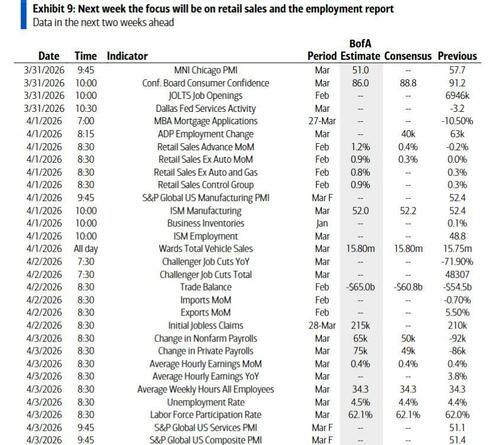

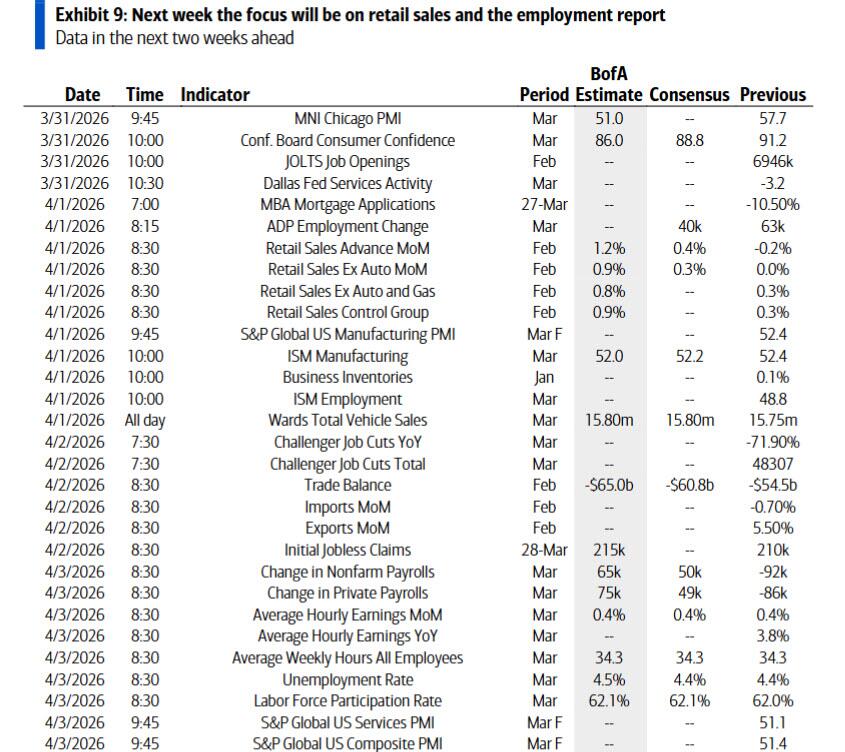

Key Events This Holiday-Shortened Week: Payrolls, PMI, ISM, Retail Sales And Fed Speech

Looking at the week ahead, we should start to learn about the economic consequences of the conflict, as several data releases for March are out which cover the period since the strikes began on February 28.

In the US, that includes the monthly jobs report on Friday – which falls on a Holday when stocks are closed, while bonds are open for half a day – where economists expect nonfarm payrolls to have risen by +60k in March. As a reminder, US payrolls have been pretty choppy in recent months, and on the current series of revisions they’ve been oscillating between positive and negative readings for every month since May. Last month they were down -92k, but some of that weakness was a function of a strike at a major healthcare company that’s since ended, along with severe weather that may have temporarily depressed February’s payrolls. So while DB economists are expecting a positive payrolls print for March, they think the unemployment rate will round up to 4.5% given how close it was last month (4.44%).

Otherwise in the US, the focus will be on whether higher oil prices have started to impact business sentiment and inflation in a meaningful way. So the ISM manufacturing will be in the spotlight, including the prices paid component for whether the inflationary impact has started to filter through. Before that, we’ll also get the Conference Board’s consumer confidence reading tomorrow.

{kind=link}

Speaking of inflation, the main highlight in Europe will be tomorrow’s flash CPI print for the Euro Area, which is an important one as the ECB work out what to do. To be fair, the flash print from Spain last Friday was weaker than expected, at +3.3% (vs. +3.8% expected), so that’s slightly eased fears about a very strong print tomorrow. Nevertheless, even with the Spanish number, DB’s European economists are still tracking the Euro Area CPI print at +2.53% year-on-year, up from +1.89% in February, a number which was reinforced with today’s regional German CPI update for March.

Elsewhere this week, there isn’t too much on the calendar of events as we move towards Easter. Indeed, markets will be closed in several countries at the end of the week for Good Friday. However, we will hear from a few central bankers, including Fed Chair Powell later today, who’s speaking in a discussion at Harvard University.

Courtesy of DB, here is a day-by-day calendar of events

Monday March 30

Data: US March Dallas Fed manufacturing activity, February net consumer credit, M4, Germany March CPI, Italy February PPI, Eurozone March economic confidence

Central banks: Fed’s Powell and Williams speak, ECB’s Stournaras speaks

Tuesday March 31

Data: US March Conference Board consumer confidence index, MNI Chicago PMI, Dallas Fed services activity, February JOLTS report, January FHFA house price index, China March official PMIs, UK Q4 current account balance, Japan March Tokyo CPI, February jobless rate, job-to-applicant ratio, retail sales, industrial production, housing starts, Germany March unemployment claims rate, February retail sales, import price index, France March CPI, February PPI, consumer spending, Italy March CPI, January industrial sales, Eurozone March CPI, Canada January GDP

Central banks: Fed’s Goolsbee, Barr and Bowman speak, ECB’s Panetta, Muller, Sleijpen and Kazimir speak, RBA minutes of the March meeting

Earnings: Nike

Other: French President Macron visiting Japan, through April 2

Wednesday April 1

Data: US March ISM index, ADP report, total vehicle sales, February retail sales, January business inventories, China March RatingDog manufacturing PMI, Japan BoJ’s Tankan survey, Italy March manufacturing PMI, new car registrations, February unemployment rate, Eurozone February unemployment rate, Canada March manufacturing PMI

Central banks: Fed’s Musalem and Barr speak, ECB’s Cipollone speaks, BoC’s summary of deliberations

Thursday April 2

Data: US February trade balance, initial jobless claims, Japan March monetary base, France February budget balance, Italy February retail sales, Canada February international merchandise trade, Switzerland March CPI

Central banks: ECB’s economic bulletin, BoE’s DMP survey

Friday April 3

Data: US March jobs report, China March RatingDog services PMI, France February industrial production

Central banks: ECB’s Radev speaks

Other: Good Friday

Looking at just the US, Goldman writes that the key economic data releases this week are the retail sales report on Wednesday and the employment report on Friday. There are several speaking engagements by Fed officials this week, including events with Chair Powell and New York Fed President Williams on Monday.

Monday, March 30

10:30 AM Fed Chair Powell speaks: Fed Chair Jerome Powell will participate in a moderated discussion at Harvard University. Moderated and audience Q&A are expected. On March 18th, Chair Powell said that the risks to employment and inflation are on an equal footing, saying that he would “be hard-pressed to say that one of them is obviously more at risk than the other.” He added that he takes seriously the risk from the oil price shock to inflation expectations against a backdrop where inflation has been high for five years. In light of this, he said, “the framework calls to balance the risks,” and a “mildly restrictive” stance or the “higher borderline of restrictive versus not restrictive” is “the right place to be.”

04:00 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will speak at the Staten Island Economic Development Corporation. Speech text and moderated Q&A are expected. On March 3rd, President Williams said that “monetary policy is currently well positioned to support the stabilization of the labor market and return inflation to our 2% goal,” adding that “in recent months there have been promising signs of stabilization in the labor market.”

Tuesday, March 31

09:00 AM S&P Case-Shiller 20-city home price index, January (GS +0.3%, consensus +0.4%, last +0.5%)

09:00 AM FHFA house price index, January (consensus +0.1%, last +0.1%)

10:00 AM Conference Board consumer confidence, March (GS 86.5, consensus 88.0, last 91.2)

10:00 AM JOLTS job openings, February (GS 7,000k, consensus 6,890k, last 6,946k): We estimate that JOLTS job openings were roughly unchanged month-over-month in February at 7.0mn based on the signal from online measures of job postings from Indeed and LinkUp. Since the end of February, those measures have declined by roughly 2% on average.

12:00 PM Chicago Fed President Goolsbee (FOMC non-voter) speaks: Chicago Fed President Austan Goolsbee will give opening remarks at a Chicago Fed Mobility Project virtual event. On March 24th, President Goolsbee said that “we could be back to the environment with multiple rate cuts for the year, if inflation behaves,” but added that “I could see circumstances where we would need to raise rates if it was going a different way and inflation was getting out of control.”

03:00 PM Fed Governor Barr speaks: Fed Governor Michael Barr will discuss stablecoin regulation at a Federalist Society virtual event. Speech text and moderated and audience Q&A are expected. On March 26th, Governor Barr said that “given the considerable uncertainty about the potential effects of developments in the Middle East on our economy, as well as other factors, it makes sense to take some time to assess conditions,” adding that “our current policy stance puts us in a good place to hold steady while we evaluate the incoming data.”

05:10 PM Fed Vice Chair for Supervision Bowman speaks: Fed Vice Chair for Supervision Michelle Bowman will speak on small businesses at the 2026 Consumer Bankers Association Live conference in San Diego. Speech text and moderated Q&A are expected. On March 20th, Vice Chair for Supervision Bowman said that she has “written three cuts before the end of 2026 to hopefully support the labor market,” and noted that “it is too soon to tell what the impacts of the conflict with Iran will be.”

Wednesday, April 1

08:15 AM ADP employment change, March (GS +40k, consensus +40k, last +63k)

08:30 AM Retail sales, February (GS +0.6%, consensus +0.5%, last -0.2%); Retail sales ex-auto, February (GS +0.5%, consensus +0.3%, last flat); Retail sales ex-auto & gas, February (GS +0.6%, consensus +0.3%, last +0.3%); Core retail sales, February (GS +0.5%, consensus +0.3%, last +0.3%): We estimate core retail sales increased 0.5% in February (ex-autos, gasoline, and building materials; month-over-month SA), reflecting solid alternative data. We estimate headline retail sales increased 0.6%, reflecting a rebound in auto sales.

09:05 AM St. Louis Fed President Musalem (FOMC non-voter) speaks: St. Louis Fed President Alberto Musalem will speak on the economy and monetary policy at the American Enterprise Institute in Washington, DC. Speech text and moderated Q&A are expected.

09:10 AM Fed Governor Barr speaks: Fed Governor Michael Barr will discuss AI and consumer issues at the National Fair Housing Alliance symposium in Washington, DC. Moderated Q&A is expected.

09:45 AM S&P Global US manufacturing PMI, March final (consensus 52.4, last 52.4)

10:00 AM ISM manufacturing index, March (GS 53.0, consensus 52.4, last 52.4): We estimate that the ISM manufacturing index increased by 0.6pt to 53.0 in March, reflecting sequential improvement in regional manufacturing surveys but a slight headwind from potential residual seasonality. Our manufacturing survey tracker increased by 1.1pt to 53.6.

05:00 PM Lightweight motor vehicle sales, March (GS 16.0mn, consensus 15.9mn, last 15.8mn)

Thursday, April 2

08:30 AM Trade balance, February (GS -$50.0bn, consensus -$60.0bn, last -$54.5bn): We forecast that the trade deficit narrowed by $4.5bn to $50.0bn in February, reflecting an increase in gold exports that was partially offset by an increase in goods imports from China.

08:30 AM Initial jobless claims, week ended March 28 (GS 205k, consensus 212k, last 210k): Continuing jobless claims, week ended March 21 (consensus 1,830k, last 1,819k)

Friday, April 3

US equity markets will be closed in observance of Good Friday, while SIFMA recommends an early close at 12 PM for the bond market.

08:30 AM Nonfarm payroll employment, March (GS +70k, consensus +60k, last -92k); Private payroll employment, March (GS +75k, consensus +70k, last -86k); Average hourly earnings (MoM), March (GS +0.3%, consensus +0.3%, last +0.4%); Unemployment rate, March (GS 4.4%, consensus 4.4%, last 4.4%): We estimate nonfarm payrolls increased 70k in March. On the positive side, we expect a 32k boost from the end of worker strikes and a moderate tailwind from sequentially better weather after it likely weighed on February payroll growth. The big data indicators we track were mixed in March. On the negative side, we expect a 5k decline in government payrolls—reflecting a 10k decline in federal government payrolls that is partly offset by a 5k increase in state and local government payrolls. We estimate that the unemployment rate was unchanged on a rounded basis at 4.4% in March, reflecting the stabilization in continuing claims over the last month. That said, the bar for rounding up to 4.5% is not high from an unrounded 4.44% in February. We estimate average hourly earnings rose 0.3% month-over-month in March, reflecting neutral calendar effects.

09:45 AM S&P Global US services PMI, March final (consensus 51.1, last 51.1)

Source: DB, Goldman

Tyler Durden

Mon, 03/30/2026 – 10:15