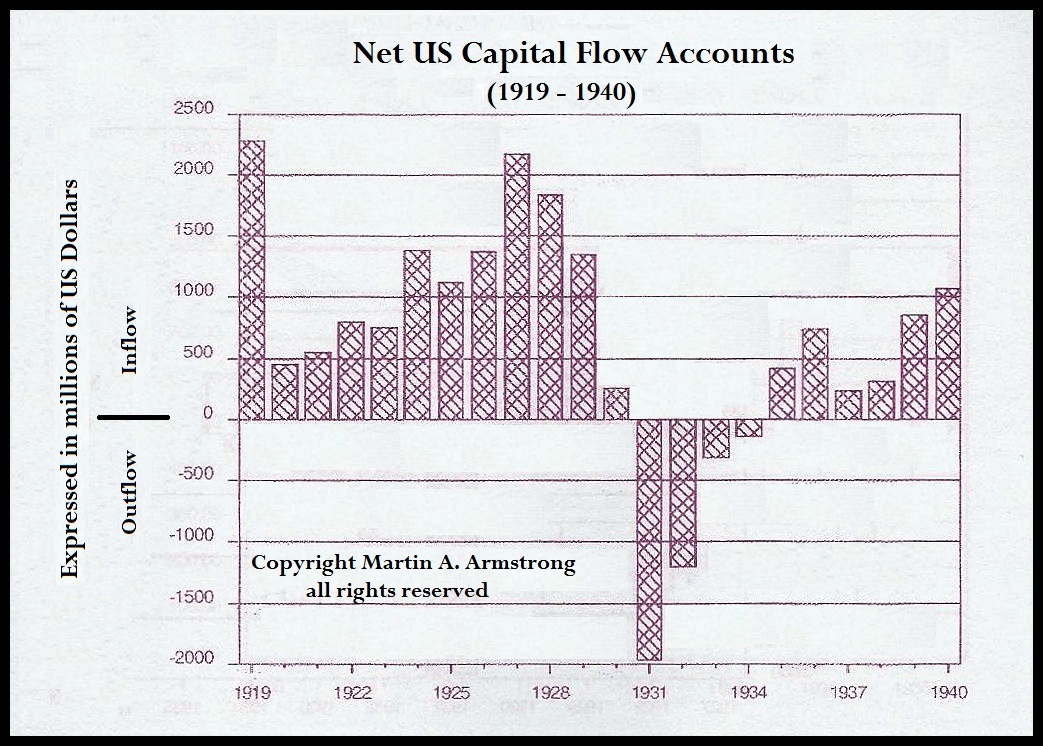

While I explained the Great Depression and the Sovereign Debt Defaults in 1931 in Europe, even Canada suspended debt payments, you can see the capital was taken back to its home countries, ending the Roaring ’20s. Everyone politically blamed Hoover and then tariffs, but nobody understood international capital flows.

{kind=link}

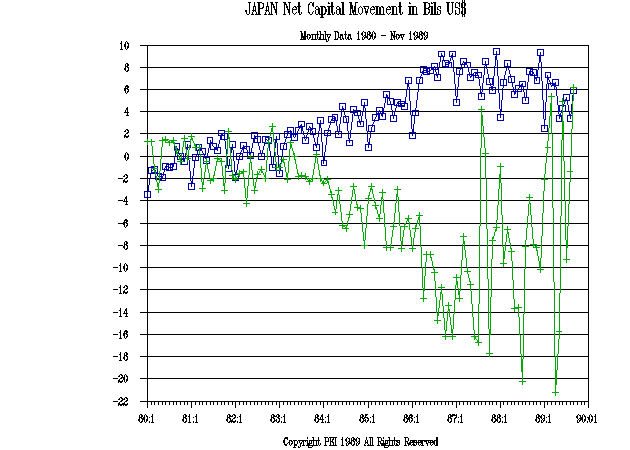

I explained HOW the G5 intentionally lowered the value of the dollar by 40% to reduce the trade deficit. As idiots, they never understood that doing that means you were devaluing everything held by a foreigner. Japan owned up to 30% of the US National Debt, and they dumped it as the capital flows revealed.

{kind=link}

It was World War I and World War II that made the US the financial capital of the world because all the gold fled to the USA during the wars. There was ABSOLUTELY no political decision made by any domestic politician that stood up and proposed making the US become the new capital for finance, taking that title from Britain.

{kind=link}

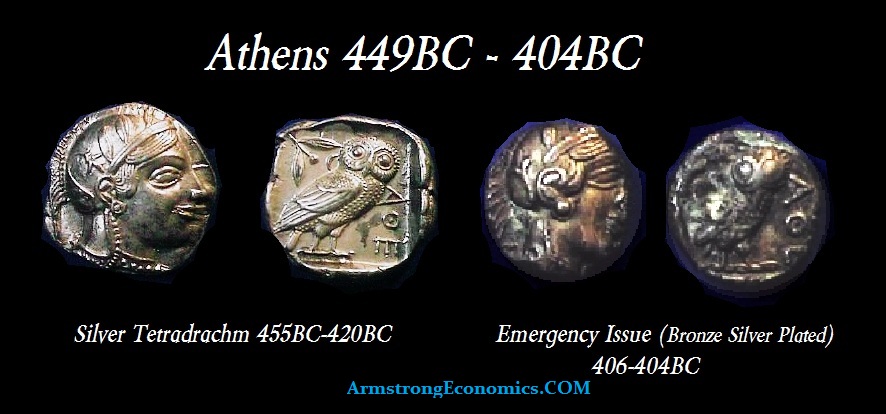

There is absolutely no historical evidence that repeated war have ever benefited any country. War destroys the economy, as evidenced by Lydia, which invented coinage and fought Persia. Athens became the financial capital of the world after the Battle of Marathon, and they were compelled to debase and lost in the Peloponnesian War to Sparta.

{kind=link}

The favorite phase in economics is: “Assuming all things remain equal.” Of course, that never happens.

{kind=link}

We have the socialists always claiming the problem is wealth disparity. They hate people who have more than they do – that’s all. Both China and Russia tried Marxism’s wealth disparity solution – confiscate all private wealth to create material equality. The people learned that you had no right to be individual. When everyone was equal, and they needed a floor swept, you were next in line – here is your broom.