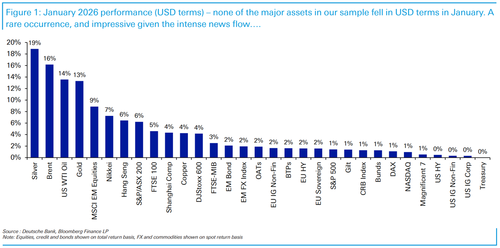

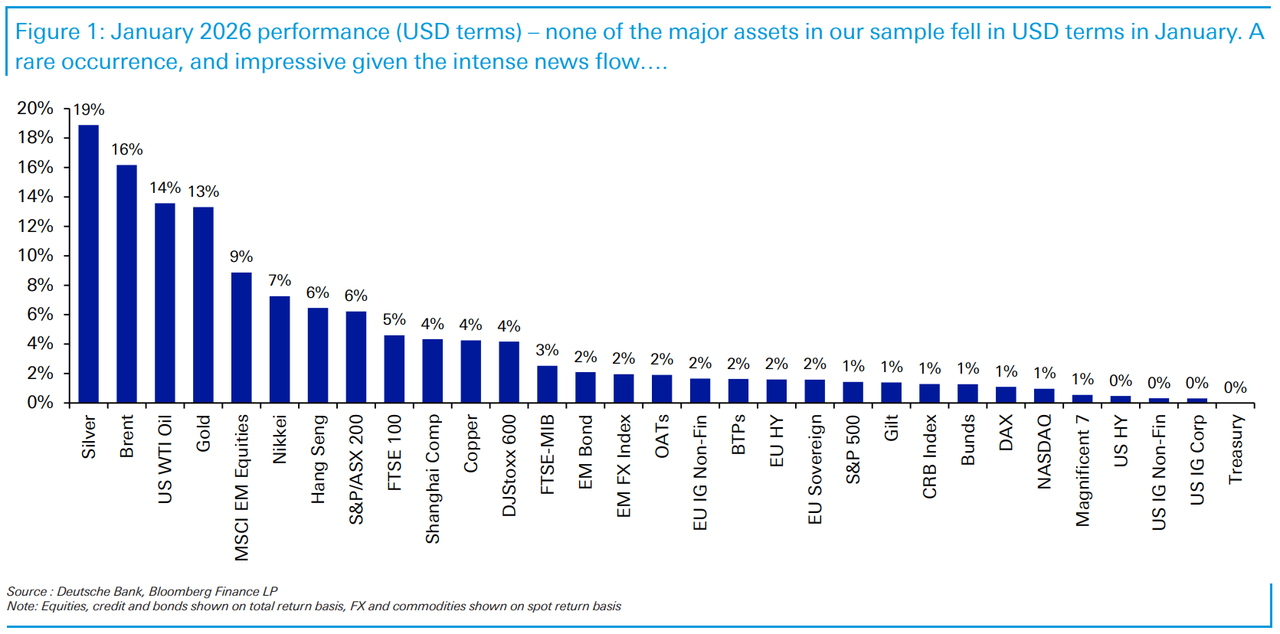

A Month Of Shock And Awe: These Were The Best And Worst Performing Assets In January

Earlier today, Deutsche Bank’s Henry Allen released his monthly performance review looking at how markets performed in January. As Jim Reid writes, “January managed to both shock and awe in various ways, yet still delivered broad based gains across all global assets in our monthly performance review when measured in USD terms—a genuinely rare occurrence. It was perhaps fitting then, that the month ended with extraordinary volatility: silver saw its largest daily fall since 1980 (36% at the intraday lows, 26.3% at the close), while Gold recorded its biggest one day decline since 2013 ( 8.95%).”

We’ll do a more detailed summary below, but here are the highlights:

The most striking feature in January was the breadth of the rally. Despite an array of risks around Venezuela, Iran, Greenland and Fed independence, nearly every major asset was still in positive territory.

Equities did well across the board, as positive data surprises continued to power risk assets. Indeed, the ISM services index hit a 14-month high, whilst the US jobs report showed unemployment ticking lower. In turn, the S&P 500 (+1.4% in total return terms) briefly poked above 7,000 for the first time, whilst the MSCI EM index (+8.9%) had its best monthly performance since November 2022.

Most notably, it was a historic and extraordinary month for precious metals, even with the late pullback. In fact, gold (+13.3%) saw its best monthly performance since September 1999, and silver (+18.9%) posted a 9th consecutive monthly gain.

Other commodities did very well, and the geopolitical risk pushed Brent crude oil (+16.2%) to $70.69/bbl, marking its biggest monthly jump in four years.

Bitcoin was one of the few major assets to end the month lower, down -10.8% to $78,197. That’s a 4th consecutive monthly decline for Bitcoin, which hasn’t happened since before the pandemic.

The US Dollar also struggled, particularly after Trump was asked about the decline, and he said “No, I think it’s great”. So the US Dollar weakened against every other G10 currency, and the dollar index also saw its worst 4-day slide since the Liberation Day turmoil last April.

Finally, there were some huge moves in Japan, where a snap election was announced for February 8. JGBs sold off amidst election pledges for more consumption tax cuts, with the 10yr yield up +18bps on the month, and the 30yr yield up another +24bps.

So January was an action-packed month. With all that’s going on, February is unlikely to be quiet.

{kind=link}

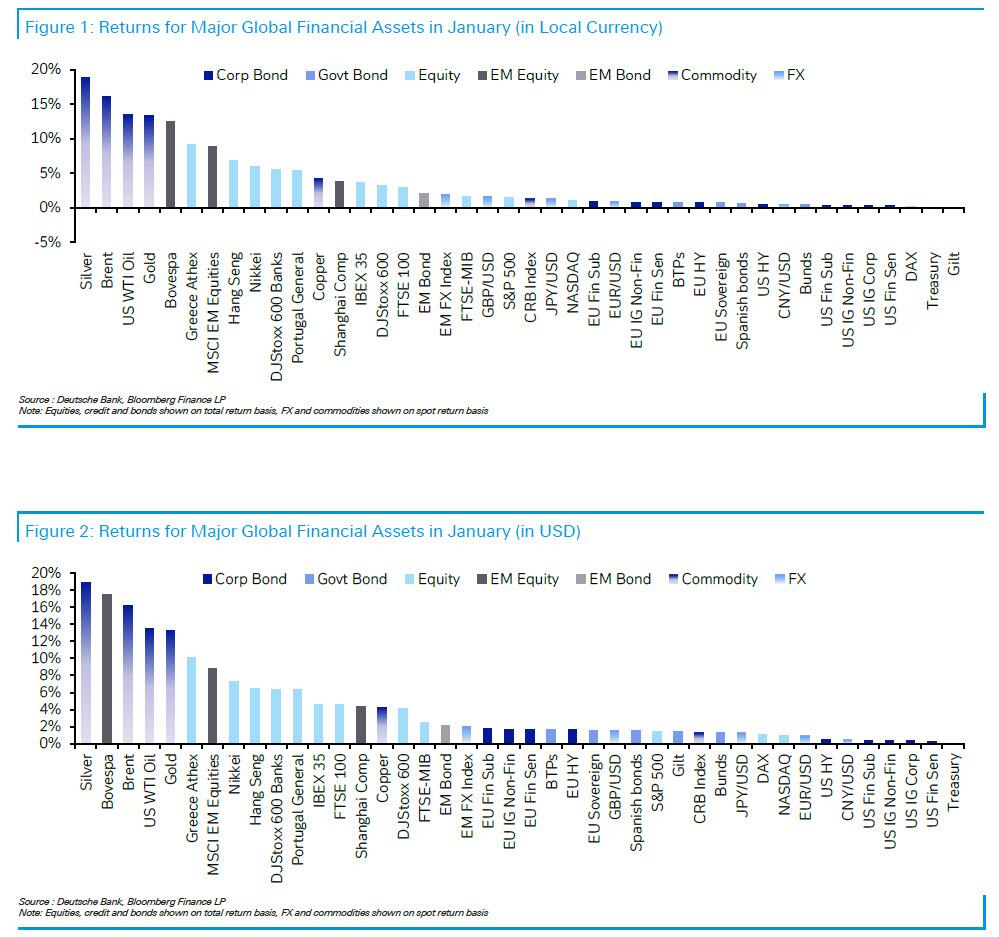

With summary in mind, here are the details:

Markets put in a strong performance in January, as positive data surprises continued to power risk assets, with the S&P 500 briefly poking above 7,000 for the first time. But just as we saw in 2025, those headline gains masked significant volatility under the surface, as geopolitical risk rose significantly, including over Venezuela, Iran and Greenland. So that meant Brent crude oil (+16.2%) saw its biggest monthly jump in 4 years, particularly after Trump warned that a “massive Armada” was heading to Iran, which raised speculation about a US strike.

Moreover, precious metals had their biggest surge in decades, with gold prices (+13.3%) seeing their biggest monthly jump since September 1999, despite the sharp pullback at the end of the month. All that came amidst growing pressure on the US Dollar, which saw its biggest 4-day decline since the Liberation Day turmoil last year, weakening against every other G10 currency in January.

Month in Review – The high-level macro overview

Geopolitics dominated the headlines in January, with the year getting off to an eventful start. The first major event was on January 3, as Venezuelan President Nicolás Maduro was captured by US forces and taken to New York. There were immediately questions about what the market implications would be, as the US EIA have said that Venezuela has the largest proven crude oil reserves in the world, with 17% of the global total. So investors had to assess whether supply disruption in the short term might be outweighed by higher production in the long term. But outside of Venezuelan assets and some US oil companies, the wider market reaction was fairly limited.

However, events in Iran led to a much clearer oil price reaction, with Brent crude ending the month above $70/bbl again. That came as speculation mounted about some kind of US strike on Iran, and Trump himself posted on Jan 13 that he had cancelled all meetings with Iranian officials, whilst calling on protestors to take over the institutions. Then on Jan 14, Reuters reported that some personnel had been advised to leave the US military’s Al Udeid Air Base in Qatar. That was significant because the base previously saw an Iranian missile attack last June, so the story added to fears that some sort of escalation might take place imminently. However, Trump later downplayed the magnitude of tensions, saying “we’ve been told that the killing in Iran is stopping — it’s stopped… And there’s no plan for executions”. However, while this led to a brief pullback in oil prices, they then resumed their ascent as trump posted on Jan 28 that a “massive Armada is heading to Iran.” So by the end of January, Brent crude was up +16.2% to $70.69/bbl, having seen its biggest monthly jump since January 2022.

The other major geopolitical story surrounded Greenland, which escalated as the month went on. For instance on Jan 14, Trump posted that “The United States needs Greenland for the purpose of National Security.” Then on Jan 17, Trump threatened a 10% tariff on several European countries from Feb 1, which would rise to 25% in June, unless “a Deal is reached for the Complete and Total purchase of Greenland”. That led to a serious risk-off move, with the S&P 500 down -2.1% on the following session. There was even speculation about more serious European retaliation, with German finance minister Lars Klingbeil said that “We are constantly experiencing new provocations, we are constantly experiencing new antagonism, which President Trump is seeking, and here we Europeans must make it clear that the limit has been reached”. However, on Jan 21, Trump then posted that “we have formed the framework of a future deal with respect to Greenland and, in fact, the entire Arctic Region.” He also said that the Feb 1 tariffs wouldn’t proceed. So that led to a market recovery, with the S&P 500 hitting another all-time high again on Jan 27, and still ending the month +1.4% higher in total return terms

Otherwise, the Federal Reserve were in the spotlight in January, particularly after the Department of Justice began a criminal investigation that revived questions around central bank independence. That also added to the upward pressure on precious metals, with gold prices moving higher throughout the month, ultimately closing up +13.3% in its best monthly performance since September 1999. If anything, that underplays the volatility, as gold prices hit an all-time intraday record of $5,595/oz on Jan 29, before pulling back sharply to close the month at $4,894/oz, including its biggest daily decline on Jan 30 (-8.95%) since April 2013. That surge in gold prices also occurred alongside a fresh move lower for the US Dollar, with the dollar index down -1.4% in January, which included the biggest 4-day slide since the Liberation Day turmoil last April. That accelerated after Trump himself was asked about the decline, and he said “No, I think it’s great”. However, the moves stabilised after Treasury Secretary Bessent reiterated the “strong dollar policy” the next day in a CNBC appearance. Finally on Jan 30, it was also announced that Kevin Warsh had been nominated by Trump to become the next Chair of the Federal Reserve.

Despite the volatility of global events in January, risk assets still put in a strong performance overall. In part, that was thanks to upbeat global data, which was still broadly robust. For instance in the US, the ISM services index hit a 14-month high of 54.4 in December. Then the jobs report showed that the unemployment rate ticked down to 4.4% in December. Meanwhile in Europe, inflation was a bit weaker than expected, which meant expectations rose that the ECB might deliver another rate cut this year. And Euro Area growth for Q4 also surprised on the upside, at a +0.3% pace. So most of the major global equity indices still advanced in January.

Finally in Japan, there were further significant market moves. That came as a snap election was announced for February 8, with JGBs selling off amidst election pledges for more consumption tax cuts. That led to a surge in long-end yields, with the 30yr yield closing at 3.86% on Jan 20, its highest since that maturity was first launched, before coming down to end the month at 3.63%. The 10yr yield also reached its highest since 1999, closing at 2.35% on Jan 20 as well, before ending the month at 2.24%. But even with the pullback, the 10yr yield was still up +18bps on the month, and the 30yr yield was up +24bps. Meanwhile, the Bank of Japan delivered a somewhat hawkish-leaning decision, as they kept rates on hold, but they also raised their inflation outlook, whilst the outlook report reiterated their desire to keep hiking rates.

Which assets saw the biggest gains in January?

Precious metals: It was a historic month for precious metals, with gold (+13.3%) rising to $4,894/oz, in its strongest monthly performance since September 1999. Meanwhile, silver (+18.9%) rose to $85.20/oz.

Oil and gas: Geopolitical risks meant Brent crude oil moved up +16.2% in January, rising to $70.69/bbl. That reversed a run of 5 consecutive monthly declines, and was the biggest monthly jump since January 2022. Natural gas also rose, with US natural gas futures up +18.2%, whilst European natural gas futures were up +39.5%, their biggest monthly jump since June 2022.

Equities: It was another strong month for global equities, with the S&P 500 (+1.4%), the STOXX 600 (+3.2%), the Nikkei (+5.9%) and the MSCI EM index (+8.9%) all rising in total return terms. For the MSCI EM index, it was the best monthly performance since November 2022.

Euro sovereigns: With inflation surprising on the downside and markets pricing a growing likelihood of an ECB rate cut this year, Euro sovereigns were up +0.7% in total return terms.

Which assets saw the biggest losses in January?

US Dollar: The dollar index fell -1.4% in January, with the dollar itself weakening against every other G10 currency. At one point in January, the Euro moved above $1.20 for the first time since 2021, before ultimately closing at $1.185.

And visually (note bitcoin is not among the assets tracked by DB or it would have been ugly);

{kind=link}

More in the full note available to pro subs.

Tyler Durden

Tue, 02/03/2026 – 08:20