European Gas Prices Soar 50% After Qatar Shuts World’s Largest LNG Export Plant

In its scenario analysis of how the Iran war could impact energy markets, Goldman laid out a section dedicated to nat gas, and specifically LNG, which like oil, is one of the commodities that is especially reliant on prompt passage through he Straits of Hormuz to reach its destination.

Specifically, unlike oil which Goldman calculated had already priced in substantial war risk premium, “European gas (TTF) and spot LNG (JKM) prices have embedded little-to-no risk premium until this past Friday” and so, the bank saw “significant upside risk to prices from a potential sustained disruption of LNG supply through the Strait of Hormuz. In a scenario where flows halt for one month, we think it is likely that TTF and JKM could approach 74 EUR/MWh ($25/mmBtu) — 130% above current levels — a threshold that triggered large natural gas demand responses during the 2022 European energy crisis.”

Here we go again: Europe among most exposed to Hormuz, with Goldman warning of massive 130% upside risk for European (TTF) gas prices, potentially hitting 74 EUR/MWh, if LNG flows are blocked https://t.co/yD07qFkNk4

— zerohedge (@zerohedge) March 2, 2026

Below we excerpt the key sections from the must read report (especially to European energy traders as we will discuss in a bit).

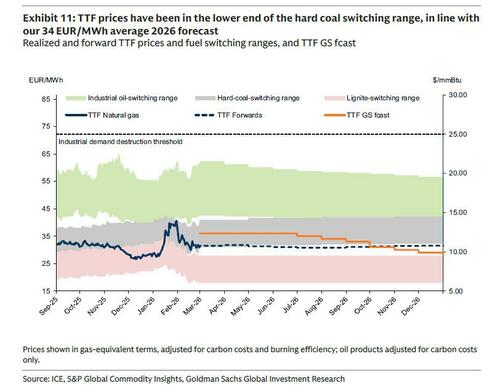

Q10. How much risk premium has been embedded in European gas prices?

Differently from oil, we believe that until this past Friday, European natural gas prices had embedded little-to-no risk premium associated with Iran-related geopolitical risks. Specifically, TTF has been pricing in the bottom half of our estimated hard-coal-to-gas (C2G) switching range for the past month, modestly below our 36 EUR/MWh March 2026 TTF forecast (Exhibit 11). Once accounting for the recent sell off in carbon emission prices to below the 80 EUR/t embedded in our TTF price forecast, worth 2.0-2.5 EUR/MWh in gas-equivalent terms, prompt gas prices are still largely in line with our view that TTF needs to be in this C2G switching range to help manage NW European gas storage to above 80% full by end-Oct26, given that current inventory levels remain well below average. That remains our view, and we maintain our 34 EUR/MWh balance-of-the-year TTF price forecast.

{kind=link}

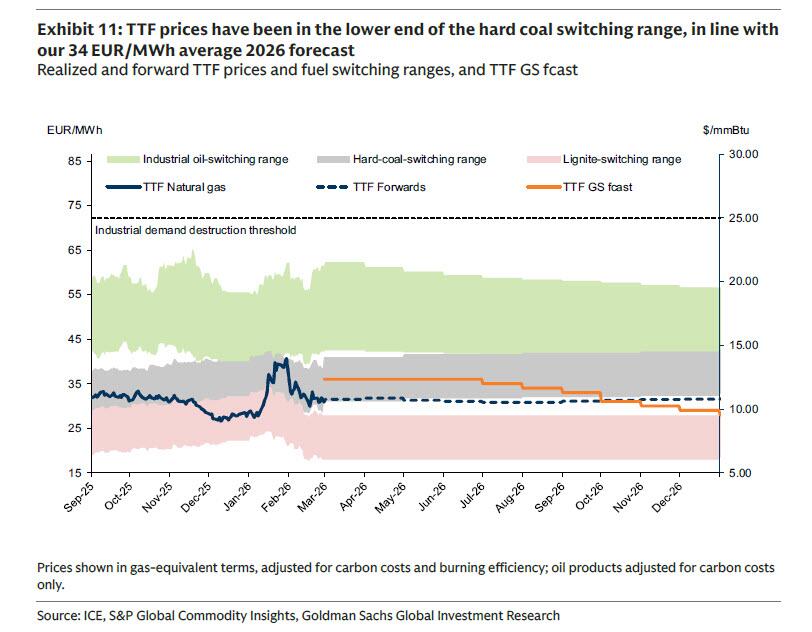

Q11. What are the risks to global gas prices from this weekend’s developments in the Middle East?

We see significant upside risk to European gas and global LNG prices. The most significant impact to global gas markets would come from a potential disruption of the approximately 80 mtpa (302 mcm/d or 11 Bcf/d, 19% of global LNG supply) of LNG that typically flow through the Strait of Hormuz (Exhibit 2), which could potentially arise from an escalation of the ongoing conflict.

{kind=link}

Specifically, in a scenario where LNG flows through the Strait are fully halted for one month, we estimate a resulting tightening of NW European gas storage equivalent to 8% of capacity. Our fuel switching models suggest that European gas prices would need to maximize both switching into hard coal and into oil products by pricing at or above distillate fuel price levels for over three and a half months to offset it. At current oil prices this would imply TTF essentially doubling to 62 EUR/MWh[10] ($21/mmBtu). Given that oil prices would also likely rally in this scenario, it is likely that TTF could approach the 74 EUR/MWh ($25/mmBtu) threshold that triggered large natural gas demand responses during the 2022 European energy crisis.

A hypothetical longer disruption of natural gas supply transit through the Strait of Hormuz lasting more than two months would likely lift European natural gas prices above 100 EUR/MWh ($35/mmBtu) to trigger more significant global gas demand destruction given the increased difficulty for the market to fully offset such a tightening shock ahead of the next winter.

See “Goldman’s Commodity Desk Lays Out The Oil Price Scenarios From Iran War” for more details).

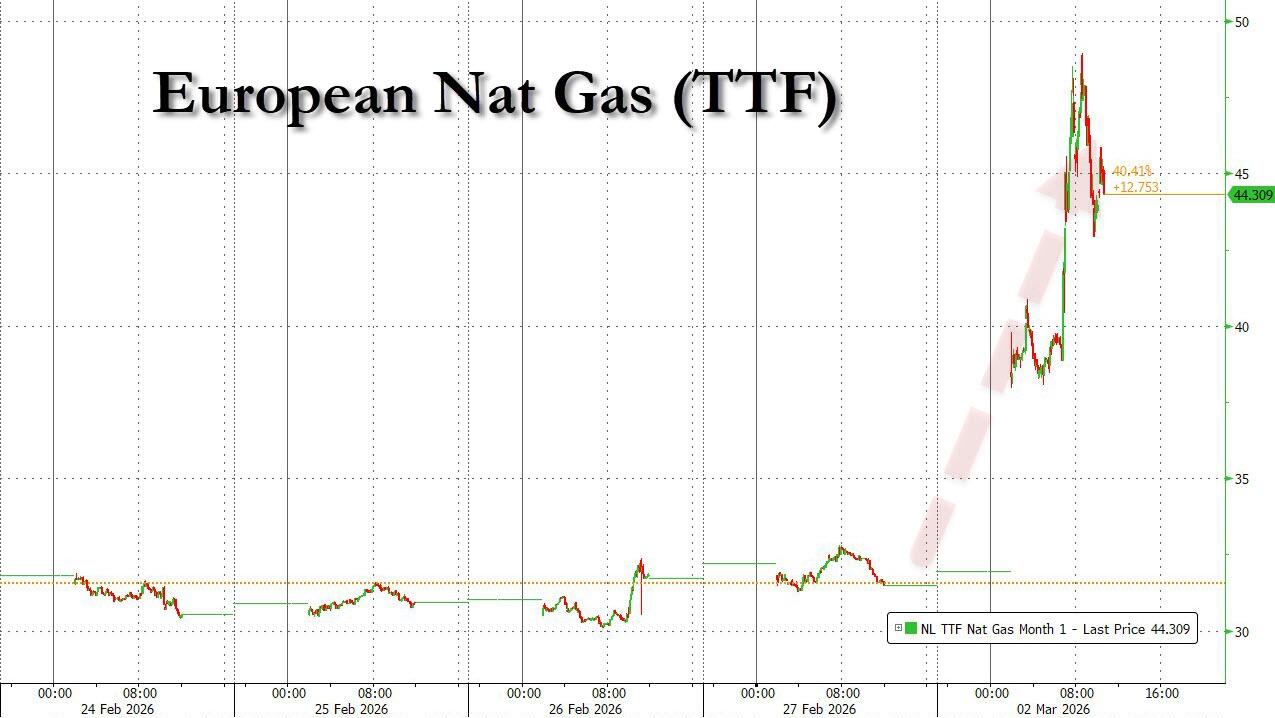

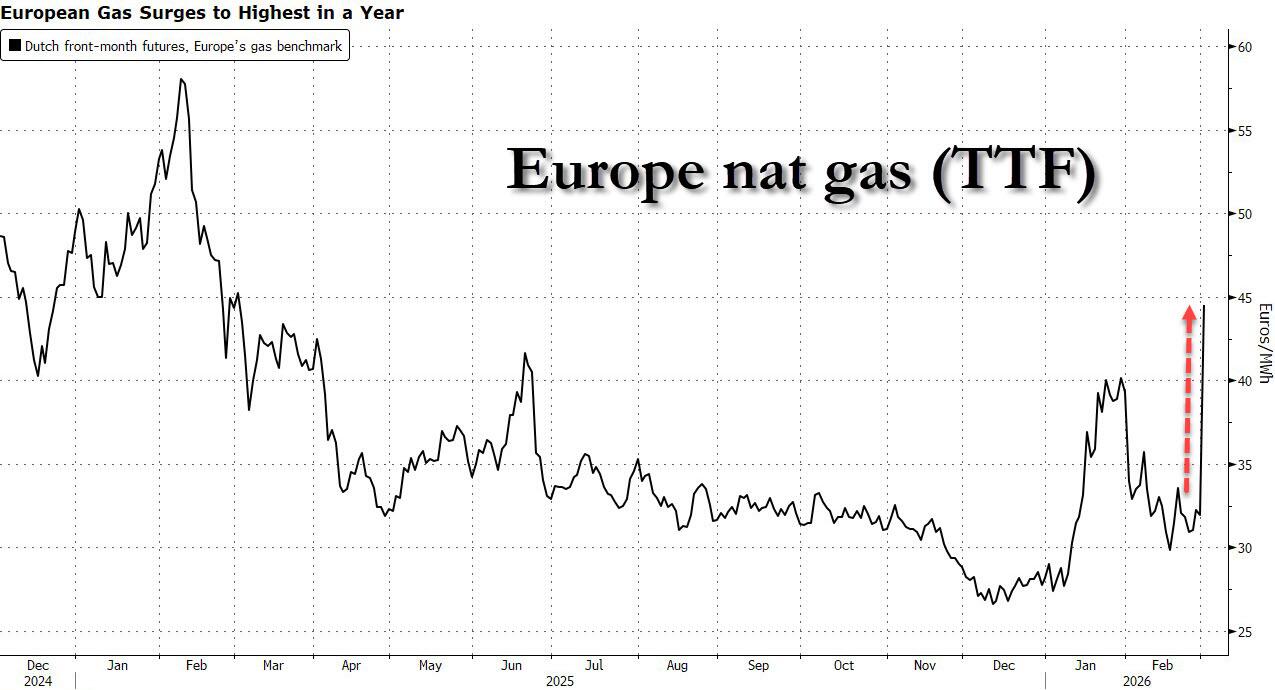

Well, for once Goldman’s commodity research desk was spot on… and very quickly at that, because just one day later, TTF shot up as much as 50%, sparking chaos across Europe’s energy markets in a deja vu moment of the start of the Ukraine war 4 years ago. Dutch front-month futures, Europe’s gas benchmark, traded 46% higher at €46.77 a megawatt-hour by 2:31 p.m. in Amsterdam. That’s the highest level since February 2025.

{kind=link}

Qatar’s Defense Ministry said said earlier that two drones launched from Iran had struck facilities in the country, although there were no casualties.

The catalyst behind today’s sharp move is not the full closure of Hormuz, which Iran still claims is passable despite occasional ships in its vicinity randomly catching fire, but because early on Monday, Qatar Energy shut down liquefied natural gas production at the world’s largest export facility after it was targeted in an Iranian drone attack.

QatarEnergy to stop production of LNG

Due to military attacks on QatarEnergy’s operating facilities in Ras Laffan Industrial City and Mesaieed Industrial City in the State of Qatar, QatarEnergy has ceased production of liquefied natural gas (LNG) and associated products.…

— QatarEnergy (@qatarenergy) March 2, 2026

QatarEnergy’s Ras Laffan plant covers about a fifth of global LNG supply and the unprecedented halt now threatens energy security worldwide.

In kneejerk response, European benchmark gas futures jumped the most since the energy crisis in 2022, while tankers had already largely stopped transiting the Strait of Hormuz, a critical artery for global fuel shipments. Needless to say, one direct hit on an LNG ship and the fireworks would be historic.

“The threat to security of supply is here and now,” said Simone Tagliapietra, an analyst at Bruegel. “The extent of it will depend on the duration of the shutdown, but we are now into a new scenario.”

The good news, if only for the US, is that as Goldman notes, there is “limited upside risk to US natural gas prices.”

Bloomberg notes that while Asian countries buy most of the LNG shipped from the Middle East, a disruption will increase competition for alternative supplies pushing up prices worldwide, including in Europe.

European gas prices are also rallying as storage inventories are unusually low, and the region needs to import large volumes of LNG this summer to refill them ahead of next winter. While the intraday surge is the biggest since Russia’s invasion of Ukraine four years ago, benchmark prices are only at a one-year high because regional supplies haven’t been directly disrupted and traders are still assessing how long the conflict will last.

{kind=link}

As we discussed yesterday, the key question for traders is how long the disruption will last: the longer, the higher prices will rise. Even if the US boosts LNG production, it’s unlikely to be enough to offset supply from Qatar in the near-term. QatarEnergy is scheduled to start its Golden Pass expansion project in the US in the coming weeks but the facility won’t be at full capacity until next year.

Gas trade disruptions in the Middle East could also eventually raise spot LNG demand from Turkey, according to BloombergNEF, as it imports pipeline fuel from Iran.

Late on Sunday, Trump said the bombing campaign against Iran could last for weeks; The conflict continues to deepen, with blasts heard across Israel, Saudi Arabia, Qatar and the United Arab Emirates, as states intercepted Iranian missiles launched in response to US-Israeli strikes.

Tyler Durden

Mon, 03/02/2026 – 11:02