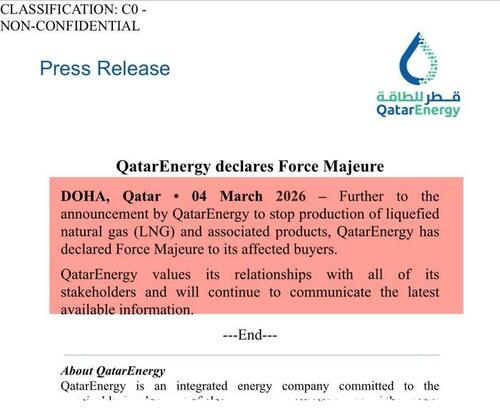

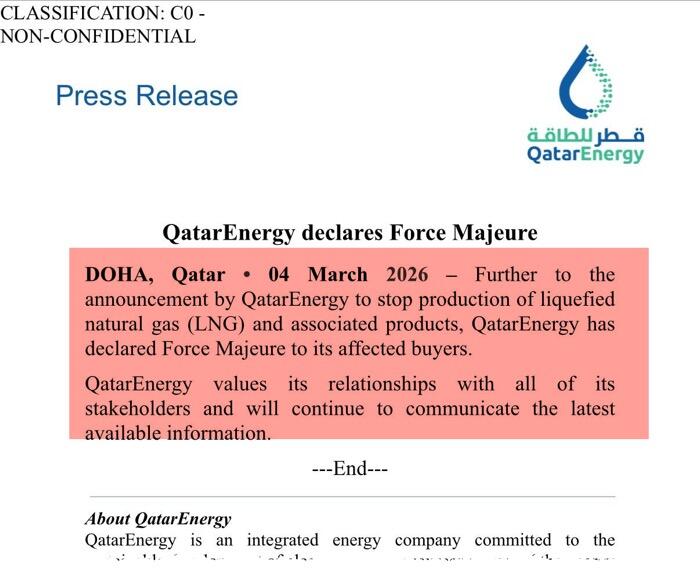

QatarEnergy Declares Force Majeure As One-Fifth Of Global LNG Supply Goes Dark

Qatar’s long-standing image as the world’s most reliable LNG supplier abruptly ended on Wednesday after QatarEnergy halted LNG production and declared force majeure to customers, a major shock to global gas markets given that Qatar accounts for 20% of global LNG exports, with 80% of those volumes to Asia.

“Further to the announcement by QatarEnergy to stop production of liquefied natural gas (LNG) and associated products, QatarEnergy has declared Force Majeure to its affected buyers,” QatarEnergy wrote in a press release on Wednesday morning.

{kind=link}

Qatar’s LNG chief Saad Sherida Al-Kaabi is confronting the biggest energy shocks of his career after an Iranian drone strike earlier this week forced the shutdown of Ras Laffan, Qatar’s top LNG export hub, for the first time in three decades.

The most immediate consequence is reputational. Wall Street analysts say the drone attack may permanently weaken Qatar’s ability to command premium gas pricing and long-term contract terms, as customers, especially in Asia, rethink their exposure to U.S. LNG in the calm warm waters of the Gulf of America.

The duration of the shutdown at the world’s leading LNG exporter is not yet known, but restarting gas liquefaction after a full shutdown can take up to two weeks, with another two weeks needed to return to full capacity. In other words, the shutdown and the time required for liquefaction plants to return to full capacity could last a month or more.

In terms of flows, Qatar’s LNG exports mostly go to Asia. The latest data shows more than 80% of Qatar’s LNG is shipped to China, India, Japan, and South Korea. Europe is also another large customer.

At the start of the week, European gas (TTF) futures nearly doubled on LNG disruptions from the Gulf area due to the Strait of Hormuz being paralyzed.

European Gas Prices Soar 50% After Qatar Shuts World’s Largest LNG Export Plant https://t.co/0Yfq1SWoXq

— zerohedge (@zerohedge) March 2, 2026

On Monday, Goldman analysts wrote (read report) that “significant upside risk to prices from a potential sustained disruption of LNG supply through the Strait of Hormuz. In a scenario where flows halt for one month, we think it is likely that TTF and JKM could approach 74 EUR/MWh ($25/mmBtu) — 130% above current levels — a threshold that triggered large natural gas demand responses during the 2022 European energy crisis.”

Vessel tracking website MarineTraffic said Wednesday morning that traffic in the critical waterway has collapsed by 90%.

“Unlike several other vessel segments where movements have largely ceased, some tankers are still travelling east and west through the strait, with a number of voyages occurring under AIS blackouts,” Kpler analyst Matt Wright wrote in a note.

Tanker traffic through Strait of Hormuz down by 90%

Analysis of vessel activity indicates tanker transits are now around 90% lower than last week. Matt Wright, Principal Freight Analyst at Kpler, explains: “Unlike several other vessel segments where movements have largely… pic.twitter.com/JIhFoAkQKO

— MarineTraffic (@MarineTraffic) March 4, 2026

Related:

US Chemical Companies “Net Beneficiaries” Of Middle East Energy Disruption Crisis

Here’s the latest from UBS analyst Nayoung Kim on “Qatar LNG, Hormuz risks”:

Upgrading 2026 global gas prices on rising geopolitical risks and uncertainty

Global gas prices are surging due to the Middle East conflicts and the effective closure of the Strait of Hormuz. The Qatari LNG production halt has pushed TTF prices to €60/MWh (about $20), with JKM seeing a modest increase to $13.5/mmBtu. Although Qatar sends >70% of its exports to Asia, market reactions suggest Europe as the main concern. How much and how long prices rise depends on the extent and duration of disruptions; our revised forecasts assume disruptions could persist for next 1-2 weeks. Given a tight market, any disruption may cause widespread effects, leading to elevated prices in 2026. We raise TTF to €38 in 1Q26E, €37 in 2Q26E, and €35 on average for 2026E. JKM revised up to $14 in 1H26E and $13 in 2026E. US Henry Hub is less affected but rising US LNG demand may push prices up to $5.00 in 1Q26E, then down to $3.15 in 2Q26E, averaging $4 for 2026E. Longer-term forecasts unchanged (see Figure 1).

How much gas has been impacted so far?

Currently, nearly 140bcm of gas supply is either disrupted or at risk. 1) 118bcm from Middle Eastern LNG exports: Qatar accounts for 110bcm, and the UAE adds 8bcm, together representing 21% of total LNG flows. 2) 10bcm of gas exports from Israel to Egypt have been completely halted. 3) 10bcm of pipeline supply from Iran to Turkey is also at risk. Given the significant volumes involved, markets remain focused on the duration and impact of Qatar’s suspension.

What are the alternatives?

Spare capacity remains limited. The US could increase production in response to prices, but has little room for growth (Figure 15). We see Russian piped gas as the feasible option with capacity of >130bcm but faces political barriers (link). Short disruptions may be offset by later ramp-ups, but persistent supply issues may be hard to resolve without new capacity. Golden Pass start-up is near, yet the project will steadily boost output. It is too early to say the situation mirrors the 2022 energy crisis, yet we cannot dismiss the possibility of additional shocks. The previous supply shortfall was offset equally by reduced demand and increased LNG supply, but now there is little scope for such move.

Are flows shifting? or stalling? how importers to react?

Despite only 7% of Qatar’s exports going to Europe, Europe faces more pressure due to low storage, limited alternatives, and potential for greater competition for spot cargos with Asia. Pre-disruption, EU storage was estimated at 26% by end-March. The ongoing disruption from Qatar throughout March could bring a loss of up to 1bcm. Given Qatar’s monthly exports to Asia (excl. China) reaching 4–5bcm, if these buyers enter the spot market, storage levels could drop further toward 20%. China is less vulnerable given its other fuel/supply options and natgas storage. We expected Europe to need an 8% y/y increase in LNG imports (see our Jan outlook), which may now be even more with Qatar and other disruptions, making the impact most pronounced.

A wide range of outcome and prices; upside risks remain

Uncertainty around Middle East tensions may cause significant volatility in prices, with risks skewed to the upside while conflicts persist. Iran’s attacks on Qatari LNG/energy facilities could drive prices >€100 (or $30) if they escalate. With limited alternatives, prices may stay higher for longer in that case, with potential demand adjustments as situation develops. If US/Israeli operations conclude and Iran ceases attacks soon, risk premiums could drop quickly, lowering prices to ~€30s (or $10-11) as weather gets mild.

The full note can be viewed here and is available to pro subs.

Beyond Qatar, Iraq has shut in 460,000 barrels per day of production at the West Qurna 2 field and will likely be forced to cut more than 3 million bpd if the Strait of Hormuz remains paralyzed. President Trump has offered insurance and U.S. military escorts in an effort to unfreeze the critical maritime energy chokepoint.

China’s massive exposure to cheap energy from Iran and other Gulf nations has infuriated Beijing, and Foreign Minister Wang Yi said that his government will send a special envoy to the Middle East for mediation. China really needs the strait to remain open

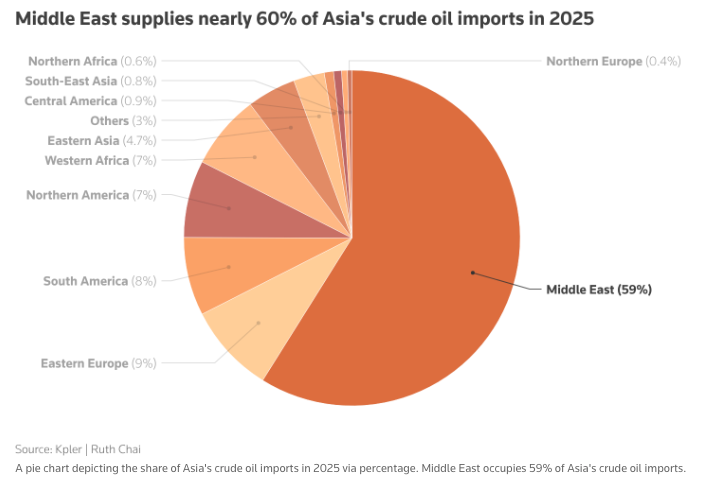

China, the world’s biggest crude importer, sources about half of its seaborne imports – or 5.4 million bpd – from the Middle East.

{kind=link}

If the Strait of Hormuz stays disrupted for an extended period, China would take a meaningful energy and industrial hit, first through soaring energy prices, then through supply woes, and ultimately through an economic growth hit. It is increasingly clear that Beijing will do everything in its power to keep the strait open and pressure Tehran to avoid a prolonged shutdown. All of this comes before Trump heads to Beijing.

Tyler Durden

Wed, 03/04/2026 – 11:20