Another 2008 Analog: Goldman, JPM Offering Hedge Funds Ways To Short Private Credit

The big story last week, a narrative which we may have inadvertently started, was the recurring comparison across various sellside desks (and quite a few buysiders) of the current double crisis (private credit as an analog to the subprime crisis of 2007/2008 coupled with soaring oil prices which peaked at just below $150 in the summer of 2008 before crashing along with the start of the global financial crisis, similar to now). None other than Michael Hartnett dedicated his latest Flow Show to describing how “Wall Street Is Ominously Trading The 2008 Analog.”

Well, we now have another very stark comparison to events from 2008.

Recall back then, while big banks like Goldman were actively pitching long RMBS trades to clients, seemingly oblivious of the subprime risk, they were quietly arranging transactions for their best clients – such as Paulson and Magnetar – to short the entire RMBS/housing stack in advance of the subprime explosion that would spark the global financial crisis. In fact, it was this trade that make Paulson a billionaire (and some might add, a one hit wonder).

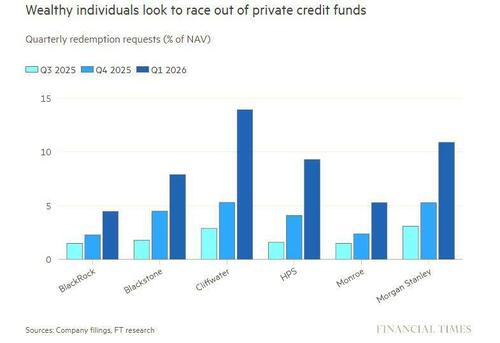

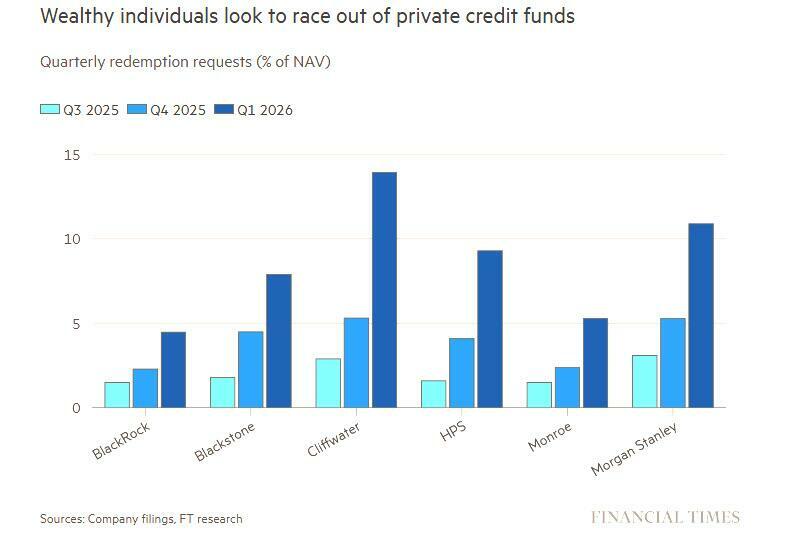

While subprime was the crisis catalyst in 2008, this time around almost everyone agrees that ground zero of the next credit crisis will be the $1.8 trillion private credit market, which as we have described extensively, is in dire straits (with all due respect to Hormuz) as a result of not only the panicked surge in redemptions on a sudden revulsion to the asset class which has prompted numerous funds to impose gates…

{kind=link}

… but also what Boaz Weinstein described as the “massive declines in everything from OTF, TCPC, FSK, OXLC, BPRE, the tripling of outflows for Cliffwater and Blue Owl, the frauds, the rise in bad PIK, the mis-labeling of Saas, the embellishment of what portion of the portfolios are true 1L, and a whole lot more.“

I’m genuinely interested in everyone’s thoughts. IMHO, what’s stoking fear @AcaciaCap isn’t our bid but the massive declines in everything from OTF, TCPC, FSK, OXLC, BPRE, the tripling of outflows for Cliffwater and Blue Owl, the frauds, the rise in bad PIK, the mis-labeling of… https://t.co/lw29B9jJc3

— boaz weinstein (@boazweinstein) March 14, 2026

And it is private credit that the big banks are now quietly aiding their best clients to short, even as they publish report after report talking how the selling in private credit is irrational and should reverse.

According to Bloomberg, Goldman and JPMorgan are among investment banks offering hedge fund clients ways to bet against the $1.8 trillion private credit markets, having assembled baskets of listed companies with exposure to the space.

Goldman’s indexes vary from one focused on European financial institutions with private credit exposure to a group of business development companies and another alternatives managers more broadly. JPMorgan’s basket meanwhile includes alternatives managers and BDCs, Bloomberg’s sources said. Clients can also invest in the indices.

Meanwhile, Bank of America has a basket of European financial firms with exposure to private credit, including Partners Group, Deutsche Bank and Axa. The Financial Times reported earlier on Thursday that the bank had since awkwardly withdrawn a recommendation that clients bet against European companies potentially exposed to private credit shocks.

Why: because the bank doesn’t want to get in trouble with European regulators who know very well that any push to tip over the private credit house of cards could lead to the next credit crisis, one which would almost certainly drag Europe’s debt-challenged states in as well.

And just to make the 2008 analog complete, separately Bloomberg reports that another branch of Goldman, the bank’s Asset Management division, has begun preliminary talks with investors to raise at least $10 billion for a global direct lending fund.

The fund, West Street Loan Partners VI, will focus on companies across North America, Europe and Australia, typically targeting businesses generating more than $100 million in EBITDA. Its predecessor fund raised over $13 billion in 2024.

Goldman is targeting returns of between 10%-12% on a levered basis for the fund, and 6%-7% on an unlevered basis, Bloomberg’s sources said. At least 80% of the portfolio is expected to consist of senior loan positions.

In other words, Goldman’s trading desk is helping and arranging for its hedge funds clients sell and short exposure to private credit while another division of Goldman (one which is supposedly behind a Chinese Wall) is actively soaking up everything that is for sale, at a sizable discount of course. One can hardly wait for the 2028 Congressional hearings on the topic.

* * * Top selling supplements (in stock)

Brain Rescue (on sale!)

Iodine Fortify (are you deficient?)

Resveratrol (potent antioxidant for healthy aging)

Tyler Durden

Thu, 03/19/2026 – 13:40