Energy Transfer LP (NYSE: ET) today reported financial and operational results for the fourth quarter and fiscal year ended December 31, 2025. The Partnership achieved record-breaking volumes across nearly all major business segments and reached a new annual milestone for adjusted EBITDA, though quarterly net income saw a year-over-year decline.

Financial Performance and Distribution Growth

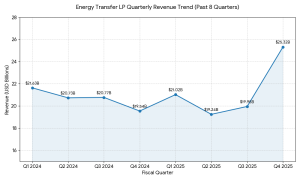

For the fourth quarter of 2025, Energy Transfer reported net income attributable to partners of $928 million, or $0.25 per common unit. This represents a decrease from $1.08 billion ($0.29 per unit) in the fourth quarter of 2024, primarily due to higher operating expenses and interest costs. Quarterly revenues reached $25.32 billion, a 29.6% increase over the same period last year.

Despite the quarterly earnings miss relative to analyst expectations, the Partnership’s cash-flow metrics remained robust:

Adjusted EBITDA: Q4 Adjusted EBITDA rose 8% to $4.18 billion. Full-year 2025 adjusted EBITDA reached a record $16 billion.

Distributable Cash Flow (DCF): DCF attributable to partners for the quarter was $2.04 billion, up from $1.98 billion in Q4 2024.

Cash Distributions: Underscoring its commitment to unitholder returns, Energy Transfer recently increased its quarterly distribution to $0.3350 per common unit ($1.34 annualized), a 3% increase over the prior year.

Operational Records Across the Network

Energy Transfer’s diversified midstream franchise saw unprecedented volume growth in 2025. For the full year, the Partnership set new operational records in the following categories:

Crude Oil Transportation: Up 6% vs. 2024.

NGL Transportation & Fractionation: Transportation volumes rose 6%, while fractionation volumes set a new record with a 2% increase.

Midstream & Natural Gas: Midstream gathered volumes grew by 5%, and interstate natural gas transportation volumes increased by 7%.

NGL Exports: Total export volumes surged 9% to a new record.

Strategic Capital Allocation and 2026 Outlook

In a strategic shift, management announced the suspension of the Lake Charles LNG export project. The decision allows the Partnership to prioritize a substantial backlog of natural gas pipeline infrastructure projects that offer superior risk/return profiles and immediate market demand.

“We are seeing a significant increase in demand for natural gas infrastructure, particularly to support the rapid expansion of data centers and power generation,” the company noted during its earnings presentation. Energy Transfer recently began flowing gas on its first dedicated lateral to a data center campus near Abilene, Texas.

Updated 2026 Guidance:

Adjusted EBITDA: Raised to a range of $17.45 billion to $17.85 billion (up from $17.3–$17.7 billion).

Growth Capital: Expected to be between $5.0 billion and $5.5 billion.

Key Projects: Focus areas for 2026 include the Desert Southwest Pipeline (recently upsized to a 48-inch diameter with 2.3 Bcf/d capacity), the Mustang Draw I and II processing plants, and the Frac IX expansion at Mont Belvieu.

Liquidity and Balance Sheet

As of year-end 2025, Energy Transfer maintained a strong financial position with $2.12 billion in available capacity on its revolving credit facility. The Partnership continues to target a long-term leverage ratio of 4.0x to 4.5x EBITDA, ending the year with its strongest financial standing in history.

The post Energy Transfer LP Announces Record Full-Year 2025 Results and Increased 2026 Guidance first appeared on AlphaStreet News.