JPM’s Dimon Warns Of “Skunk At Party,” Talks Credit Cycles, Touts U.S. Military Power

JPMorgan CEO Jamie Dimon began his annual shareholder letter on Monday by tying the bank’s legacy to the nation’s history: “In 2026, America is celebrating its 250th anniversary. This year, we are also celebrating the 227th anniversary of JPMorgan Chase, which was founded in April 1799.”

{kind=link}

Quick Summary

Dimon used his annual letter to tout another year of record financial results, while warning that investors may be underestimating the risks building across the global economy. These risks include the U.S.-Iran conflict entering its second month, trade negotiations that exacerbate geopolitical tensions, the convergence of surging oil prices and inflation, and elevated asset prices.

Touting 2025 JPM Results

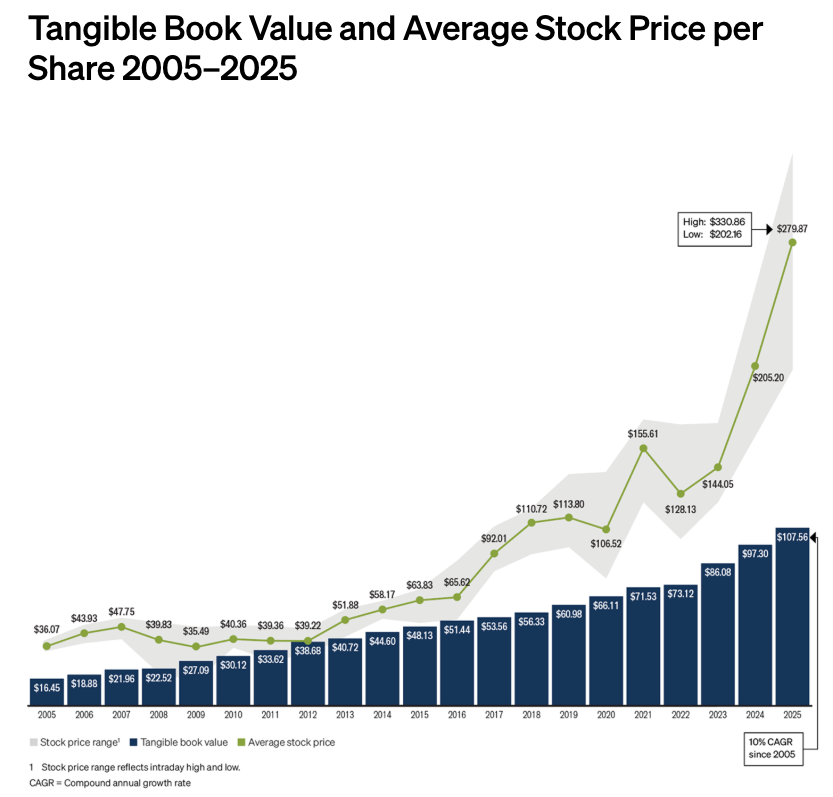

The largest U.S. bank said 2025 revenue rose to a record $185.6 billion, while net income reached $57 billion and return on tangible common equity (ROTCE) was 20%. JPM also lifted its quarterly dividend twice during the year, to $1.50 a share from $1.25, as it continued to note the strength of its balance sheet.

{kind=link}

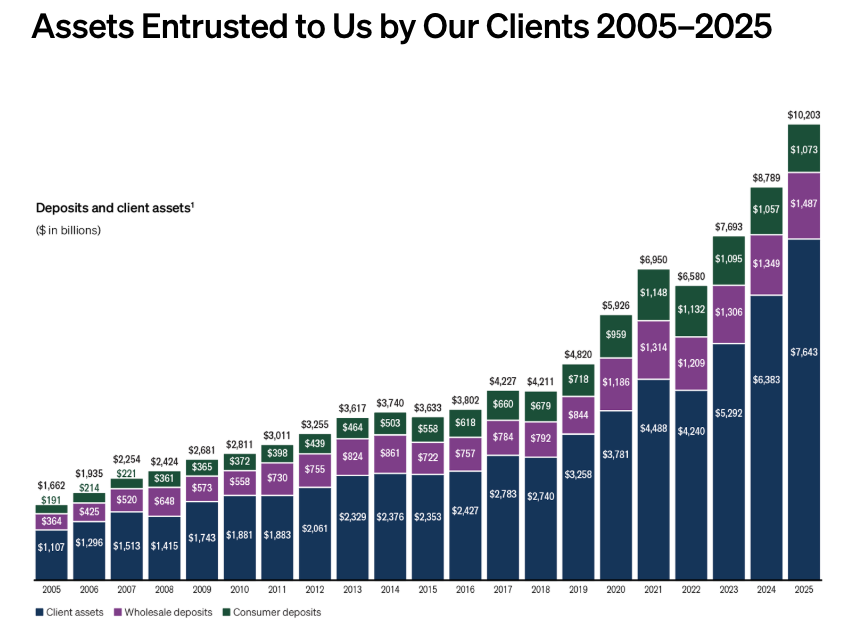

The letter also highlighted JPMorgan’s significant role in the US and global economies. Dimon said the bank extended credit and raised capital totaling $3.3 trillion in 2025, moves nearly $12 trillion a day across more than 120 currencies and 160 countries, and safeguards more than $41 trillion in assets.

{kind=link}

Risks

Beyond the numbers, Dimon warned about “some scenarios that would result in a recession, which generally reduces inflation, and other scenarios that would lead to a recession with inflation (stagflation—where inflationary forces overcome deflationary ones).”

He said the “skunk at the party” could emerge this year and “would be inflation slowly going up, as opposed to slowly going down,” adding, “This alone could cause interest rates to rise and asset prices to drop. Interest rates are like gravity to almost all asset prices. Falling asset prices at one point can change sentiment rapidly and cause a flight to cash.”

Tailwinds

However, Dimon pointed out, “there are lots of tailwinds helping the U.S. in 2026, including:

Increasing fiscal stimulus from the One Big Beautiful Bill. Our economists believe this will inject another $300 billion (effectively 1% of GDP) into the economy. This has to be very modestly inflationary this year.

Benefits from the Fed’s purchase of $40 billion of additional securities each month, which is supposed to be reduced to $20 billion–$25 billion this April. At a minimum, this supports asset prices and helps ensure there is no liquidity squeeze in the financial system.

Positive effects of comprehensive deregulatory policies. This was badly needed and long overdue. Change is clearly evident in bank regulations that will free up capital and liquidity, which can be lent out (and we already see this happening), and in deregulation across many other industries, from energy to home building. It is fair to say that actions taken have clearly increased confidence and animal spirits. This should add to productivity and be modestly deflationary this year.

Huge increase in AI-driven capital spending and construction by the five hyperscalers. In 2025, this number was $450 billion, and in 2026, it will be approximately $725 billion. While AI will clearly drive productivity, which is generally good for inflation in the long run, all of this spending is probably inflationary in the short run.

Larger Risks

He warned of a series of unresolved “larger risks” shifting beneath the surface of the economy, “like tectonic plates—always moving and periodically causing earthquakes and volcanoes when they crash into each other.”

Those larger risks include:

First and foremost, geopolitics. Russia’s war in Ukraine and its ongoing sabotage in Europe and now the war in Iran and its potential effects on energy prices can cause events that are unpredictable. We all hope these wars get properly resolved. But war is the realm of uncertainty, as each side in a war determines what it wants to do (as is often said, “the enemy gets a vote”), and these conflicts involve many countries. Not only do they have a major impact on the nations at war, but they also have an impact on countries and economies across the globe that are not directly involved in war. Nations that are heavily dependent upon imported energy are already seeing the effects. And it’s not just energy, it’s commodity products that are byproducts of oil and gas, like fertilizer and helium. And given our complex global supply chains, countries are experiencing disruptions in shipbuilding, food and farming, among others. The outcome of current geopolitical events may very well be the defining factor in how the future global economic order unfolds — then again, it may not.

High global sovereign deficits and debt. Global deficits are significantly elevated, particularly during what has been a relatively healthy global economy and, until recently, a time of peace — the deficit globally is at an extremely high 5%, while global sovereign debt is at all-time highs. The current forecast from the Congressional Budget Office has our debt-to-GDP ratio going from 100% today to 120% in 2036. High government debt is somewhat offset by low consumer debt, which was nearly 100% of GDP in 2007 and is now below 70%. Similarly, corporate debt is at a fairly normal healthy level of 45%. High and increasing government debt will eventually have to be dealt with — the right way would be to deal with it now before it becomes a problem; the wrong way would be to let it become a crisis, which, in my opinion, is probably the likely outcome. Importantly, almost 60% of government spending is for entitlements and is not discretionary. This makes the job that much harder. A crucial note on the importance of growth: If interest rates went down 100 basis points and GDP grew at 3%, the debt-to-GDP ratio could actually start to go down instead of going up.

High asset prices and very low credit spreads. In and of itself, this is not a bad thing. Household net worth as a percentage of GDP is now 560%. The high during the housing peak in 2006 was 460%. But this also means that anything less than positive outcomes could have a dramatic impact on global markets. Rapidly decreasing asset prices can sometimes create a self-reinforcing loop. It’s always good to remember that prices are set by the marginal buyers and sellers — which, on the average day, is only a small fraction of asset owners. And it’s also good to remember that foreigners own almost $30 trillion of U.S. equities and bonds. While U.S. investments and the U.S. dollar are generally havens of security in a troubled world, that didn’t stop recessions and bad markets in prior times.

Trade 2.0. The U.S. tariffs themselves had only minor effects on inflation or growth, and were only one straw on the camel’s back. But the trade battles are clearly not over, and it should be expected that many nations are analyzing how and with whom they should create trade arrangements. This is causing a realignment of economic relations in the world. While some of this is necessary for national security and resiliency, which are paramount, it is hard to figure out what the long-term effects will be.

U.S. and China relations. This relationship is critical to the whole world and is also impacted by the events mentioned above. The United States and China clearly have different systems, values, goals and objectives, and while both sides are currently engaging, we have to expect that there will be some bumps in the road — maybe even some large ones. We should all hope that ongoing proper engagement continues to lead to what may be a competitive but peaceful future.

Private credit and credit in general. The leveraged private credit market totals $1.8 trillion. As a comparison, the U.S. high yield bond market totals $1.5 trillion, and the bank syndicated leveraged loan market totals $1.7 trillion. Taking a wider view, the total market size of investment grade bonds is $13 trillion. And the total market value of all residential mortgage securities and loans is also $13 trillion. In the great scheme of things, private credit probably does not present a systemic risk.

Credit Cycle

Dimon continued, “I do believe that when we have a credit cycle, which will happen one day, losses on all leveraged lending in general will be higher than expected, relative to the environment.” We’ve been extensively tracking the cracks emerging across credit (latest here).

Geopolitics

On the topic of what appears to be Eurasia on fire, with multiple warzones raging, Dimon emphasized three critical issues about preserving the American empire:

The United States must maintain the premier military force in the world.

The United States must maintain its preeminent economic position in the world, which also requires reigniting the American Dream.

The United States must manage its foreign economic affairs to strengthen the U.S. economy and that of our critical allies so that the first two points remain true.

US Military & American Empire

All about the empire… Dimon said, “We at JPMorganChase feel an enormous responsibility to our nation and many others — and we remind ourselves that many companies will only thrive if their countries thrive. With the right policies and committed actions, the United States will maintain the strongest military and strongest economy and will remain the bastion of freedom and the arsenal of democracy.”

Dimon, who turned 70 in early March, has transformed JPMorgan into the nation’s largest and most profitable bank, making it one of the core pillars of the U.S. financial system. This year’s annual letter carries a warning that the world is becoming more fractured and, in at least one key region, engulfed in war. The broader message is unmistakable: American power is supreme, and JPMorgan intends to help preserve the empire for decades to come.

Tyler Durden

Mon, 04/06/2026 – 08:10