Conrad Nichols, a senior energy storage technology analyst at market intelligence firm IDTechEx, previews some of the key findings from a new report.

The Li-ion battery (LIB) recycling market has continued to grow rapidly through players establishing new partnerships, securing supply deals, and gathering large volumes of funding. Key players have also persisted with constructing new commercial-scale facilities utilizing mechanical, hydrometallurgical, and pyrometallurgical recycling technologies. These technologies are well understood and are increasingly being used at commercial-scale to produce intermediary products for new Li-ion battery production, such as black mass, battery-grade metal salts, precursor cathode active material (pCAM), and CAM.

However, these technologies struggle to economically recycle lower-value LFP cathodes. With the increasing penetration of this chemistry in electric vehicle (EV) and battery energy storage system (BESS) markets, the long-term development of direct Li-ion battery recycling technologies will be crucial, given their proposed production of cheaper recycled cathode material. Moreover, traditional LIB recycling technologies have focused on recovering high-value cathode materials, such as lithium, nickel, and cobalt. Recyclers could capitalize on commercializing battery-grade graphite recycling technologies to increase the overall value that could be extracted from recycling LIBs. In the market report, “Li-ion Battery Recycling Market 2025-2045: Markets, Forecasts, Technologies, and Players”, IDTechEx forecasts that the Li-ion battery recycling market will be valued at US$52B in 2045, based on the value of materials that could be extracted from available end-of-life (EOL) LIBs and manufacturing scrap. Importantly, however, continued innovation and advancements in direct LIB recycling and battery-grade graphite recycling technologies will be needed for this full value to be captured.

Advances in direct Li-ion battery recycling technologies: commercial activity, challenges, and prospects

It is widely known that LIBs adopting ternary chemistries such as NMC (nickel manganese cobalt oxide) are more profitable to recycle than LFP chemistries due to the inclusion of nickel and cobalt in the cathode. However, LFP chemistry demand is increasing within both EV and BESS markets, where prioritizations on cost, safety, and cycle life may be seen depending on the application. Therefore, pressure is starting to mount for the development of more economic recycling technologies, which would greatly benefit LFP recycling. Namely, this could include direct LIB recycling technologies.

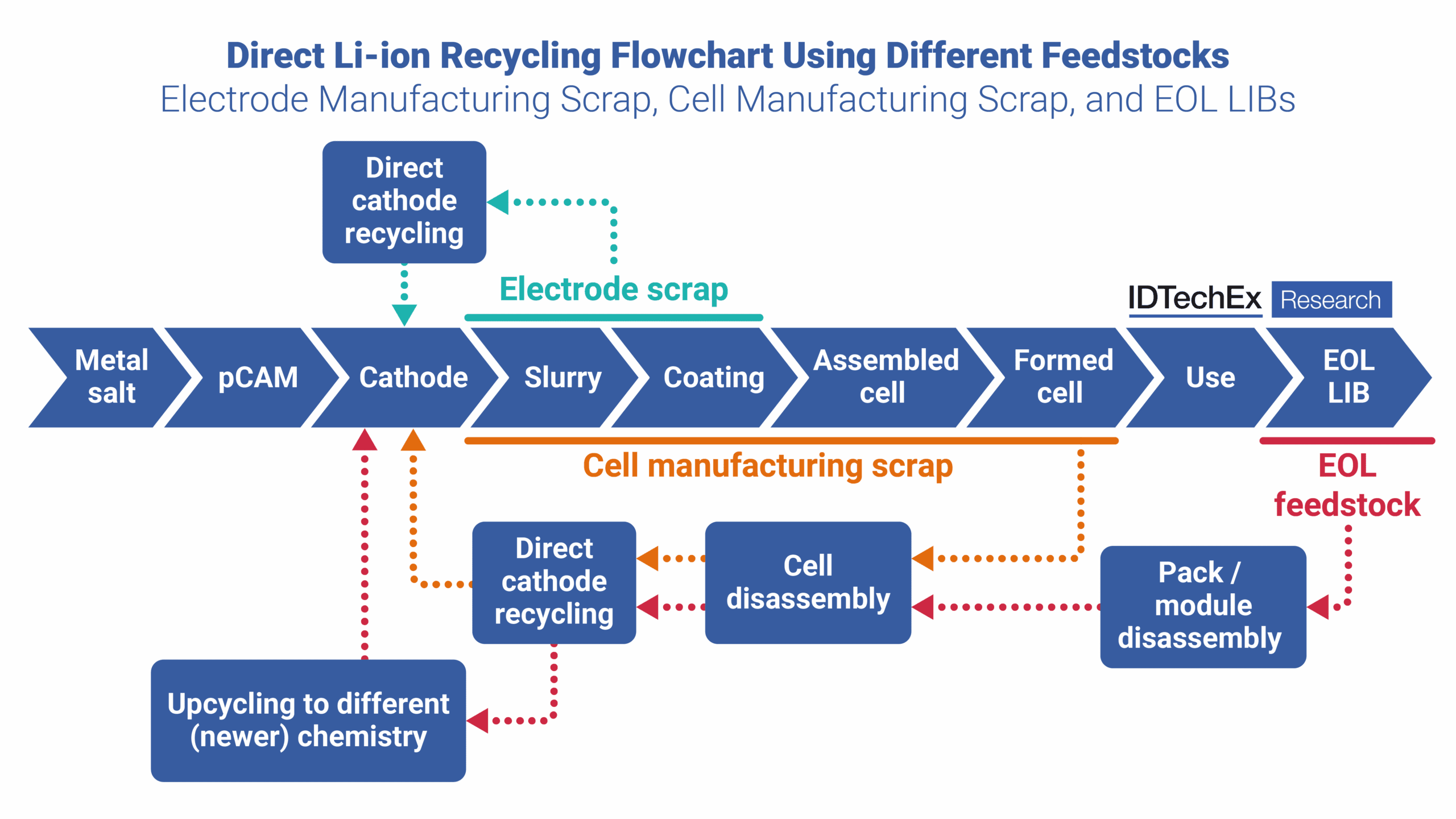

Direct recycling involves reactivating the battery material to recover capacity lost during cycling. Unlike pyro- and hydrometallurgical methods, the crystal structure of Li-ion cathodes is prevented from being broken down. If the CAM is repairable, it can be relithiated via a range of techniques, including thermal, hydrothermal, and electrochemical processes.

Direct recycling technologies being developed could offer a cheaper alternative to traditional LIB recycling technologies. These claims are being suggested by several key players, as investigated in the new report. Several of these players are also in pilot stages of direct LIB recycling technology development, with a few close to commencing commercial operation of their first direct LIB recycling plant.

While direct LIB recycling proposes a cheaper solution, two key challenges include demonstrating performance over extended cycling (>1000 cycles) with minimal capacity fade, and upcycling chemistries to meet new market demand. If an EOL LIB is used as the direct recycling feedstock, this will likely need to be upcycled to a newer chemistry since the feedstock will lag demand for new, potentially higher performance, chemistries. Upcycling is therefore likely to add to process cost, due to extra processing and potentially added process energy intensity, reducing the commercial viability of the technology.

{kind=link}

However, LIB cell manufacturing scrap coming from different points in the cell manufacturing process will also be a key feedstock for direct LIB recycling. Electrode scrap, along with assembled and formed cells can all form parts of cell manufacturing scrap feedstock. Since this feedstock is made available during ongoing cell manufacturing, this chemistry will not require upcycling. This may therefore see this feedstock become favoured for direct recycling technologies in the medium term, which could be also beneficial for the uptick in LFP adoption being observed in current EV and BESS markets. Nevertheless, with the great majority of LFP cell production occurring in China, this niche benefit is only likely to be realized by Chinese LIB recyclers in the medium-term.

Irrespective of feedstock, if upcycling process costs can be minimized, and extended cycling performance of recycled cathodes can be demonstrated, direct recycling technologies could cause a much greater shift in both LIB recycling and virgin cathode production markets in the longer term.

Emerging activity of battery-grade graphite recycling technology development for Li-ion

Commercial recovery and recycling of graphite from Li-ion batteries (LIBs) is limited due to the comparatively lower value of graphite compared to higher value cathode materials, and due to the difficulty of recycling graphite back to a product with battery-grade purity (>99.95%). However, the increasing popularity of LFP, attempts for more localised supply chains, ongoing reliance on China for battery graphite supplies, and continued growth in graphite anode demand, alongside growing pressure for a more circular Li-ion battery industry, has all started to put focus on the recycling of graphite from LIBs.

Several key players are looking to commercialize battery-grade graphite recycling technologies. This includes Li-ion recycling players such as American Battery Technology Company (ABTC), Ascend Elements, and Cylib. Key players focused on graphite recycling include Green Graphite Technologies, EcoGraf, Graphite One, and X-BATT. Some of these players are claiming that their recycled graphite is, or close to, battery-grade, and some are in stages of verifying anodes using recycled graphite in tests with customers (e.g., EV battery manufacturers). While these initial tests look promising, recycled graphite purity and anode performance over extended cycling (>1000 cycles) must be demonstrated to promote the commercial viability of these recycling technologies.

Crucially, given the lower value of graphite compared to other critical battery materials, the methods used to purify and recover recycled graphite will also need to be performed at low cost to ensure the economic viability of battery-grade graphite recycling technologies.

Li-ion battery recycling technology outlook

Traditional LIB recycling technologies, including mechanical, hydrometallurgical, and pyrometallurgical processes, are commercially available, well understood, and capacities for these technologies are expanding globally. However, developing direct recycling and battery-grade graphite recycling technologies could help LIB recyclers realize improved profitability. These technologies could also allow for the more economic recycling of LFP Li-ion batteries. If both the performance of anodes using recycled graphite and the performance of directly recycled cathodes can be shown to not be significantly worse than their virgin counterparts, and process costs can be kept low, these prospects could become a more widespread reality in the long-term. Both technologies continue to undergo development, with some direct LIB recyclers looking to soon commission their first commercial-scale plant.

For more information on this report visit www.IDTechEx.com/LIRecycling.