Blue Owl Stock Slides After Moody’s Cuts Outlook To “Negative” On Surging Redemption Requests

Blue Owl stocks is getting slammed this morning, erasing all early gains, after Moody’s Ratings cut its outlook on a $36-billion Blue Owl non-traded fund to “negative” from “stable” on Tuesday, citing redemption requests that were significantly higher than at peers in the first quarter. Moody’s also said the change in the outlook on Blue Owl Credit Income Corp (OCIC) is due to the majority of the redemption requests coming from a very limited number of investors, revealing some concentration in the equity-holder base.

The downgrade highlights the mounting strains in the $2 trillion private credit industry after a strong run, as jittery retail investors bail out amid rising concerns around transparency, lending standards and valuations.

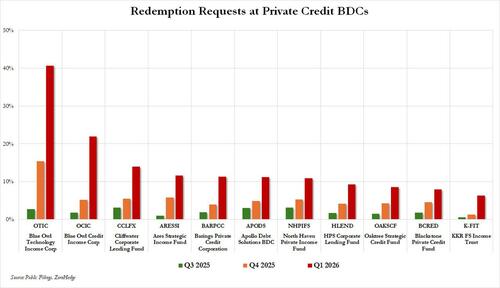

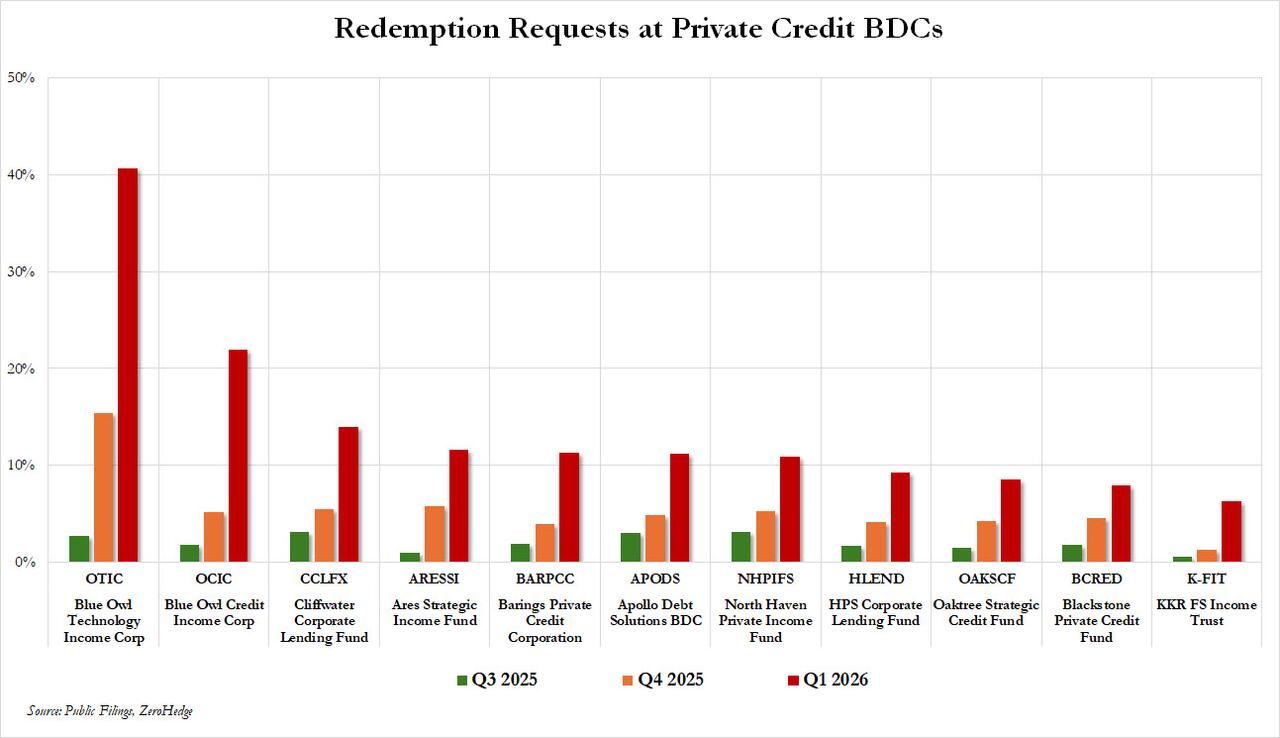

As we noted recently, having started the firesale in the private credit in February, the decision has since backfired on Blue Owl, leading to an unprecedented surge in redemptions, which hit a record 40.7% for the Blue Owl Technology Income Corp, and 22% for the Blue Owl Credit Income Corp.

{kind=link}

In response, OCIC, Blue Owl’s biggest business development company (BDC), had said about 90% of the investors did not request to redeem in the first quarter, which, however, is precisely one of the main concerns for Moody’s which cautioned about concentration risk. OCIC investors sought to redeem 21.9% of shares in the first quarter, significantly higher than the 5.2% redemption requests received in the fourth quarter.

Moody’s said it expects elevated redemptions to persist in the coming quarters and inflows could slow further, resulting in the dissipation of OCIC’s currently strong capital and liquidity positions.

Blue Owl has previously said there was a “meaningful disconnect” between public sentiment on private credit funds and the underlying performance of its portfolio, although as we explained previously, the company may be simply delaying the inevitable asset remarking as a mere 20% drop in underlying asset values would breach key regulatory ratios.

{kind=link}

Earlier on Tuesday, Moody’s had revised its outlook on US all BDCs to “negative” from “stable”, citing rising redemption pressures, higher leverage and weakening access to funding markets.

Non-traded perpetual BDCs, like OCIC, have grown rapidly in the past few years as alternative asset managers aggressively expanded in the wealth channel and focused on retail and high-net-worth investors, who are increasingly buying private assets.

But retail investors tend to be less patient and predictable compared to institutional investors during periods of volatility.

Such investment vehicles offer lower volatility compared to publicly traded BDCs, but investors have to contend with lower liquidity.

As we have repeatedly discussed, Blue Owl has become the poster child for private credit funds that are struggling with an elevated level of redemptions. Its stock has more than halved over the past 12 months and is trading near record low, and on Wednesday it reversed all early gains and was trading down 1%, if still above its record lows hit last week.

{kind=link}

Its handling of some of its private credit funds in recent months also attracted intense scrutiny and raised concerns about liquidity for such vehicles.

Blue Owl had last year planned to merge its publicly traded fund Blue Owl Capital Corp with a non-public fund called Blue Owl Capital Corp II, but called off the deal after a plan to freeze withdrawals ahead of the transaction rattled investors.

The firm earlier this year replaced quarterly redemptions at OBDC II with promised payouts. It also sold $1.4 billion in assets from three of its credit funds to a consortium of investors which included an affiliated insurer, to return capital to investors and pay down debt. Concerns promptly emerged that the less than “arms length” transaction had cherry picked the best assets, leaving investors stuck with underperforming software exposure.

OBDC II is a finite-life non-traded BDC and the fund was due to give a full liquidity event to investors within three-to-four years of the completion of its public offering, which runs through 2026.

Last month, S&P Global revised the outlook on Cliffwater’s $33 billion flagship private credit fund to “negative” over higher investor redemption requests.

Tyler Durden

Wed, 04/08/2026 – 13:25