Futures Flat, Global Stock Rally Fizzles Ahead Of PPI Report

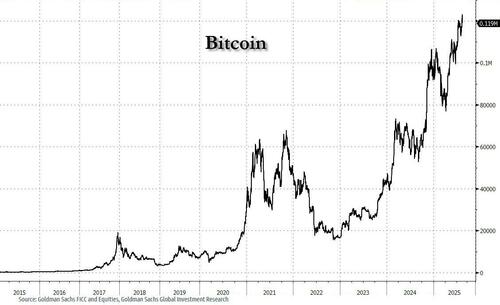

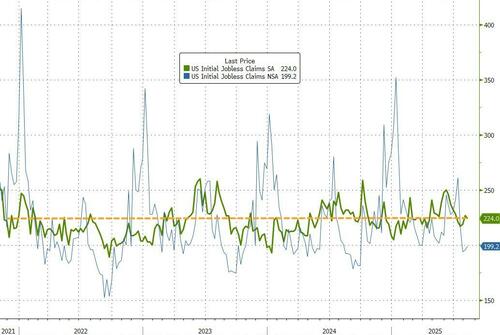

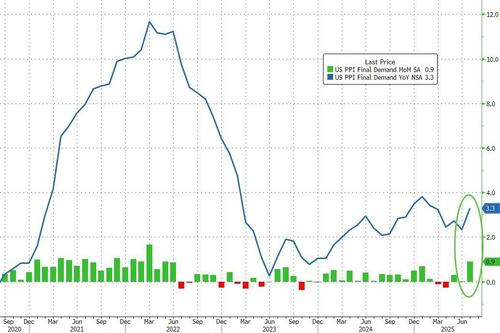

The global market rally stalled and US equity futures are flat with small caps underperforming (SPX and NDX made new ATHs yesterday while the Russell still sits ~5% below its ATH) into this morning’s PPI print, where the market may confirm CPI’s trend as well as solidifying PCE estimates. As of 8:00am, S&P 500 futures were flat changed after the benchmark notched a record close for a second straight session; Nasdaq futures dropped 0.2% after Cisco shares fell after issuing a cautious full-year revenue outlook. Europe’s Stoxx 600 rose 0.3%. Pre-mkt, Mag7 names are mostly higher with Semis weaker; Defensives looking stronger than Cyclicals with healthcare leading. Bond yields are lower as the curve bull flattens: the yield on 10-year notes dropping two basis points to 4.21%. Bitcoin retreated 1.7% from an all-time high and the USD is flat. Today’s macro data focus is on PPI and Initial Jobless Claims; an in-line print in both should support stocks. JPMorgan says that should the rally resume, look for RTY to close the gap to tech/large caps.

{kind=link}

In premarket trading, Magnificent Seven stocks are mixed (Microsoft +0.3%,Tesla +0.4%, Meta -0.01%, Amazon +0.2%, Alphabet -0.06%, Nvidia +0.09%, Apple +0.07%).

Bullish (BLSH) rises 15% a day after the crypto exchange operator and CoinDesk owner raised $1.1 billion in an initial public offering.

Bumble (BMBL) falls 11% after holders offered to sell shares at a 11% discount to the closing price.

Cisco Systems (CSCO) slips 1.4% after the largest maker of machines that run computer networks and the internet gave a lukewarm forecast for the current fiscal year.

Coherent Corp. (COHR) sinks 20% after the fiscal 4Q report from the photonics company, which also said it would sell its Aerospace and Defense business to Advent for $400 million.

Deere (DE) falls 5% after the agricultural-equipment giant trimmed the high end of its full-year net income outlook

DLocal (DLO) surges 26% after the payments company reported net income for the second quarter that beat the average analyst estimate.

NetEase ADRs (NTES) fall 6% after the company reported 2Q sales that missed estimates and growth at its core gaming segment fell short of expectations.

Ibotta Inc. (IBTA) slumps 33% after the digital marketing software company provided a third-quarter forecast that trailed expectations.

PagSeguro (PAGS) falls 6% after the company reported total payment volume in the second quarter below what analysts expected.

Tapestry Inc. (TPR) declines 6% after its annual outlook for a key profit metric missed analysts’ forecasts due in part to tariffs, a sign that Wall Street is still adjusting to the full cost of duties for US companies.

TeraWulf (WULF) soars 17% after signing two 10-year high-performance computing colocation deals with AI cloud platform operator Fluidstack.

Today’s PPI report is expected to show an uptick in producer prices, while Friday’s retail sales figures will offer insight on US consumer health as the labor market shows signs of losing momentum. Traders are now fully pricing in a quarter-point cut at the Fed’s September meeting, with some bets leaning toward a larger move following this week’s benign inflation data.

“We’re constructive about the market and that’s been backed up by data and earnings, but we’re certainly not looking to add more at these levels,” said Rory McPherson, chief investment officer at Magnus Financial Discretionary Management. “Bad news is good news as far as retail sales are concerned. But a 50-basis-point cut would seem too reactionary.”

Today’s data “could be make-or-break to cement a 25 basis-point rate cut from the Fed, or even to encourage the possibility of a jumbo cut,” said Andrea Gabellone, head of global equities at KBC Securities in Brussels. “People are already speaking of a 50 basis-point cut, but I think we will need further labor data to shift the narrative.”

San Francisco Fed President Mary Daly pushed back against calls for a half-point cut next month, telling the Wall Street Journal the move “would send off an urgency signal that I don’t feel about the strength of the labor market.”

In Europe, the Stoxx 600 rises 0.3% as upbeat earnings from insurers helped offset disappointing reports from companies including Adyen and HelloFresh. Earnings also caused other major swings, like a 40% surge for warehouse automation firm Autostore, which surged 40%, and game developer Embracer, which sank 25%. Here are the biggest movers Thursday:

Autostore surges as much as 40%, the most on record, after delivering orders, sales, and Ebitda in the second quarter that were all significantly ahead of analyst expectations

Talanx shares are up as much as 8.3% on Thursday morning, the biggest gain since April, as the insurance company upped its guidance for the full year, beating the average analyst estimate. The stock is up 51% this year

Aviva shares rally as much as 5% to trade at their highest level since 2018 after the insurer delivered profits well ahead of expectations in the first half. Jefferies said it was particularly pleased with the update on Direct Line

Admiral Group shares rise as much as 7.8%, the most since March, after the British insurer reported strong 1H profits and announced a dividend that analysts at JPMorgan said was above expectations

Adyen shares slide as much as 20%, the most since 2023, after the payments firm toned down its sales growth outlook for the year, saying a prior view of full-year net revenue acceleration is “unlikely”

Embracer falls as much as 25%, the most since May 2023, after the Swedish game company cut its full-year outlook while publishing a weak 1Q earnings report. Analysts say the outlook dents confidence in the firm

Carlsberg shares fall as much as 7.4% despite narrowing its full-year profit outlook to the upper end, after the Danish brewer’s organic volume, sales growth and Ebit were lower than expected

Thyssenkrupp shares fall as much as 12%, the most since May, after the German steel and engineering group cut its full-year guidance for sales and earnings, and posted a deeper third-quarter loss

HelloFresh shares fall as much as 17%, the steepest drop since March, after the meal-kit firm lowered its earnings guidance and delivered what analysts described as a soft topline performance in the second quarter

Lanxess shares fall as much as 4.4%, the most in almost a month, after the specialty chemicals company cut its adjusted Ebitda forecast for the full year by more than analysts had expected

RWE shares drop as much as 3.7% to trade at a two-month low after the German electricity company delivered earnings below expectations in the first half. The stock is falling for a sixth consecutive session

Holmen falls as much as 5%, briefly hitting a four-month low, after the forestry and paper firm reported earnings that fell short of expectations, according to analysts, who see the results pushing consensus estimates lower

Beazley shares drop as much as 3.1%, trading at a seven-month low, as the specialist insurer extends its decline after cutting revenue guidance on Wednesday. Analysts at Berenberg meanwhile said the selloff is “overdone”

Earlier in the session, Asian equities declined, with Japanese shares under pressure after US Treasury Secretary Scott Bessent said the Bank of Japan was behind the curve on inflation and likely to raise interest rates, triggering a yen surge. The MSCI Asia Pacific Index fell as much as 0.5%, set to snap a three-day rally. TSMC and Mitsubishi Heavy Industries were among the biggest drags on the benchmark. Shares in Taiwan, China and Hong Kong declined. Indonesian stocks headed for a record. The weakness in Japanese shares follows record highs in the country’s stock benchmarks on Wednesday, fueled by relief over US tariffs and a tech rally. Bessent’s comments coincide with the Bank of Japan’s continued adherence to one of the lowest policy rates among major economies, despite inflation exceeding its 2% target.

In FX, the Japanese yen retains its lead at the top of the G-10 FX leader board, rising 0.6% against the greenback after US Treasury Secretary Scott Bessent said the Bank of Japan is falling behind the curve in addressing inflation. The Norwegian krone climbs 0.2% after the Norges Bank left interest rates on hold and reiterated its plan to extend easing later this year. The pound inched higher as the UK economy fared better than expected in the second quarter, raising the bar for further rate cuts from the Bank of England.

“Hopes of a sharp rebound are likely to be dashed,” said George Brown, senior economist at Schroders. “The labor market has softened and capacity constraints mean even tepid growth is generating inflation pressures. With this in mind, we expect the Bank of England to keep rates on hold for the remainder of the year.”

In rates, treasuries rise and outperform their European counterparts, with US 10-year yields falling 3 bps to 4.21%, outperforming bunds and gilts in the sector by 1bp and 2bp. US yields are 1bp-3bp richer across tenors with the curve flatter, leaving 2s10s spread tighter by around 1.5bp. Treasury futures hold gains, sitting at weekly highs and outperforming European bonds, in anticipation of weekly jobless claims and July PPI data. Fed rate-cut expectations implied by swap contracts ebbed slightly, however, after San Francisco Fed President Mary Daly pushed back on the need for a 50bp cut at the September meeting. Rates markets price in about 24bp of easing for September meeting ahead of US data releases at 8:30am New York time, and a combined 61bp by year-end vs 63bp at Wednesday’s close

In commodities, WTI crude futures climb 0.4% to near $62.90 a barrel. Oil steadied near a two-month low as traders monitor the lead-up to Friday’s summit between the US and Russian leaders. US President Donald Trump cautioned he would impose “very harsh consequences” if Vladimir Putin didn’t agree to a ceasefire in the country’s war with Ukraine. Brent crude traded below $66 a barrel. Spot gold is steady near $3,356/oz. Bitcoin retreats from a record high.

Today’s economic data slate includes July PPI and weekly jobless claims (8:30am). Fed speaker slate includes Musalem (10am) and Barkin (2pm).

Market Snapshot

S&P 500 mini little changed

Nasdaq 100 mini little changed

Russell 2000 mini -0.2%

Stoxx Europe 600 +0.3%

DAX +0.4%

CAC 40 +0.3%

10-year Treasury yield -3 basis points at 4.21%

VIX +0.2 points at 14.64

Bloomberg Dollar Index little changed at 1201.02

euro -0.2% at $1.1685

WTI crude +0.3% at $62.85/barrel

Top Overnight News

President Donald Trump told European leaders during a call on Wednesday that he does not intend to discuss any possible divisions of territory when he meets with Russian President Vladimir Putin in Alaska this week. He confirmed he is willing to contribute some security guarantees for Ukraine – with some conditions. NBC, Politico

Bessent said that Japan’s central bank is falling “behind the curve” on inflation and will probably have to raise interest rates, in a rare swipe by a senior official at the monetary policy of another country. FT

US homeownership affordability dropped to its lowest level on recoUS President Trump signed a pharma Executive Order to fill the Strategic Active Pharmaceutical Ingredients Reserve with critical drug components and signed a space industry related Executive Order, while the White House also announced a revocation of the 2021 Executive Order on competition.rd in June according to the latest Atlanta Fed model, primarily driven by rising home prices. Atlanta Fed

US President Trump signed a pharma Executive Order to fill the Strategic Active Pharmaceutical Ingredients Reserve with critical drug components and signed a space industry related Executive Order, while the White House also announced a revocation of the 2021 Executive Order on competition.

A growing number of blue cities and states across the country, from Washington state to Rhode Island, are looking at ways to wring more revenue from their richest taxpayers. Lawmakers are boosting tax rates on robust annual incomes, hiking capital-gains taxes, and putting new levies on luxury vacation homes. Some state legislators have proposed higher taxes in response to projected shortfalls in federal funding related to President Trump’s new tax law, which extends a broad federal tax cut to the wealthy. WSJ

China is preparing to ask some state-owned enterprises to buy unsold homes from distressed property developers, people familiar said. The firms will be allowed to tap $41.8 billion of funding. BBG

DeepSeek delayed its new AI model after facing issues training it using Huawei chips, the FT reported. The issue underscores the challenges of replacing Nvidia systems. FT

The UK economy grew 0.3% in the last quarter, above all estimates and raising the bar to further rate cuts from the BOE. It means the UK recorded the fastest growth of the G-7 nations during the first half. BBG

San Francisco Fed President Daly pushed back against the need for an interest-rate cut of a half percentage point, or 50 basis points, at the Federal Reserve’s September meeting. WSJ

Manhattan apartment hunters are facing record rents and bidding wars. New leases were signed at a median of $4,700 in July, with rents up 9.3% from a year earlier. BBG

Trade/Tariffs

Brazil’s Vice President said the government will extend the programme that returns part of the exported value to all companies that ship to the US and will extend the deadline for exporters to defer tax payments under the drawback scheme for one year, while the plan will also include government purchases.

US Secretary of State Rubio said the State Department took steps to revoke visas and impose visa restrictions on several Brazilian government officials.

China and India are in talks to resume border trade after a five-year pause, according to Bloomberg.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were ultimately mixed despite the positive handover from Wall St, where the major indices extended on gains amid Fed rate cut hopes as money markets fully priced in a September rate cut. ASX 200 extended on record highs with utilities and financials leading the advances following earnings releases from the likes of Origin Energy and Westpac. Nikkei 225 pulled back from record highs and returned to beneath the 43,000 level with pressure seen amid profit taking, higher yields and a firmer currency. Hang Seng and Shanghai Comp were initially supported with earnings releases in focus including a jump in profits for Tencent Holdings, although gains were capped following weaker-than-expected loans and aggregate financing data from China which showed New Loans contracted for the first time since 2005.

Top Asian News

South Korea is to extend fuel tax cuts by two months through to October 31st and it is to announce a restructuring plan for the country’s struggling petrochemical sector.

DeepSeek delayed the release of its new AI model, R2, after encountering persistent technical issues during the training process which used Huawei chips, via FT citing sources.

Foxconn (2317 TT) expects Q3 revenue to see significant growth Y/Y (prev. significant growth). Q3 Revenue Guide: AI Server growth of over 170% Y/Y. Components and other products: significant growth Y/Y (prev. grow strongly). Cloud & Networking: strong growth Y/Y (prev. strong growth). AI market to continue strong demand in 2026.

China is reportedly mulling asking firms run by central government to purchase homes, according to Bloomberg.

S&P upgrades India to “BBB” from “BBB-“; outlook stable.

European bourses (STOXX 600 +0.3%) opened flat/modestly higher, but sentiment gradually improved as the session progressed to display a positive picture in Europe. Nothing really behind the upside today, but building on two prior days of strength (for the STOXX 600). European sectors opened mixed but now hold a slight positive bias. Insurance takes the top spot and is the clear outperformer in Europe today; Swiss Re (+2.6%) benefits after posting strong H1 results and confirming its FY guidance. Also, booting sentiment is post-earnings upside in Admiral (+5%) and Aviva (+4%), which both reported a beat on op. profit.

Top European News

Norwegian Key Policy Rate 4.25% vs. Exp. 4.25% (Prev. 4.25%); The Committee judges that a restrictive monetary policy is still needed but that it will likely be appropriate to continue with a cautious normalisation of the policy rate ahead

FX

DXY is a little firmer. After two sessions of losses, which have been driven by markets ramping up bets on Fed rate cuts, the DXY is attempting to bounce off its recent lows. There isn’t an obvious reason for the upside and as such, it may be more technical in nature. On Fed speak, Daly spoke with the WSJ where she pushed back on the notion of a 50bps move, saying that she does not see the need to catch up. Price data will reassert itself today on the macro narrative with PPI metrics due on deck, which will help formulate expectations for the PCE release later in the month. DXY has recovered to 97.94 but still shy of Wednesday’s best at 98.13.

EUR is a touch softer vs. the broadly firmer USD with EUR/USD slipping back onto a 1.16 handle after topping out on Wednesday at 1.1730; highest since late July. No real move to EZ GDP Flash Estimate / Employment for Q2. EUR/USD has delved as low as 1.1674 and is currently holding above Wednesday’s trough at 1.1669.

JPY is the clear outlier across the majors with the Yen firmly at the top of the leaderboard. The outperformance is being pinned on Wednesday’s comments by US Treasury Secretary Bessent who remarked that the BoJ is behind the curve on inflation and is likely to hike interest rates soon. This allied with the increased pace of rate cut bets in the US has brought interest rate differentials between the US and Japan into greater focus and dragged USD/JPY to a fresh low for the month at 146.22, briefly slipping below its 200DMA at 146.40. Markets price 15bps of tightening from the BoJ by year-end.

GBP is proving to be more resilient than most peers (ex-JPY) with the pound benefitting from a better-than-expected outturn for UK GDP. M/M growth for June rose to 0.4% from -0.1% (Exp. 0.1%), leaving the Q/Q Q2 print at 0.3% vs. prev. 0.7% (Exp. 0.1%). The upside was driven in large part by government consumption, as opined by ING and therefore may be deemed by some as not showing “high quality” growth. Cable has advanced further on a 1.35 handle with a current session high at 1.3591 and focus on a test of 1.36; not breached since 10th July.

After two sessions of gains vs. the USD, both of the antipodes are softer vs. the broadly firmer dollar. A choppy reaction was seen for AUD after the latest Australian jobs data showed Employment Change slightly missed forecasts but was solely fuelled by an increase in full-time work and the Unemployment Rate fell to 4.2% from 4.3%, as expected.

PBoC set USD/CNY mid-point at 7.1337 vs exp. 7.1743 (Prev. 7.1350)

Fixed Income

JGBs are lower. Market pricing has seen a hawkish shift overnight, with just over 16bps of tightening now implied by end-2025 vs around 14bps on Wednesday. A move that was spurred by a general hawkish shift in the JPY and JGBs overnight. Despite the interview with US Treasury Secretary Bessent occurring on BBG at midday on Wednesday, his comment that the BoJ was likely “behind the curve” and will probably need to hike again has been attributed to the overnight price action.

USTs are firmer, but only modestly so. Digesting the geopolitical updates from the Trump meeting with European leaders and Ukraine yesterday. At the time, the tone was a constructive one from this. Since, that has been corroborated and expanded on by a Politico sources piece. Drivers since a little light with focus more on moves in JGBs and developments elsewhere. As it stands, USTs are at the top-end of a narrow 112-05 to 112-12 band. Given this, yields are lower with the long-end leading slightly, but the flattening is modest in nature as it stands. Ahead, aside from potential geopolitical updates, we keenly await the PPI report to add detail post-CPI into PCE models. Note, Fed’s Daly (2027 Voter) speaking with the WSJ has pushed back on the notion of a 50bps move, saying that she does not see the need to catch up.

Gilts began the day essentially flat, before picking up a handful of ticks to a 92.13 peak. Stronger-than-expected GDP data spurred a kneejerk bearish-bias. With pressure seen in Gilts as the data provides the hawkish contingent at the BoE with more time to scrutinise the development of inflation in the months ahead. On the flip side, the data is very welcome by Chancellor Reeves as stronger growth performance trims the size of the “black hole” that Reeves will need to deal with in October, a development that is welcome by the Gilt market and thus provided a bearish driver into the open.

Bunds are in-fitting with USTs, in a 129.71 to 130.06 band, lifting gradually across the morning. Specifics have been very light for the space this morning, focused on digesting the discussed geopolitical talks and particularly the reason for European optimism (since explained by Politico).

Commodities

Modestly firmer trade across the crude complex despite a stronger dollar and mixed risk sentiment, with oil traders’ sights firmly set on the summit between US President Trump and Russian President Putin tomorrow. The meeting itself has been repeatedly downplayed, with President Trump suggesting there is a good chance of a second meeting and he would like to do a second meeting almost immediately which would include Zelensky if the first meeting goes okay, but there may not be a second meeting if he feels it is inappropriate or if he does not get the answers he wants. WTI currently resides in a 62.70-63.09/bbl range while Brent sits in a USD 65.74-66.08/bbl range.

Mostly softer trade across precious metals against the backdrop of a firmer dollar intraday and with macro newsflow quiet ahead of the US day. Spot gold resides in a USD 3,341.45-3,374.80/oz range, wider than Wednesday’s USD 3,342.62-3,370.82/oz parameter and on either side of the 50 DMA at USD 3,348.91/oz.

Copper futures pulled back from overnight highs and now sits with mild losses amid the firmer dollar and mixed risk environment, with the broader base metals sector reflective of the indecision. 3M LME copper prices reside towards the bottom end of a USD 9,757.10-9,838.70/t range.

Chile’s Codelco said the El Teniente accident caused a loss of 20,000 to 30,000 metric tons of copper, equivalent to USD 300mln, while it later stated that the El Teniente smelter is to restart on Thursday.

Indian oil name BPCL executive says they are tapping alternative oil supplies amid a lower discount on Russian oil sales, discounts have declined to USD 1.50/bbl. Purchased oil from Brazil, West Africa and the US to replace some of the Russian oil.

Bank of America projects an average 890k BPD surplus of crude in the 12-month period from July 2025.

Geopolitics

North Korea said it will not sit down with the US and sees no point in South Korea and the US adjusting joint military drills. It was also reported that North Korean leader Kim’s sister said North Korea has not removed propaganda loudspeakers and has no intention to do so, while the South Korean military said it stands by its previous announcement that North Korea had dismantled propaganda loudspeakers at some points on the border.

Russian Kremlin’s Ushakov says Alaska summit will begin at 11:30 local time on Friday (20:30 BST/15:30 EDT). Russian President Putin and US President Trump to have a one-on-one meeting with translators; also to have a wider meeting with delegations; central topic is Ukraine. Trump and Putin to give a joint press conference at the end of the summit. Sensitive matters to be discussed. To discuss trade and economic cooperation where there is “huge untapped potential”. Delegation to include Lavrov, Ushakov, Belousov, Siluanov and Dmitriev

Russia’s Special Envoy and head of Sovereign Wealth Fund Kirill Dmitriev will participate in the US President Trump-Russian President Putin meeting on Friday, according to Reuters sources.

Russian Finance Minister Siluanov will participate in Trump-Putin summit on Friday, according to RBC citing two sources; Defence Minister Belousov will also attend

“Russian officials: Ukrainian drones cause fires in two Russian regions and ignite oil refinery”, according to Sky News Arabia.

Israeli Finance Minister Smotrich says “[Israeli PM] Netanyahu supports settlement expansion and the imposition of sovereignty over the West Bank”.

Houthis says they bombed Ben Gurion airport in Tel Aviv, Israel, with a hypersonic ballistic missile, according to Al Qahera News.

US Event Calendar

8:30 am: Jul PPI Final Demand MoM, est. 0.2%, prior 0%

8:30 am: Jul PPI Ex Food and Energy MoM, est. 0.2%, prior 0%

8:30 am: Jul PPI Final Demand YoY, est. 2.51%, prior 2.3%

8:30 am: Jul PPI Ex Food and Energy YoY, est. 3%, prior 2.6%

8:30 am: Aug 9 Initial Jobless Claims, est. 225k, prior 226k

8:30 am: Aug 2 Continuing Claims, est. 1967k, prior 1974k

Central Banks

10:00 am: Fed’s Musalem Appears on CNBC

2:00 pm: Fed’s Barkin Speaks in NABelgium Webinar

DB’s Jim Reid concludes the overnight wrap

The market rally continued to power forward over the last 24 hours, with the S&P 500 (+0.32%) reaching another record as investors grew more confident about the near-term outlook. The main catalyst was mounting speculation about a Fed rate cut as soon as the next meeting in September, with the hope being that a series of cuts would help to maintain the economic expansion and support risk assets. Indeed, it’s worth noting that when the Fed have historically cut rates into a soft landing (rather than cutting because of a recession), that’s usually been a very strong backdrop for markets, and so far at least, that pattern has been playing out again.

This strength has been clear across multiple asset classes, with several milestones that demonstrated just how buoyant markets are right now. For instance, the VIX index of volatility (-0.24pts) fell to its lowest closing level of 2025, at just 14.49pts, and Bitcoin prices (+2.31%) hit an all-time high of their own yesterday at $122,951. Meanwhile in credit, Euro IG spreads remained at 79bps, their joint-lowest since 2018. And among sovereign bonds, the spread of 10yr Italian yields over bunds fell to the tightest since 2010, at just 77bps, which was last seen right before the Euro crisis began to kick off in earnest.

One factor driving those moves were comments from Treasury Secretary Bessent, who added to the calls for more aggressive rate cuts. For instance, he said in a Bloomberg interview that “I think we could go into a series of rate cuts here, starting with a 50 basis point rate cut in September”. And more generally, he said that “we should probably be 150, 175 basis points lower.” In the interview, Bessent argued that if the negative revisions to payrolls had been known beforehand, then “I suspect we could have had rate cuts in June and July”. Later in the session, those calls for rate cuts were echoed by President Trump, who said “I believe we should be 3 or 4 points lower”.

After Bessent’s comments, fed funds futures saw an immediate reaction, with 26.7bps of cuts priced for the September meeting by the close. So in other words, markets are now fully pricing in a 25bps cut. Moreover, investors priced in a more aggressive cycle of rate cuts beyond September, with a total of 110bps of cuts now priced in by the June 2026 meeting, up +5.4bps on the day. And in turn, that led to a fresh rally for Treasuries across the curve, with the 2yr yield (-5.6bps) down to 3.68%, whilst the 10yr yield (also -5.6bps) fell to 4.23%.

But even as the administration were calling for faster cuts and markets priced that in, Fed officials were still sounding cautious. In particular, Chicago Fed President Goolsbee (a voter this year) said that the labour market was “strong”, and he referred to the rise in services inflation in this week’s CPI print, saying that “I want some more surety that that’s not going to be a persistent inflation shock.” Meanwhile, Atlanta Fed President Bostic said that “I still have one cut on my outlook” for this year, which is more hawkish than current market pricing, which expects 2 to 3 cuts by the December meeting. Next week the Kansas City Fed are hosting their annual economic policy symposium in Jackson Hole in Wyoming, which has historically often been used for the Fed to signal policy shifts. It was last year that Chair Powell said that the “time has come for policy to adjust”, just weeks before they cut rates for the first time since the pandemic. So all eyes will be on that conference for any fresh signals on the likelihood of rate cuts.

Staying on the Fed, Treasury Secretary Bessent also commented on the search for a new Fed chair, suggesting there were lots of candidates being considered. He said that “I’m going to cast a wide net, 10, 11 people, and then there’ll be a group of us who are meeting with them”. And separately, there was a CNBC article that said they were considering 11 candidates, three of which hadn’t previously been mentioned, including former Fed Governor Larry Lindsey, Rick Rieder at BlackRock, and David Zervos at Jefferies. However, President Trump said later that “I’m down to 3 or 4 names”. As a reminder, Powell’s current four-year term comes to an end in late-May, and in recent instances, the nomination for the next Chair has been announced by the President a few months beforehand.

As markets were pricing in more rate cuts, that proved to be a great backdrop for equities, and the S&P 500 (+0.32%) advanced to a fresh all-time high. That was despite a decline for the Magnificent 7 (-0.31%), which slipped back from its own record on Tuesday. But it was a broad-based advance otherwise, with 421 of the S&P 500’s constituents higher on the day, while the small-cap Russell 2000 (+1.98%) hit a 6-month high and posted its best two-day run (+5.03%) since early April when Trump delayed the Liberation Day tariffs. Meanwhile in Europe, there were solid gains as well, with the STOXX 600 (+0.54%) advancing, whilst the FTSE 100 (+0.19%) was up to a new record. There were also fresh milestones for Italy’s FTSE MIB (+0.60%) and Spain’s IBEX 35 (+1.08%), as both indices closed at their highest levels since 2007.

Otherwise yesterday, there were further headlines on Ukraine ahead of President Trump’s meeting with Russian President Putin tomorrow in Alaska. In particular, a call took place between Trump and several European leaders, and afterwards the European leaders maintained their position that Ukraine needs to be involved in any peace talks. Meanwhile President Trump said that Putin would face “very severe consequences” if he didn’t agree to a ceasefire, and he also suggested that a second meeting could take place afterwards that could potentially also involve Ukraine’s President Zelensky.

Ahead of that meeting tomorrow, oil prices continued their recent decline, with Brent crude (-0.74%) falling to a two-month low of $65.63/bbl. So that helped to alleviate some concerns about inflationary pressures in Europe, and coupled with the move for US Treasuries, European sovereign bonds also posted a very strong rally. For instance, yields on 10yr bunds (-6.5bps), OATs (-7.4bps) and BTPs (-8.0bps) all moved lower, and the 30yr Germany yield (-7.1bps) also came off from its post-2011 high on Tuesday.

Overnight in Asia, there’s been a more mixed tone overnight. In particular, Japan’s Nikkei is down -1.35% from its record high on Tuesday, which comes as the Japanese Yen has strengthened by +0.68% against the US Dollar this morning. That follows comments by US Treasury Secretary Bessent, who said in his Bloomberg interview yesterday that the Bank of Japan were “behind the curve” and that “they’re going to be hiking and they need to get their inflation problem under control”. The US Treasury have commented on BoJ policy before, and in their semiannual currency report, it said that “BOJ policy tightening should continue”, and that tighter policy support “a normalization of the yen’s weakness against the dollar and a much-needed structural rebalancing of bilateral trade”. Japan’s sovereign bond yields have also moved higher this morning, with the 10yr yield up +4.0bps to 1.54%.

Outside of Japan however, markets in Asia have put in a relatively stronger performance. For instance, the Shanghai Comp (+0.20%) is on track for its highest closing level since September 2021, whilst the CSI 300 (+0.54%) is on track for its highest close since October last year. In Australia, the S&P/ASX 200 (+0.55%) has also advanced, and there’ve only been modest losses for the Hang Seng (-0.06%) and the KOSPI (-0.22%).

To the day ahead now, and data releases include the US PPI reading for July, the weekly initial jobless claims, along with the UK Q2 GDP reading. Meanwhile, central bank speakers include the Fed’s Barkin.

Tyler Durden

Thu, 08/14/2025 – 08:29