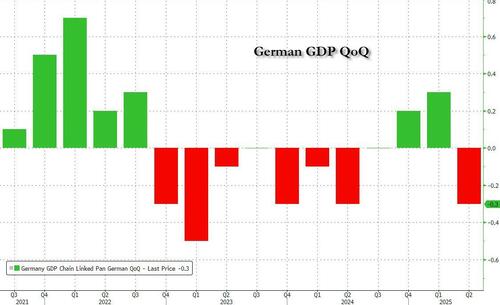

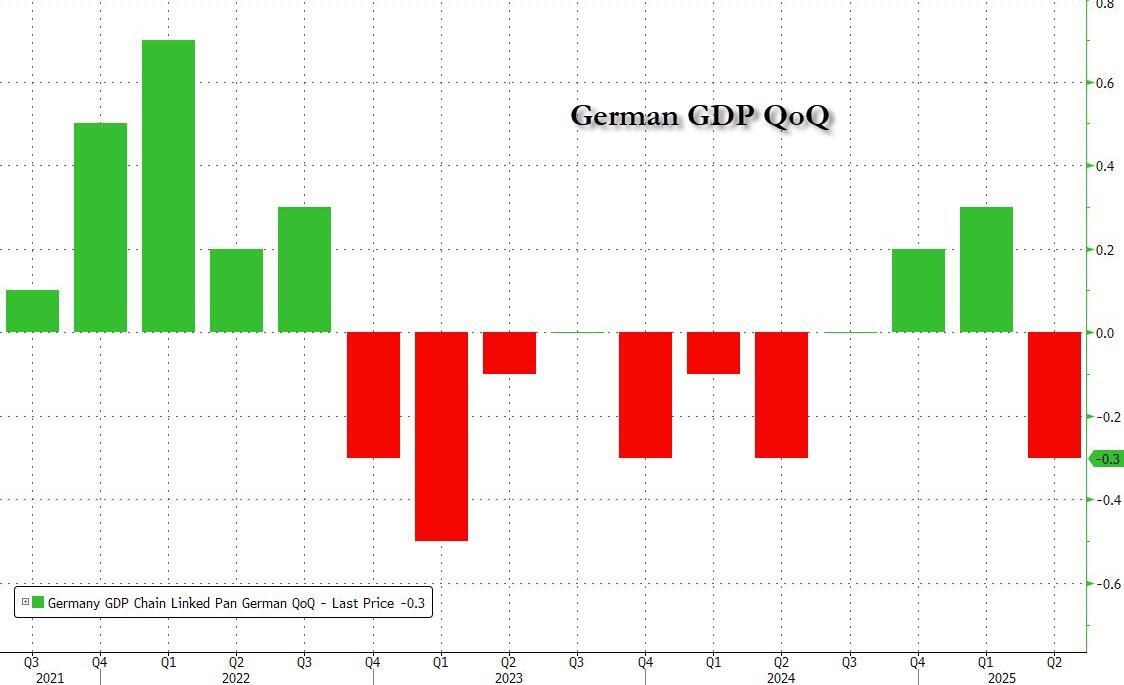

German Economy Shows No Signs Of Emerging From Recession

By Thomas Kolbe

Germany’s Mittelstand Collapses as “Investment Booster” Flops

The German economy shows no signs of emerging from recession. The monthly Mittelstand index, compiled by the consulting firm DATEV, confirms that the downturn continues unabated. The crisis has spread across virtually all sectors of the economy.

{kind=link}

The recovery announced by the German government remains a summer fantasy. Data collected in July through DATEV’s monthly survey of small and medium-sized enterprises (SMEs) describes the economic situation as extremely fragile—with no upturn in sight. SMEs saw revenues fall by 1.7 percent year-on-year in July. The corresponding business cycle index dropped, seasonally and calendar adjusted, to 91.9 points—firmly anchored in recession territory.

No Sector Spared

Sectors traditionally dominated by the Mittelstand, such as hospitality, have been hit especially hard. Revenues in the sector fell 4 percent, while construction contracted again by 2 percent. “With the absence of a summer revival, the situation in the hospitality industry continues to deteriorate,” said Prof. Dr. Robert Mayr, CEO of DATEV eG. “Hopes now rest on a more positive August.” Hope, however, is no substitute for strategy—and no good advisor amid the worsening conditions for SMEs.

Only retail managed a slight reprieve, posting a meager 0.1 percent revenue increase. That uptick likely reflects sharply rising wages, up 4 percent. But this brings little relief. Businesses are caught in a squeeze: a deteriorating business environment on one side and rising wage costs in a broader economic setting marked by stagnating or slightly declining productivity.

Investment Drought and Capital Flight

Germany is underinvested, losing foreign direct investment while labor costs rise. The consequence is job cuts. DATEV data confirm this trend, especially among small firms, which reduced headcount by 3.4 percent year-on-year. Overall employment declined by 0.3 percent, translating into about 125,000 jobs lost over the past 12 months—70,000 of them in industry, the backbone of Germany’s economy.

The DATEV index offers a granular, real-time look into the engine room of the German economy. The data are not government estimates or Bundesbank approximations but anonymized, aggregated real-time figures drawn from VAT filings and payroll accounts, covering over one million companies and eight million employees.

A Realistic Look at a Deep Recession

The numbers confirm that after contracting by 0.9 percent in 2023 and 0.5 percent last year, the German economy is set to slip even deeper this year. To assess the real trajectory, one must strip out the artificial boost from government spending. With a 3.5 percent deficit and a public-sector share of 50 percent of GDP, the private-sector recession looks dramatically worse—somewhere between –4 and –5 percent. Hospitality’s 4 percent drop lines up almost perfectly with this estimate.

Consumers, meanwhile, remain deeply unsettled. Despite rising wages, they are holding back on spending. Everyone seems to sense that this is just the beginning of a recession, one that could end with a full-blown employment crisis.

The “Investment Booster” Is a Dud

Germany’s structural problems are well known and now manifest. The old business model—cheap energy (much of it from Russia), export-driven growth fueled by the weak euro—belongs to the past. The government’s much-publicized “investment booster” will not jolt the country out of its economic paralysis.

The planned relief amounts to just €7 billion per year—spread across accelerated depreciation rules for machinery and buildings, and token tax cuts that won’t even take effect until 2028. Compare that with the over €100 billion German firms pay annually in corporate and trade taxes—before counting social charges and bureaucracy costs in the hundreds of billions.

The result: the booster is marginal, a drop in the ocean. Instead of real tax cuts or structural reforms, companies get a temporary gimmick. Politicians sell a cosmetic fix as a breakthrough—but in reality, the investment brake remains fully engaged.

* * *

About the author: Thomas Kolbe, a German graduate economist, has worked for over 25 years as a journalist and media producer for clients from various industries and business associations. As a publicist, he focuses on economic processes and observes geopolitical events from the perspective of the capital markets. His publications follow a philosophy that focuses on the individual and their right to self-determination.

Tyler Durden

Mon, 08/25/2025 – 02:00