US Chemical Companies “Net Beneficiaries” Of Middle East Energy Disruption Crisis

Bloomberg News headlines indicate that Iraq has begun shutting down oil output at Rumaila, the world’s largest “supergiant” oil field, while other Gulf states have idled some of the world’s largest refineries and major energy hubs following Iranian drone strikes. This signals that a massive energy disruption is set to hit global energy markets as the Strait of Hormuz remains paralyzed.

Goldman analysts led by Duffy Fischer have released a note assessing whether U.S. chemical manufacturers have exposure to Middle East energy disruptions. They find that “U.S. companies are likely to be net beneficiaries” of the Middle East conflict and the resulting energy disruptions.

Fischer pointed out that as oil prices rise, naphtha-based competitors in Europe and Asia are squeezed, while U.S. chemical makers that rely more on natural gas are relatively insulated due to domestic production. That, in turn, widens the U.S. margin advantage.

These U.S. chemical manufacturers use raw materials such as natural gas, crude oil liquids, salt, sulfur, and other minerals to produce products like:

basic chemicals: ethylene, propylene, methanol, chlorine, ammonia

plastics/resins: polyethylene, PVC, polyurethane inputs

fertilizers: nitrogen, phosphate products

industrial chemicals: solvents, coatings, acids, adhesives

specialty chemicals: ingredients used in electronics, autos, construction, packaging, and consumer goods

Fischer explained:

The oil to gas ratio is a large driver of U.S. chemical production profitability. With oil prices increasing (see our Commodity team’s note and podcast), this will push up the price of naphtha, which is likely to increase the cost of European and Asian feedstocks. Since many naphtha crackers are currently near breakeven levels, that should force them to raise prices. This should lead the spot and export prices higher for U.S. product. The result would be an increase in U.S. margins as their natural gas feedstocks are not likely to be impacted. Lastly, while the industry believed that the March PE contract prices would roll flat, the events would significantly increase the possibility of U.S. producers achieving pricing in March.

Next, the analysts assess whether U.S. chemical manufacturers have exposure to the Middle East. They point out that Middle East disruptions would benefit U.S. chemical manufacturers.

Here’s how:

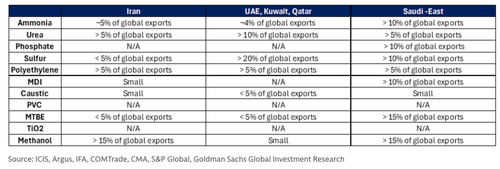

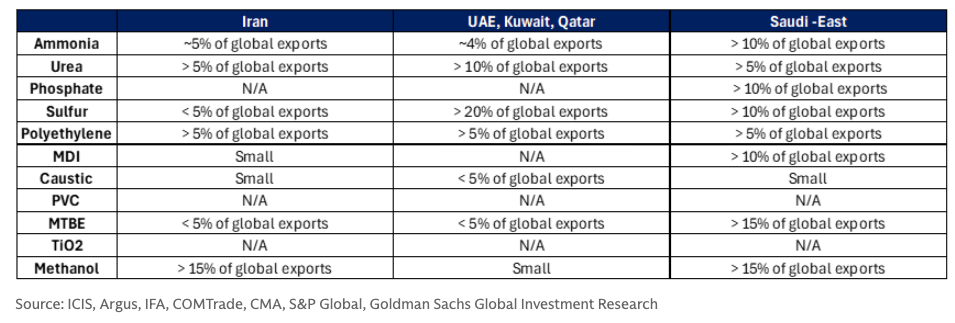

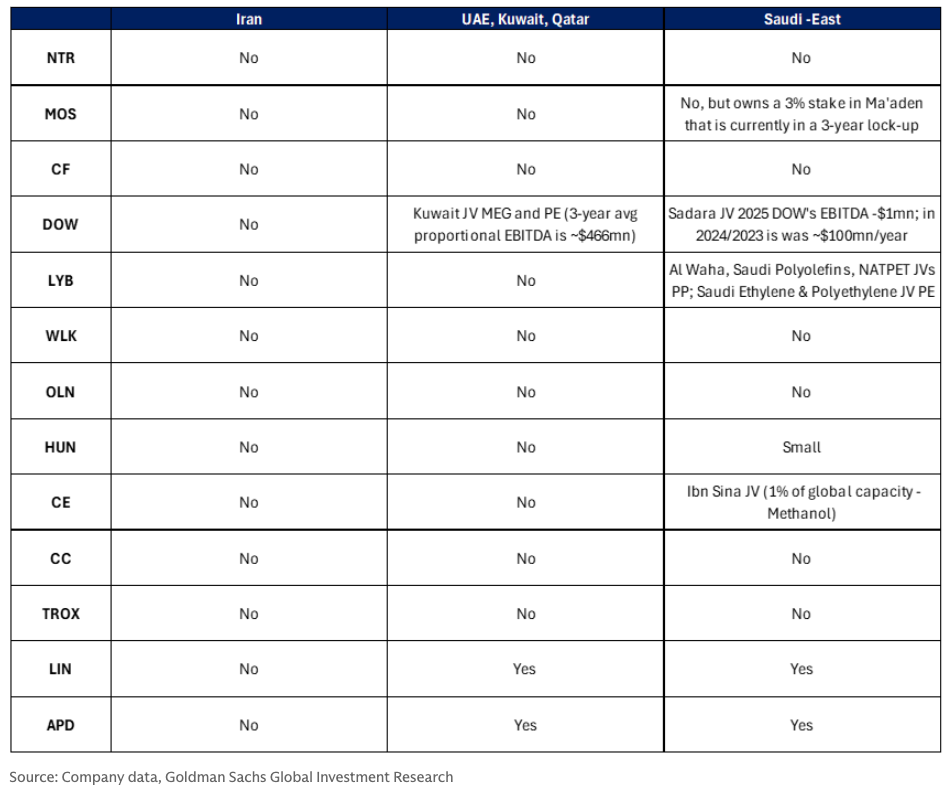

Significant amounts of competing chemical products are produced in the affected Middle East region. If this product is offline or is not able to ship then that would start to tighten global supply-demand and open up more volume opportunities for US producers. We look at three buckets of production (Iranian, UAE/Kuwait/Qatar, and Eastern Saudi Arabian). The impact on Iranian production is unclear and ships carrying production from Eastern Saudi Arabia, UAE, Kuwait, and Qatar through the Straight of Hormuz appear to be disrupted. Exhibit 1 shows the greatest impact to the least for impacted chemical chains: Nitrogen, Sulfur, Methanol, MTBE, Phosphate, Polyethylene, MDI, TiO2, Chlorovinyls. While U.S. companies are likely to be net beneficiaries, there are some U.S. companies with assets in the region that may see negative impacts. Barring any U.S. assets being kinetically impacted, the net should be positive for all U.S. chemical companies.

Exposure:

Regional Exports by Chemical Chain as a % of Global Exports

{kind=link}

Company Asset Exposure to the Middle East

{kind=link}

More in the full Goldman note (here) available to pro subs.

Tyler Durden

Wed, 03/04/2026 – 05:45