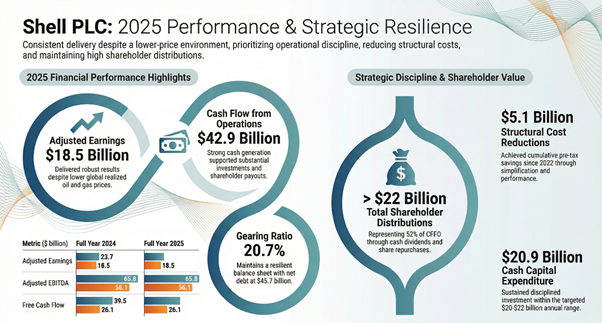

Shell plc (NYSE: SHEL) reported fourth-quarter 2025 adjusted earnings of $3.3 billion, reflecting lower commodity prices, seasonally weaker downstream performance and non-cash tax updates, while maintaining strong cash flow and shareholder distributions.

Full-year adjusted earnings were $18.5 billion, down from $23.7 billion in 2024 amid lower oil and gas prices, while cash flow from operations reached $42.9 billion.

Portfolio Shift

Shell’s 2025 results were shaped by active portfolio high-grading, including completion of the Adura joint venture with Equinor in the UK offshore sector. The group also finalized the divestment of its onshore Nigerian subsidiary, Shell Petroleum Development Company of Nigeria Limited (SPDC), and completed an oil sands asset swap in Canada, exiting its remaining 10% mining interest. These structural actions, combined with underlying field declines, led to a negative 40% reserve replacement ratio on an SEC basis for the year.

Quarterly Performance

Adjusted earnings for the fourth quarter were $3.3 billion, compared with $5.4 billion in the prior quarter, reflecting lower realized prices across Integrated Gas, Upstream and downstream segments.

Income attributable to shareholders was $4.1 billion in the quarter. Adjusted EBITDA totaled $12.8 billion. Cash flow from operations was $9.4 billion. Free cash flow reached $4.2 billion in the quarter. Net debt stood at $45.7 billion, with gearing at 20.7%.

Segmentally, Integrated Gas and Upstream remained the largest earnings contributors, while Chemicals & Products reported a quarterly loss and Marketing earnings declined sequentially due to seasonal and margin effects. Brent crude averaged $64 per barrel in the fourth quarter, compared with $69 in the previous quarter.

Full-Year Results

Adjusted EBITDA was $56.1 billion, and free cash flow reached $26.1 billion. Integrated Gas and Upstream earnings declined year-over-year due to lower realized prices, while Marketing delivered modest growth and Renewables & Energy Solutions returned to positive earnings. Average Brent prices declined to $69 per barrel in 2025 from $81 in 2024, weighing on earnings across core segments.

Capital Allocation & Shareholder Returns

Shell declared a quarterly dividend of $0.372 per share, a 4% increase under its progressive dividend framework. The company announced a $3.5 billion share buyback program, with buybacks of at least $3 billion for the 17th consecutive quarter. Total shareholder distributions for 2025 exceeded $22 billion, representing 52% of cash flow from operations. Cash capital expenditure for 2025 was approximately $21 billion. The company maintained its capex framework of $20 billion to $22 billion annually for 2025-2028.

SWOT analysis

Strengths:

Strong cash flow from operations of $42.9 billion in 2025.

Resilient balance sheet with gearing around 20.7%.

Consistent shareholder distributions exceeding $22 billion in 2025.

Diversified segment earnings across Integrated Gas, Upstream and Marketing.

Weaknesses:

Earnings decline year-over-year due to lower realized commodity prices.

Quarterly downstream and chemicals earnings showed sequential declines.

Segment earnings volatility linked to market prices and margins.

Opportunities:

Structural cost-reduction program targeting $5 billion to $7 billion by 2028.

Targeted free-cash-flow-per-share growth through 2030.

Continued shareholder distribution framework tied to cash flow generation.

Threats:

Exposure to oil and gas price volatility.

Regulatory and energy-transition-related risks.

Margin pressure in refining, chemicals and marketing segments.

Market & Macro Context

Commodity price declines were a key factor in earnings moderation. Average Brent prices fell year-over-year, while refining and chemical margins showed mixed trends. Indicative refining margins improved year-over-year, but chemical margins were lower compared with 2024. Gas pricing benchmarks showed mixed trends, with higher European gas prices but lower U.S. gas prices relative to 2024.

Balance Sheet & Cost Structure

Net debt remained at $45.7 billion at year-end 2025. Shell reported delivery of more than $5 billion in structural cost reductions since 2022 and targets total structural cost reductions of $5 billion to $7 billion by end-2028.

What Investors are Watching

Cash returns: Continuity of share buybacks and dividend growth under the stated payout framework.

Commodity prices: Sensitivity of earnings to oil and gas price movements.

Capex discipline: Execution within the $20 billion to $22 billion annual capex range.

Cost reductions: Progress toward structural cost-reduction targets through 2028.

Segment margins: Trends in refining, chemicals and marketing profitability.

Risks & Concerns

Commodity volatility: Earnings remain exposed to oil and gas price fluctuations.

Margin variability: Downstream and chemicals margins showed sequential declines in Q4.

Macro factors: Currency movements, demand shifts and regulatory developments may affect results.

Energy transition: Capital allocation across traditional and low-carbon businesses remains a key execution factor.

Forward Outlook

Shell continues to target shareholder distributions of 40% 50% of cash flow from operations through the cycle.

The company expects to maintain annual capex in the $20 billion to $22 billion range and pursue structural cost reductions through 2028.

Long-term plans include normalized free-cash-flow-per-share growth of more than 10% annually through 2030 under current planning assumptions.

The post Shell Q4 Earnings Decline on Lower Prices; Maintains Buybacks, Dividend and Capex Discipline first appeared on AlphaStreet.