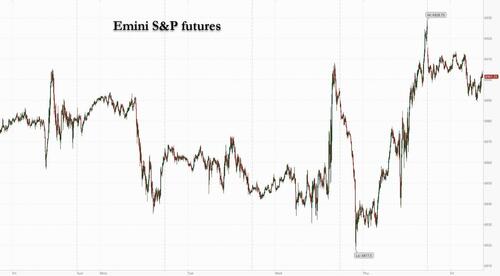

Futures Dip After Hitting Record High, As Fed’s “QE Lite” Sets Up Christmas Rally

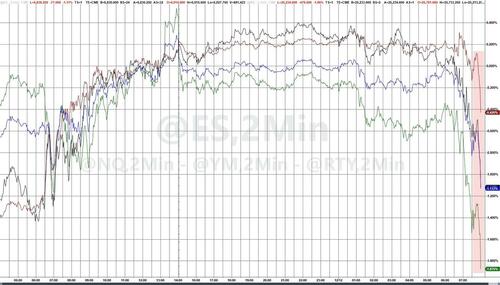

US equity futures are mixed; with small caps higher and tech stocks lagging. As of 8:15am ET, S&P 500 futures fall 0.1% after hitting a fresh record high yesterday; Nasdaq 100 contracts -0.5% amid signs of rotation out of tech as the equity rally broadens; Oracle led the broader sector lower on Thursday and Broadcom is poised to do the same in US trading after its sales outlook failed to meet investors’ lofty expectations. Its shares are down over 6% in premarket on lack of updated guidance, adding to weaker AI trade sentiment. In pre-market trading, Mag 7 stocks are mostly lower with NVDA -0.6% and MSFT/META -0.3%; AVGO fell -5.7% after its earnings call despite universal beats across all metrics (bears pointed to the lack of FY27 AI revenue guide). Today we have the first POMO Lite operation by the Fed, in which the central bank will buy $8.2BN in bills this morning, setting up the market for a Christmas rally. Europe’s Stoxx 600 rose as much as 0.5% to a fresh peak, while a measure for Asia advanced to less than 2% from its all-time high. Bond yields are largely unchanged; USD is higher modestly. Commodities are mostly higher led by base metals (copper +2.7%) and gold/silver (+1.1%). There is nothing on the economic calendar; Fed speakers include Philadelphia’s Paulson (8am), Cleveland’s Hammack (8:30am) and Chicago Goolsbee, who dissented from Wednesday’s decision in favor of no change (10:35am).

{kind=link}

In premarket trading, Mag 7 stocks are mostly lower (Alphabet +0.4%, Apple -0.1%, Amazon little changed, Tesla -0.2%, Meta -0.4%, Microsoft -0.4%, Nvidia -0.1%).

Bristol Myers (BMY) rises 2% after Guggenheim Securities upgraded the drugmaker to buy, citing a “much more compelling risk reward.”

Broadcom (AVGO) falls 5% after the chip company provided a sales outlook for the AI market that failed to meet investors’ expectations.

Eli Lilly & Co (LLY) rises 1% after Reuters reported that the FDA’s Commissioner Office sought to cut the time reviewers spent checking documents related to the drugmaker’s experimental weight-loss pill to one week from 60 days.

Lululemon (LULU) climbs 9% after the yoga-wear retailer said its CEO Calvin McDonald will step down after a seven-year stint, signaling a potential strategy change after sales struggled and the stock fell more than 60% from a 2023 peak.

Netskope Inc. (NTSK) declines 5% after the security software company posted fiscal third-quarter results.

Quanex Building Products (NX) climbs 22% after posting fourth-quarter profit and revenue that topped expectations.

Roblox (RBLX) falls 2% after JPMorgan downgrades to neutral, seeing the stock taking a breather next year due to headwinds around user engagement and bookings.

Veeva Systems (VEEV) falls 2% on light volume after KeyBanc cut the recommendation on the life-sciences software company to sector weight, saying that a recent round of channel checks has indicated large pharma clients that are in the middle of software evaluations are leaning toward Salesforce’s offering.

In other corporate news, Uber expects to offer robotaxi services in more than 10 markets by the end of next year, as it seeks to become a dominant force in an industry it estimates will eventually be worth at least $1 trillion. A group of Swiss lawmakers proposed allowing UBS to use AT1 bonds instead of equity to meet capital requirements. T-Mobile US authorized a new shareholder return program of up to $14.6 billion.

S&P 500 futures were slightly weaker after the index notched a record close in the previous session. By contrast, gauges for US blue-chip and small-cap stocks were poised to extend their push into fresh highs. The diverging fortunes for US equities highlight the broadening of a rally that has put the S&P 500 on track for a third successive year of gains. For many investors, this week’s affirmation that the Federal Reserve’s easing cycle is still intact is clearing the way for a year-end rally.

Traders “are searching for alternative real assets, especially given the Federal Reserve rate cut and the possibility of more to come,” wrote Richard Hunter, head of markets at Interactive Investor. “The rotation also provides something of a hedge for investors, where concentration risk among the ‘Magnificent Seven’ in particular was becoming more of an issue.”

Investors were seeking more clarity on when and how Broadcom will get a payoff from AI but, instead, they got a vague timetable mixed with some concerns about tightening profit margins. Meanwhile, Softbank is said to be studying an acquisition of data center operator Switch to expand in AI and Microsoft’s Mustafa Suleyman describes the technology as “already superhuman” in this weekend’s Big Interview with Bloomberg’s Mishal Husain

Diversification across geographies and themes is becoming a key consideration. After technology heavyweights drove equity gains for much of the year, concerns about stretched valuations and vast capital outlays have prompted investors to look for opportunities elsewhere.

“Given the set-up in markets, diversification is now the price worth paying to keep you fully invested in equities,” wrote Goldman Sachs’s Mark Wilson. He adds that there are compelling investment stories including Korea, Japan, China or the broader emerging markets.

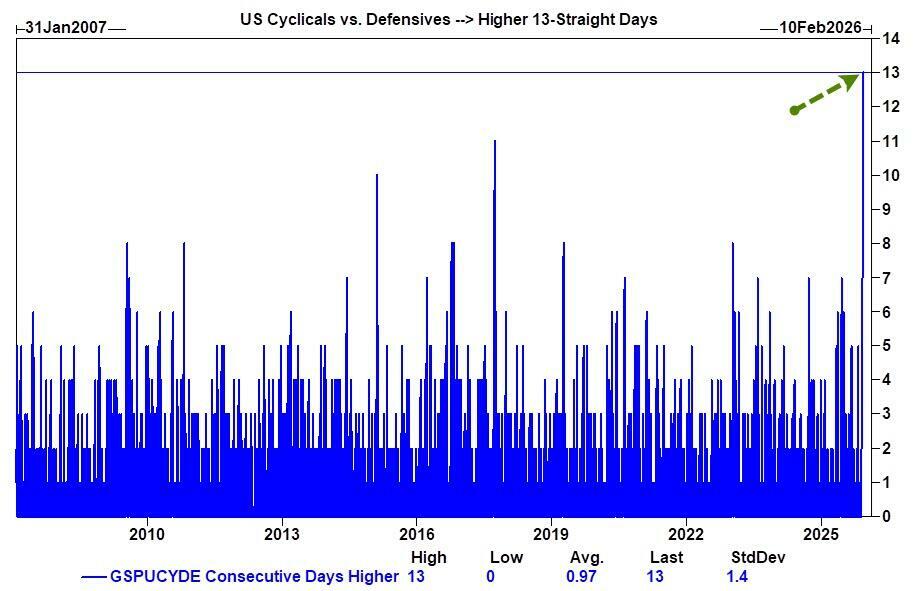

As we noted yesterday, Goldman’s Cyclicals vs. Defensives basket is on its longest rising streak in years. “You don’t get moves like this unless the market is starting to lean into a better growth outlook,” wrote Goldman Sachs managing director Lee Coppersmith.

{kind=link}

Meanwhile, Goldman strategists expect stocks to notch fresh records next year, citing resilient economic growth and broader adoption of artificial intelligence to support corporate earnings. Goldman’s Ben Snider reaffirmed his target for the S&P 500 to reach around 7,600 points in 2026, implying gains of about 10% from current levels. Other forecasters and asset managers share the upbeat view, with strategists at firms including Morgan Stanley, Deutsche Bank AG and RBC Capital Markets LLC also calling for US stocks to rise more than 10%.

Some are eyeing gains on an even shorter horizon, betting on further advances before 2025 ends as investors rotate into stocks that have so far remained in tech’s shadow. “Everyone is convincing themselves that there will be a Christmas rally, so it looks like there will be one, and to be honest, there’s no negative catalyst visible until the end of the year,” said Karen Georges, a fund manager at Ecofi Investissements in Paris. “Investors are keen to buy this year’s laggards, it’s a good time to diversify your portfolio at the moment.”

In government news, Trump issued an executive order seeking to limit the influence of proxy advisory firms. Trump also said the US would help with Ukraine’s security in a peace deal with Russia, but continued to express frustration with the pace of the talks.

European stocks tracked their Asian counterparts higher. The Stoxx 600 is up 0.3% after hitting a record earlier. The travel and leisure sector outperforms, while health care stocks lag. Here are some of the biggest movers on Friday:

UBS shares jump as much as 5%, hitting the highest level since February 2008, after a group of influential Swiss lawmakers proposed watering down the capital demands that the country wants to impose on the bank.

LPP shares surge as much as 12%, hitting an all-time high, after the clothing company reported quarterly results above expectations and boosted its guidance for 2027.

Wendel shares rise as much as 7.4%, the most since April, after the French investment firm announced plans to return more than €1.6 billion to shareholders by 2030.

Sopra Steria shares rise as much as 6.5% after the French digital and software consulting firm picked Rajesh Krishnamurthy as its new chief executive.

CarrefourSA shares climb a smuch as 9.9% in Istanbul after Mergermarket reported parent Sabanci Holding is in talks to sell some of the Turkish grocery stores.

Harbour Energy shares rally as much as 7.6% after the British oil and gas company agrees to buy substantially all the subsidiaries of Waldorf Energy Partners and Waldorf Production for $170 million.

Card Factory shares fall as much as 35%, the most since March 2020, after the firm cut its guidance in what Panmure Liberum called a “shock warning that surprises in scale.”

Asian stocks climbed, buoyed by a rally in Japanese equities on bets the Bank of Japan will hike interest rates next week. The MSCI Asia Pacific Index rose as much as 1.3%, putting the gauge on track to close at the highest in a month. All sectors were in the green, with TSMC, Toyota Motor and Tencent contributing the most to the advance.

For the week, the gauge was up about 0.6%, on course for its third straight week of gains. Japan’s Topix was the best performing major index in the region, up 2% to a fresh record, driven by insurance and banking stocks seen as key beneficiaries of a potential hike.

In FX, Bloomberg’s index of the dollar traded near a two-month low on Friday and was on track for a third weekly loss; the pound is down 0.1%.

In rates, treasuries are mixed, with weakness at the long-end steeping the curve. US 10-year yields rise 1 bp to 4.17%. Gilts see a similar steepening move after the UK economy posted a surprise contraction in October.

In commodities, spot gold climbs $55 to the highest since October. Bitcoin falls 0.5%. WTI crude futures drop 0.3% to near $57.40 a barrel.

Fed speakers include Philadelphia’s Paulson (8am), Cleveland’s Hammack (8:30am) and Chicago Goolsbee, who dissented from Wednesday’s decision in favor of no change (10:35am); US economic calendar is blank, with several delayed releases scheduled for next week

Market Snapshot

S&P 500 mini -0.1%

Nasdaq 100 mini -0.5%

Russell 2000 mini +0.2%

Stoxx Europe 600 +0.4%

DAX +0.5%

CAC 40 +0.7%

10-year Treasury yield +1 basis point at 4.17%

VIX +0.3 points at 15.17

Bloomberg Dollar Index little changed at 1207.36

euro little changed at $1.1729

WTI crude -0.3% at $57.44/barrel

Top Overnight News

Trump posted that “Prices are coming down FAST, Energy, Oil and Gasoline, are hitting five-year lows, and the Stock Market today just hit an All Time High. Tariffs are bringing in Hundreds of Billions of Dollars.

Trump signed an executive order on AI, according to the White House website. Furthermore, a Trump administration aide said the executive order is to make sure AI can operate within a single national framework and that they are taking steps for a single national standard on AI.

Fed regional bank presidents were reappointed in a unanimous vote, with new five-year terms beginning March 1st.

US offers ‘free economic zone’ in east if Ukraine cedes Donbas, Zelenskiy says: RTRS

Trump said the WSJ has another ridiculous story that China is dominating us, and the world, in the production of electricity related to AI.

US admiral leading US troops in Latin America to step down: RTRS

China Prepares as Much as $70 Billion in Chip Sector Incentives: BBG

Nvidia considers increasing H200 chip output due to robust China demand, sources say: RTRS

White House said Trump signed an order to increase oversight of and take action to restore public confidence in the proxy adviser industry.

Ukraine fails to fill key posts as corruption scandal lingers: RTRS

Trump is expected to push the government to dramatically loosen federal restrictions on marijuana.

US Treasury Department is reportedly planning more access to corporate tax breaks for R&D, and an announcement may come as soon as next week.

Seizure of Venezuelan Oil Strikes at the Heart of Maduro’s Grip on Power: WSJ

The US government is to require AI vendors to measure political bias.

Hope for More Rate Cuts Is Tempting Buyers Back to Bonds: WSJ

Indiana’s Republican-controlled Senate rejected the Congressional redistricting plan backed by President Trump.

Law Professor Sues Boeing After Alleged Exposure to Toxic Fumes on Flight: WSJ

Trade/Tariffs

Indian PM Modi said he had a call with US President Trump on Thursday as New Delhi seeks relief from 50% US tariffs on some of the country’s key exports to punish India for its Russian oil purchases.

Indonesia’s chief negotiator to the US said they agree to conclude what had been agreed in July, and Indonesia hopes to conclude tariff negotiations with the US by year-end, while Indonesia will send a delegation to Washington to continue tariff talks soon.

South Korea’s Trade Ministry said rare earth trade talks with China will continue.

Chinese Commerce Ministry announces export licenses for some steel products, with the license to kick in from January 2026.

Argentina’s Government confirms cut to export tax on grains and by-products, according to the Official Gazette.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were predominantly higher following on from the mostly positive handover from Wall St, where the S&P 500 and DJIA notched record closes, but the Nasdaq lagged on Oracle-related headwinds. ASX 200 rallied with mining, materials and financials leading the broad advances, with nearly all sectors in the green. Nikkei 225 advanced after Japan’s Lower House recently approved the supplementary budget bill, with the index briefly returning to above the 51,000 level before fading some of the gains. Hang Seng and Shanghai Comp were somewhat mixed as the Hong Kong benchmark conformed to the upbeat mood in the region, although the mainland lagged despite the recent Central Economic Work Conference where it was stated that China is to make use of RRR and rate cuts flexibly, while China’s pledge to implement an appropriately loose monetary policy, implement more proactive fiscal policy, and stabilise the property market with city-specific measures, failed to inspire.

Top Asian News

Japanese Finance Minister Katayama said they will review various special measures for corporate tax.

BoJ is likely to maintain its pledge next week to keep raising rates at a pace dependent on how the economy reacts to each increase, according to Reuters sources. Will not release updated estimate on neutral rate, will not use it as the main communication tool on rate hike timing.

China Industry Ministry said it issued a notice on optimising the import and export supervision measures of lithium thionyl chloride batteries.

A Japanese Finance Ministry Official said participants at today’s primary dealers meeting said a sale reduction of super long JGBs is desirable.

China prepares as much as USD 70bln in chip sector incentives, according to Bloomberg sources.

European bourses (STOXX 600 +0.4%) opened mostly firmer and have continued to reside at highs throughout the morning. European sectors hold a strong positive bias. Travel & Leisure leads alongside Financial Services, whilst Healthcare lags. For Financials, UBS (+4.3%) shares have hit a 17-year high as traders continue to digest reports that Swiss lawmakers have floated a compromise on new capital rules for the bank.

Top European News

European Commission reportedly considers the second phase of the safe loan scheme for defence projects.

ECB said it will ask banks to describe what sort of political shock would reduce their CET1 by 300bps

FX

G10s are modestly mixed vs the Dollar this morning, with very slight underperformance in the JPY, where USD/JPY currently trades at the upper end of a 155.46 to 155.93 range.

DXY is trading within narrow ranges after declines on Thursday. Today’s US docket does not have too much to offer in terms of data; we expect FOMC voters Schmid, Miran and Goolsbee to provide reasoning to their dissents. Currently trades within 98.29-98.44 parameters, trading at session highs at the time of writing; there may be some resistance at its 100DMA at 98.64.

Despite GDP figures signalling a contraction in growth for October, sterling trades a just touch lower against the USD. GDP data showed continued weakness in production and construction, with the ONS noting JLR was unable to spark a recovery after production was halted in November.

Elsewhere, the Antipodeans were the outperformers in the G10 FX space amid higher commodity prices, but have since pulled back off their best levels as sentiment wanes a touch.

Fixed Income

USTs have held a negative bias this morning, attempting to scale back from some of the strength seen post-FOMC, which also sparked a steepening of the curve. Today, US paper is trading at the lower end of a 112-09+ to 112-14 range; there is now a clear path towards the 112-00 mark, should the pressure continue, and then 111-29 thereafter. The data docket ahead is void of any pertinent data, but focus will be on scheduled Fed speak via Paulson, Hammack and Goolsbee – the latter, alongside Miran and Schmid, should release an explanation for their recent dissent also.

Bunds are following USTs and have held a negative bias throughout the morning. Some modest upticks were seen following the softer-than-expected UK GDP figures, but this ultimately proved fleeting. For the EZ specifically, German/French CPIs were unrevised, whilst Spanish HICP Y/Y was revised a touch higher – no move was seen in the German benchmark, which currently hovers just shy of the 127.50 mark.

Gilts initially gapped higher by around 11 ticks at open after the UK’s softer-than-expected GDP report, but have since waned following the negative bias seen across global peers. Currently trading at the lower end of a relatively narrow 91.38 to 91.63 range.

Commodities

Crude benchmarks continue to rebound following Thursday’s selloff on broader market optimism and rising geopolitical tensions between Venezuela and the US. WTI and Brent oscillate in a USD 57.85-58.19/bbl and USD 61.49-61.86/bbl band, respectively, as the European session gets underway. This comes following a bounce from their lows in nearly two months, as equities stateside began to rebound.

Spot XAU continues to trend higher after breaking out of its 9-day range in Thursday’s session. After peaking at USD 4286/oz in Thursday’s session, XAU spent the APAC session fluctuating in a USD 4265-4284/oz range before extending higher as short positioning continues to unwind.

3M LME Copper peaked to another ATH of USD 11.94k/t in the latter part of the APAC session, but has failed to hold onto gains as the European session gets underway. The red metal rallied in Thursday’s session, in line with the broader risk tone, but has pulled back and is currently trading at USD 11.8k/t as participants take profit.

India Minister says India to start coal export for the first time.

Geopolitics: Middle East

White House said a lot of quiet planning is underway for the next phase of the Gaza peace plan, and they will make announcements at an appropriate time.

Geopolitics: Ukraine

US President Trump said they would help on security with Ukraine, and he thought they were close to a deal, while he added that there is a meeting on Saturday, and they will attend if they think there is a good chance. Trump also commented that he has spoken to China and Russia about nuclear weapons.

Kremlin Aide said the US will sooner or later discuss with Moscow the outcome of its discussion with Ukraine, via RIA. Moscow did not revise US proposals after discussing with Ukraine and may “not like a lot of things there”.

Russia’s Kremlin, on Ukraine’s referendum suggestion, said the whole of Donbass belongs to Russia

Geopolitics: Other

US President Trump said that it is going to start on land soon regarding Venezuela.

US is reportedly preparing to seize more ships transporting Venezuelan oil, in which action would target tankers that may have transported other sanctioned crude such as Iranian, while the seizure has led to a suspension of at least three shipments, according to Reuters sources.

US Treasury issued fresh Venezuela-related sanctions in which it was reported to have sanctioned Venezuelan President Maduro’s nephews and six ships carrying Venezuelan oil.

US President Trump said he will have to make a couple of phone calls regarding Thailand and Cambodia. It was later reported that Thailand’s PM said a call with US President Trump is set for 21.20 local time 14:20GMT/09:20EST.

China’s Military said small Philippine aircraft “invaded” Scarborough Shoal airspace. Monitored, warned forcefully and drove away the aircraft.

US Event Calendar

No Macro data

8:00 am: Fed’s Paulson Speaks on Economic Outlook

8:30 am: Fed’s Hammack Speaks at Real Estate Roundtable Series

10:35 am: Fed’s Goolsbee Speaks at Economic Outlook Symposium

DB’s Jim Reid concludes the overnight wrap

Thank Friday it’s Friday after a busy week. There won’t be much thanks in our household though as school breaks up today and we have to work out what to do with them for another 10 days before we go on holiday. If anyone wants a 10yr old, or two identical 8yr olds as an intern for a week let me know. Skills? Eating cake. Weaknesses? Not clearing it up. Apply within!

The celebratory cake ended up being rolled out last night after an inauspicious start, with the S&P 500 (+0.21%) recovering from a weak open to reach a new all-time high. US equities were initially weighed down by a big slump for US tech stocks as Oracle (-10.83%) was the worst performer in the S&P 500 following its earnings release. However, the broader market mood was more positive as investors continued to digest the Fed’s rate cut from the previous day, and also helped by ebbing inflation fears as 2yr inflation swaps fell to their lowest in 13 months. And Europe saw a strong rally across the board as investors dialled back the chance of an ECB rate hike next year, which helped the STOXX 600 (+0.55%) to close less than half a percent beneath its record high.

Those earnings from Oracle (-10.83%) on Wednesday night were a big story yesterday, as it revived fears about the sustainability of AI spending. As a reminder, they reported revenue that was beneath expectations, and capital expenditures that were above expectations. So that meant the share price fell to its lowest level since June, having now shed -39% since its closing peak back in September. Remember as well that Oracle’s CDS spreads have been used as a hedge against a potential AI bubble, and their 5yr CDS spreads rose +12bps to 134bps by the close, their highest level since 2009 around the GFC. It seems to me that since early October the AI trade has changed from everyone being a winner to winners and losers. In the period where Oracle is down nearly -40%, fellow hyperscaler Google is up around +30%. There are other examples of winners and losers with the likes of Coreweave down -39% since early October and the poster child of AI, namely OpenAI under much more scrutiny. I can’t help but think this trend would continue in 2026 where the AI story will result in more divergence. For markets overall it will depend on whether one of the mega cap stocks get on the wrong or right side of that winners and losers equation.

Back to yesterday and while the Oracle news cascaded across US tech stocks, leaving the Magnificent 7 -0.66% lower on the day, the overall equity market managed to shake off initial negativity as the optimism we saw after the Fed’s rate cut on Wednesday again took hold. The S&P 500 (+0.21%) reversed a -0.77% decline early in the session, and outperformance by blue-chip and small-cap stocks also sent the Russell 2000 (+1.21%) and the Dow Jones (+1.34%) to new record highs.

The swing in AI sentiment continued with Broadcom’s earnings after the US close. Following a +78% advance YTD, the chipmaker now has a larger market cap than Meta and Tesla, playing a growing role in the tech market narrative. The stock initially advanced +4% after-hours after unveiling stronger-than-expected revenue guidance for the current quarter ($19.1bn vs $18.5bn est.). But it then turned sharply lower as management held off on giving an AI revenue forecast for the year, leaving Broadcom’s shares down -4.5% by the end of after-market trading. NASDAQ 100 futures are down a tenth and the S&P equivalent is flat.

US Treasuries also had a mixed day yesterday. Yields initially moved lower as markets digested the Fed’s latest rate cut and reacted to messy set of weekly claims data. However that move reversed as the session went on, and 10yr yields (+0.9bps to 4.16%) inched higher late in the session after the Fed Board unanimously reappointed eleven Fed regional presidents to new five-year terms (Atlanta Fed President Bostic, who is retiring, was the lone exception). The regional presidents’ current terms expire in February so the advance announcement suggests that the Board was united in wanting to avoid the risk that the reappointment process raises questions over Fed independence.

At the frontend, 2yr Treasury yields (+0.2bps) were little changed, with their rise limited by a decline in breakevens as the 2yr inflation swap fell -2.0bps to 2.43%, its lowest level since November 2024. That was in part due to oil prices declining to their lowest since October, with Brent crude down -1.49% to $61.28/bbl. The amount of Fed cuts priced by December 2026 stayed at 55bps (-0.4bps on the day), so still consistent with at least two cuts next year. Meanwhile, the recent dollar weakness continued, with the dollar index (-0.45%) hitting an eight-week low.

Over in Europe, markets put in a strong performance as investors dialled back their expectations for ECB rate hikes next year. By the close, the chance of a hike by the December 2026 meeting was down to 28%, which is still noticeable, but down from 40% the previous day when front-end yields hit their highest in months. So those more dovish expectations supported assets across the continent, with the STOXX 600 (+0.55%) closing half a percent beneath its record high, whilst Spain’s IBEX 35 (+0.72%) hit an all-time high. Similarly for sovereign bonds, yields on 10yr bunds (-0.8bps), OATs (-1.4bps) and BTPs (-2.0bps) all moved lower.

Otherwise in Europe, the main story was from the Swiss National Bank, who left their policy rate at 0% as expected. However, the perception was that a return to negative interest rates was unlikely in the next few meetings, and SNB Chair Schlegel said that the “hurdle is higher for the introduction of a negative interest rate”. That backdrop meant the Swiss franc was the top-performing G10 currency yesterday, up +0.57% against the US dollar. Meanwhile, yields on 10yr Swiss government debt rose +0.8bps, contrary to the declines across the rest of Europe.

Asian stock markets have gathered some positive momentum this morning with the Hang Seng index (+1.69%) leading the way, while the S&P/ASX 200 (+1.23%) is also notably higher, continuing the substantial increases from the previous session. Elsewhere, the Nikkei (+1.08%) and the KOSPI (+1.13%) are also strong supported by a recovery in technology stocks. The CSI (+0.57%) and the Shanghai Composite (+0.31%) are lagging a bit, as local semiconductor manufacturers are lower due to the anticipated rise in competition from NVIDIA Corporation.

Finally, there wasn’t much economic data yesterday, although we did get the weekly initial jobless claims from the US. They were higher than expected, at 236k in the week ending December 6 (vs. 220k expected). Treasuries saw a modest rally following the release but for the most part markets took the print in their stride. There were always expectations of choppiness around the Thanksgiving holiday, and the 4-week moving average was still at 216.75k, which is at the bottom of the range in recent months. We also had the trade balance for September, which had the US trade deficit falling to its smallest since June 2020, at just $52.8bn (vs. $63.1bn expected).

To the day ahead now, and data releases include UK GDP for October. Otherwise, central bank speakers include the Fed’s Paulson, Hammack and Goolsbee.

Tyler Durden

Fri, 12/12/2025 – 08:56