Fed’s Favorite Inflation Indicator Shows No Signs Of Runaway Tariff Costs

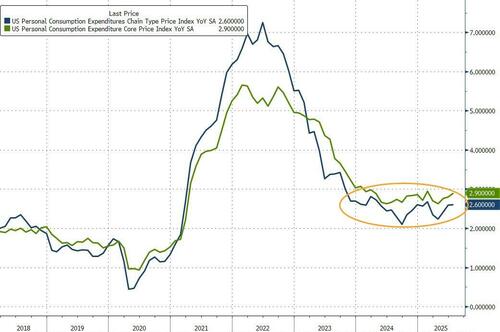

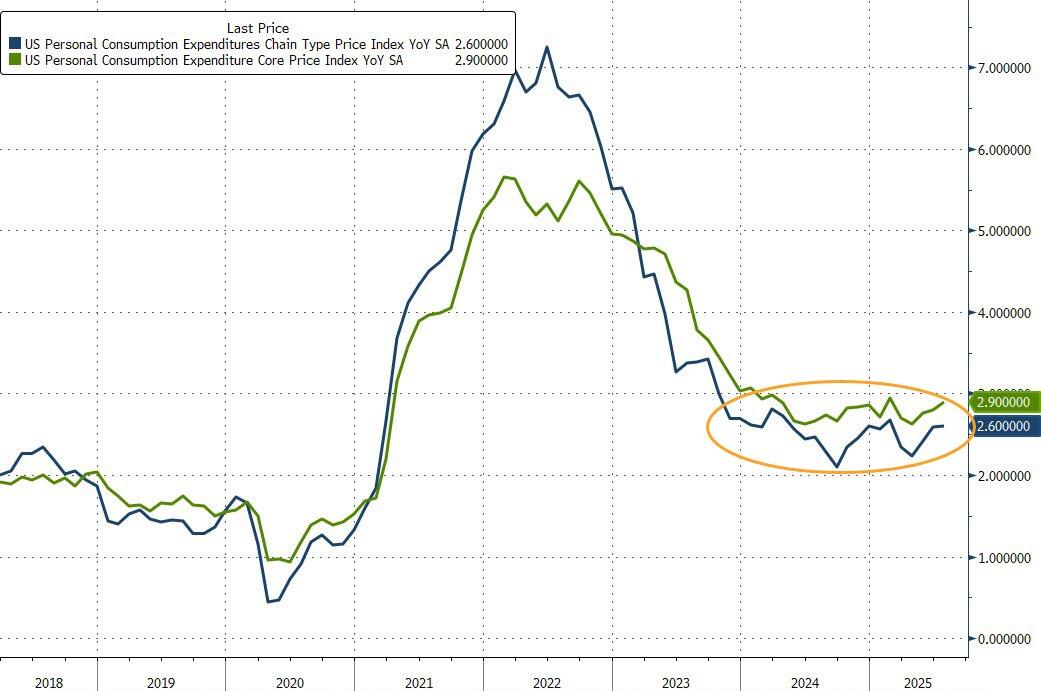

Having ticked higher in June, analysts expected headline PCE to be steady at +2.6% YoY in July and Core PCE – The Fed’s favorite indicator – to rise from +2.8% to +2.9% YoY… and the numbers all came in right in line with expectations.

‘As Expected’ is the them of this morning’s data with headline and Core PCE both matching expectations and staying in the same range they have been in for two years… not exactly the Trump Tariff terror future that was predicted…

{kind=link}

Source: Bloomberg

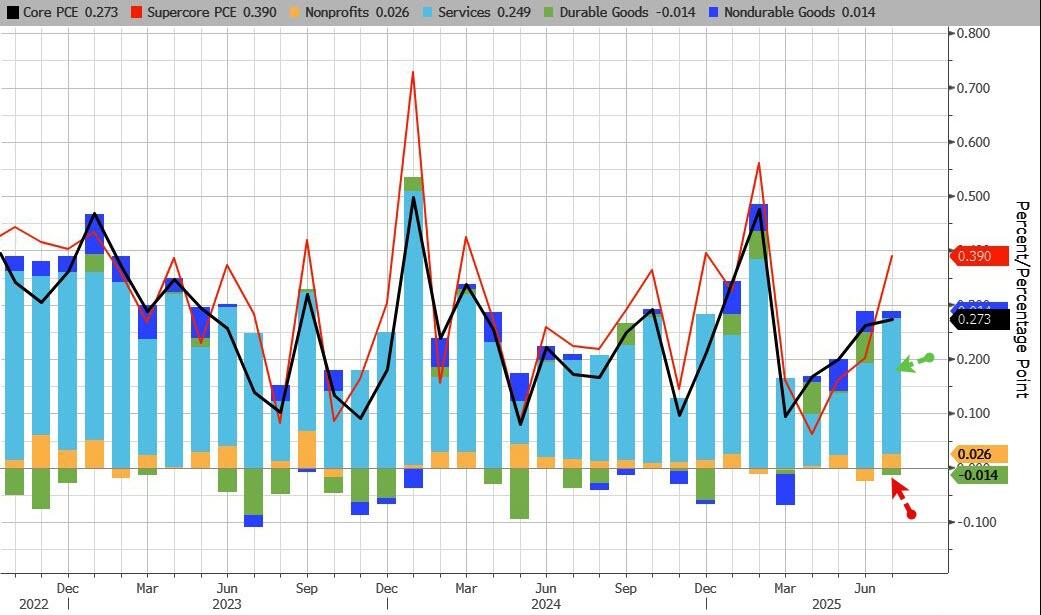

Durable Goods prices decline MoM while Services costs increased the most…

{kind=link}

Source: Bloomberg

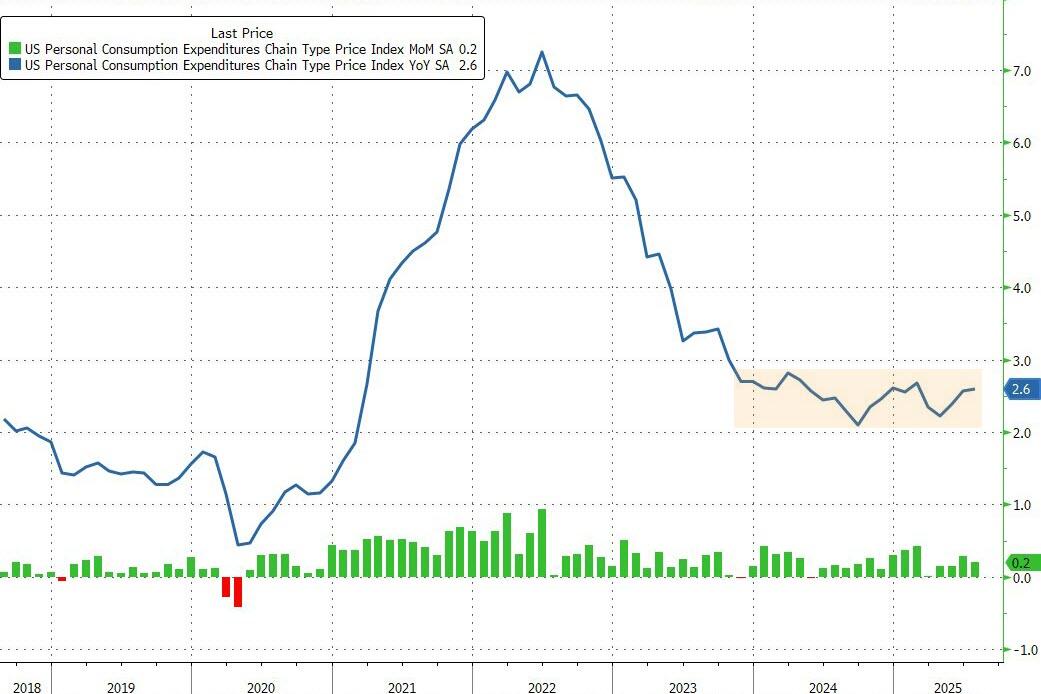

Headline PCE rose 0.2% MoM (as expected) and +2.6% YoY (as expected)…

{kind=link}

Source: Bloomberg

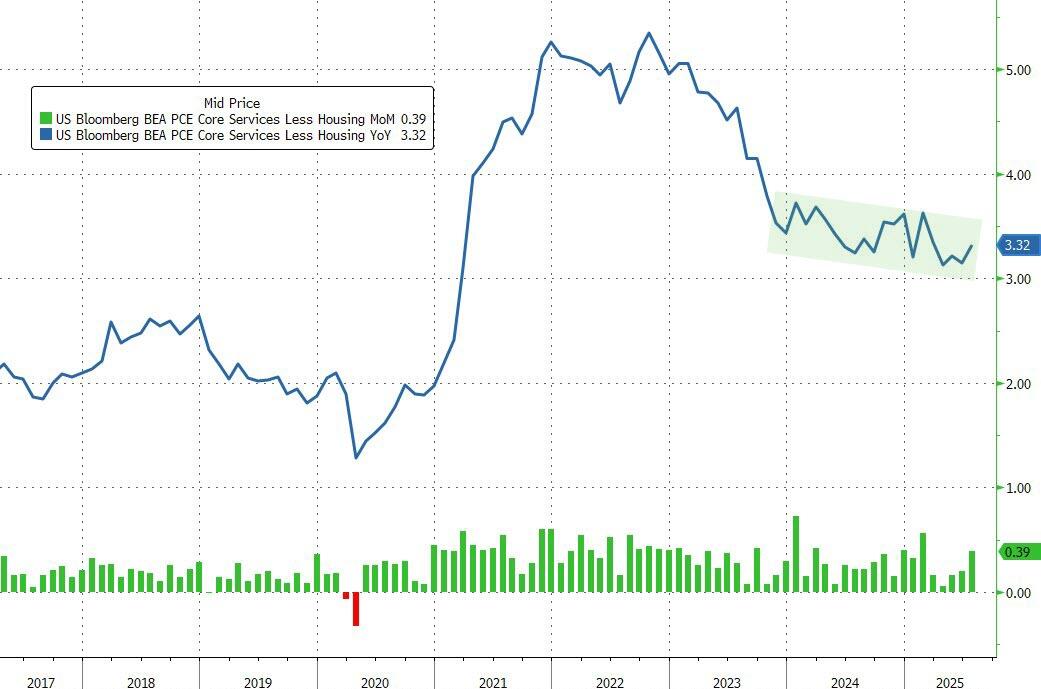

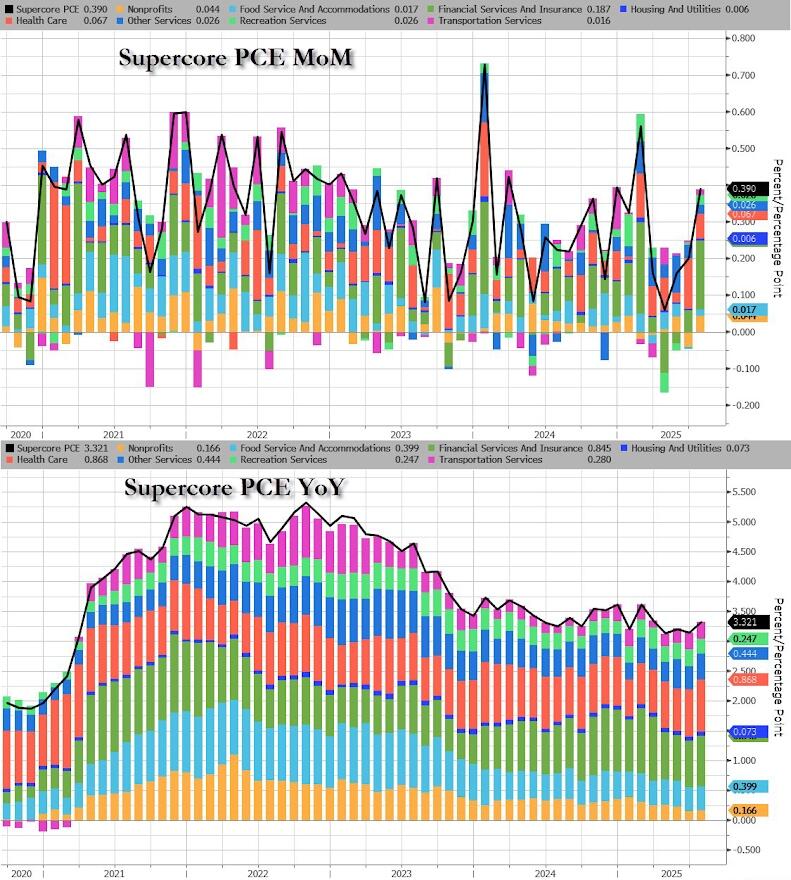

Super Core PCE – Services Ex-Shelter – rose to +3.32% YoY in July – the same level it was at in July 2024…

{kind=link}

Source: Bloomberg

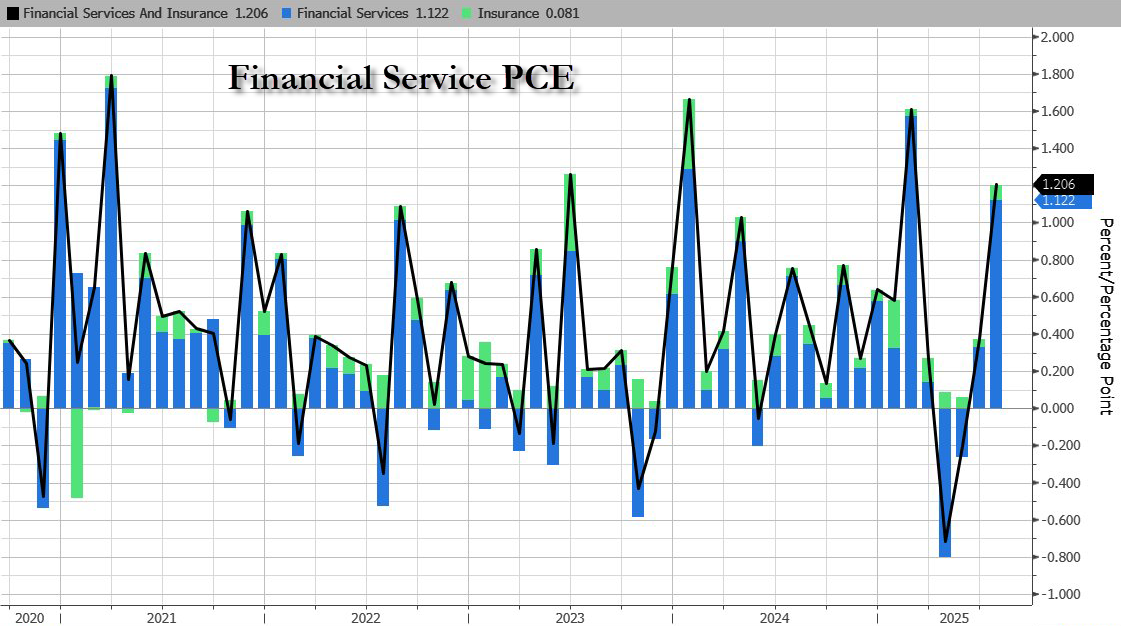

Financial Services costs (soaring stock market?) dominated SuperCore prices (and certainly have nothing to do with tariffs at all)…

{kind=link}

Source: Bloomberg

So stocks up, financial services costs up, inflation up?

{kind=link}

Source: Bloomberg

Blame Trump?

{kind=link}

Source: Bloomberg

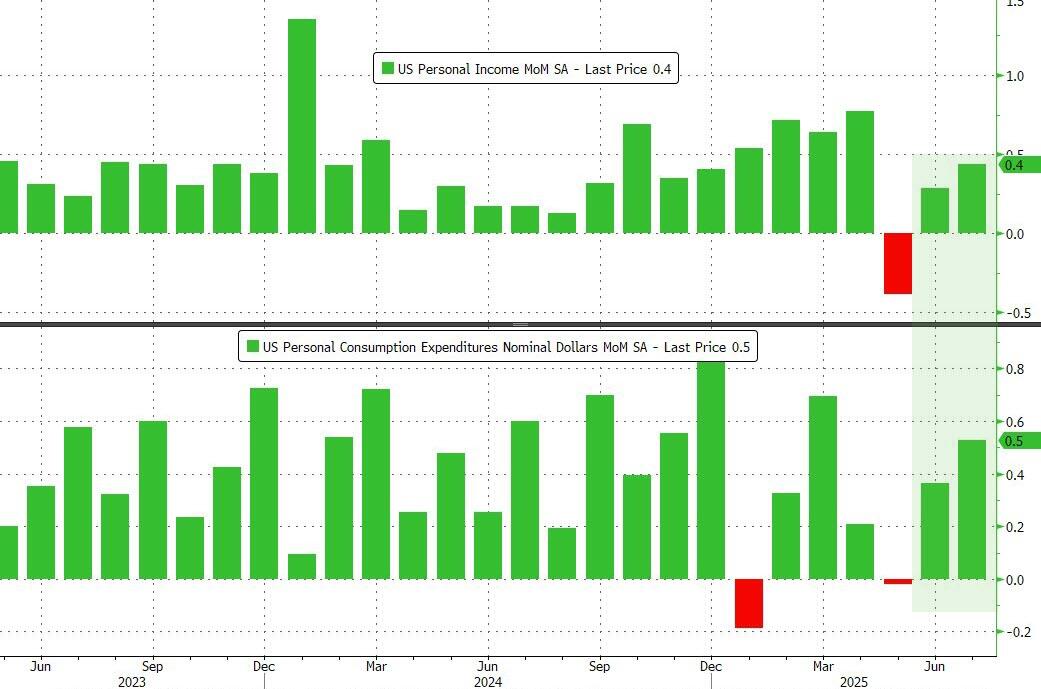

So while prices are rising but in their recent normal range, income and spending rose just ‘as expected’, up 0.4% MoM and 0.5% MoM respectively…

{kind=link}

Source: Bloomberg

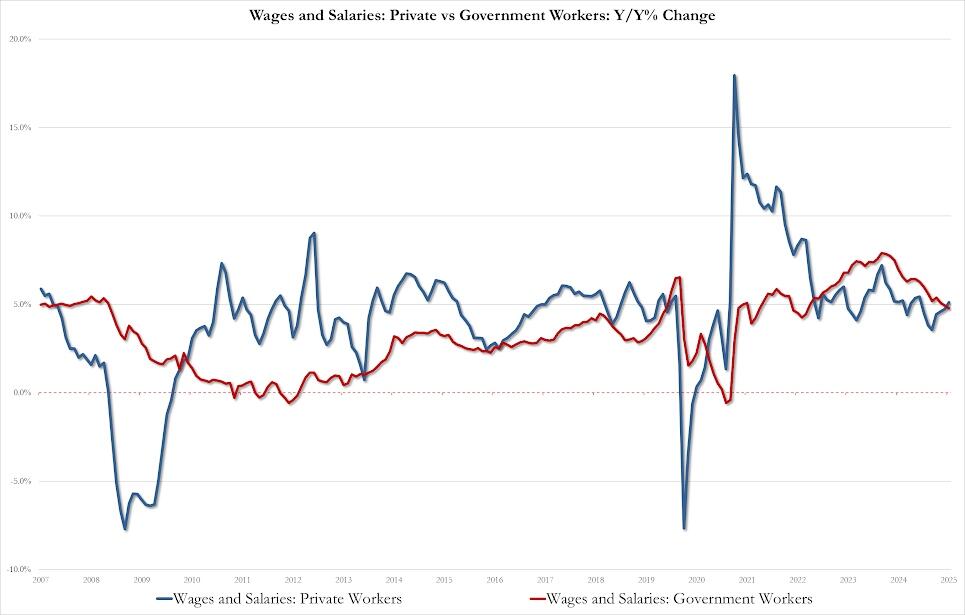

On the income side, for the first time since Dec 2022, wages of private workers (5.1% YoY) are rising faster than government workers (4.8%)

{kind=link}

Real personal spending (adjusted for inflation) rose 2.1% YoY (slower than recent months but still positive)…

{kind=link}

Source: Bloomberg

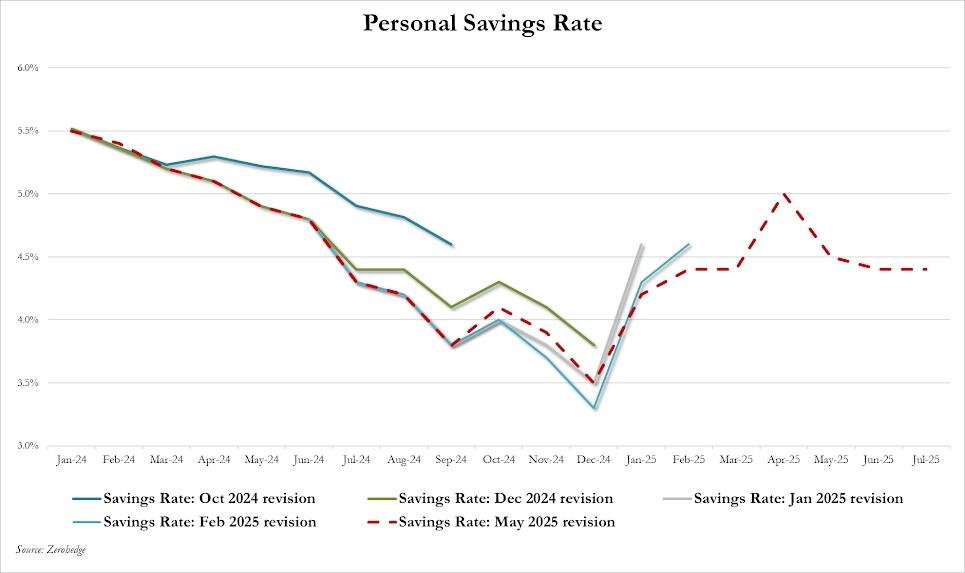

Not exactly screaming that the consumer is struggling with the savings rate flat at 4.4% of DPI…

{kind=link}

…the lack of inflationary impact from tariffs is ‘transitory‘?

Tyler Durden

Fri, 08/29/2025 – 08:41