Futures Rise As Tech Gains On Palantir’s “Cosmic Reward”

Stock futures are higher, led by tech, while metals rebound and global markets more than retrace Friday/Monday losses. Only bitcoin continues to slide on laughable fears that Kevin Warsh will somehow shrink the Fed’s balance sheet. As of 8:00am ET, S&P futures are up 0.3% and Nasdaq futures gain 0.5% after blockbuster results from Palantir renewed the AI trade. Pre-market, Mag7 names are all higher ex-AAPL with PLTR the standout which should aid the Software reboot. Palantir’s forecast for 61% sales growth this year is helping the AI narrative, with CEO Alexander Karp describing the company’s accelerating revenue as “a cosmic reward” for the data analytics firm’s shareholders. Energy, healthcare, and Staples are weaker pre-mkt as all other sectors are big higher. European stocks briefly traded into record territory, while technology stocks led gains in Asia as South Korea’s chipmakers are surging again. Elsewhere, dip-buyers are crowding into metals: gold is +5.5%, silver +9.4% with WTI flat and Ags bid. Bond yields are flat to +1bp with USD flat. Today’s macro focus is on the vote to reopen the government, where Trump told GOP not to block the deal; we also get the January vehicle sales update. NFP / JOLTS have been delayed with release dates to be updated after the gov’t reopens. Earnings remain front and center, with PepsiCo, Pfizer and AMD due today. . Bitcoin remained under pressure.

{kind=link}

In premarket trading, Mag 7 stocks are all higher ex-Apple which is again depressed by soaring memory prices (Alphabet +1.2%, Tesla +1.1%, Amazon +0.7%, Microsoft +0.2%, Nvidia +0.7%, Meta +0.1%, Apple -0.7%)

Gold and silver miners including Newmont (NEM) gain as precious metal prices climb out of a three-day slide. Newmont rises 4%.

AES Corp. (AES) rises 8% after BlackRock Inc.’s Global Infrastructure Partners is said to team up with EQT AB in a bid to acquire the power company.

Eaton Corp. (ETN) falls 5% after the power equipment company forecast adjusted earnings per share for 2026 of $13.00 to $13.50, a range with a midpoint below analysts’ expectations.

Fabrinet (FN) falls 4% after the engineering and manufacturing services company’s results showed component constraints pressuring the datacom business. However, analysts are broadly positive on the prospects going forward.

HP Inc. (HPQ) slips 2% as CEO Enrique Lores stepped down to lead PayPal Holdings.

Palantir Technologies Inc. (PLTR) rises 11% after the company forecast revenue for fiscal 2026 that significantly exceeded Wall Street expectations, a boost for the data analytics company after its shares have gotten off to a lackluster start so far this year.

PayPal Holdings (PYPL) falls 15% after the fintech reported profit and revenue that fell short of expectations. The company also said Chief Executive Officer Alex Chriss will be replaced by HP Inc. CEO Enrique Lores.

Rambus (RMBS) slides 8% after analysts note that a supply chain hiccup weighed on the semiconductor device company’s first-quarter outlook. The stock has performed strongly of late, rising about 24% so far this year.

SoFi Technologies (SOFI) climbs 3% after JPMorgan upgraded to overweight. The bank is positive about the company’s execution and “more tenable valuation.”

Teradyne (TER) soars 20% after the semiconductor manufacturing company forecast revenue for the first quarter that exceeded the average analyst estimate.

In corporate news, Elon Musk confirmed the combination of SpaceX and xAI in a deal that values the enlarged entity at $1.25 trillion, with the company said to still be planning an IPO later this year. Musk’s rationale is that the least expensive way to do AI computations within two to three years will be in space. Bloomberg estimates that xAI is burning through ~$11 billion in cash in 2025, constraining its ability to seek outsized funding rounds similar to OpenAI. In other corporate news, Uber is rolling out its ride-hailing service in the Chinese gambling hub of Macau, expanding into a new Asian market for the first time in years. Watch shares of professional publishers after Anthropic released an AI-powered productivity tool for companies’ in-house legal teams.

Traders’ appetite for risk rebounded after a steep drop in precious metals triggered a pullback from stocks and crypto at the end of last week. Strong US manufacturing data added to optimism, showing that the economy is on a sound footing as the earnings season rolls on.

“There is a lot of liquidity out there and it’s remaining committed to financial assets,” said Guy Miller, chief strategist at Zurich Insurance. “It’s rotating within the markets, and the macro backdrop is supportive of that continuing.”

In politics, Republican opposition to Trump’s deal with Democrats to end the partial government shutdown began to crumble late Monday as two conservative holdouts agreed to end their threatened blockade. And an analysis of results from a state senate district vote in the Fort Worth area showed that a Texas Democrat’s shock win was powered by big shifts among Latino voters.

Looking at earnings season, out of the 178 S&P 500 companies that have reported so far, 79% have managed to beat analyst forecasts, while 16% have missed. PepsiCo reported better-than-expected fourth-quarter profit and announced a $10 billion share buyback. Merck’s forecast for 2026 sales and profit missed Wall Street’s expectations.

Investors will now turn their attention Tuesday to a slate of earnings, including Advanced Micro Devices Inc., after a favorable reception to Palantir’s report. Traders are watching for signs that AMD is challenging Nvidia Corp.’s dominance in the market for artificial-intelligence accelerators as they look more broadly than the Magnificent Seven for winners of the AI trade. AMD has rallied more than 50% since October, while Nvidia remained largely flat.

In Europe, the Stoxx 600 is up 0.2%, having surrendered most of an earlier advance that took the index to an all-time peak. Miners outperform, tracking a rebound in precious metals. Meanwhile, a drop in Publicis Groupe weighed on media shares. Here are the biggest movers Monday:

Amundi shares advanced as much as 6.4% to a fresh high after Europe’s largest asset manager reported what RBC says is a “solid” update and announced a €500m share buyback

The Stoxx 600 Basic Resources Index gained 2.4%, with gold and silver advancing as dip buyers crowded into precious metals following an abrupt unwinding of a record-breaking rally

Plus500 shares rise as much as 8.5%, climbing to a new all-time high, after the trading platform announced its entry into the US retail prediction markets through a deal struck with Kalshi Exchange

ING Groep shares gain as much as 3.1%, hitting a fresh 2007-high, after analysts at Deutsche Bank upgraded the bank and significantly increased their estimates

Swatch shares gain as much as 3.2% after Bank of America upgraded to neutral from underperform on optimism that the worst of the decline is over for watchmakers

R&S jumps as much as 24%, the most on record, after the Swiss transformers manufacturer posted order intakes for the full year that surpassed the consensus estimate

Demant shares plunge as much as 12% to the lowest in three years after the Danish hearing-aid maker provided guidance for 2026 that was below expectations

Publicis shares drop as much as 9%. Despite strong results for the fourth quarter and for the full year, analysts note the advertising agency’s conservative growth guidance for 2026 implies a slowdown

Zalando shares fall as much as 8.5% as Morgan Stanley warned the clothing retailer continued to face risks stemming from social commerce

Siltronic shares slide as much as 6.8% after the silicon wafer manufacturer warned the challenging market is expected to persist in 2026, which analysts at Jefferies believe will weigh on expectations

Schaeffler shares drop as much as 4.5% after UBS downgraded the stock to sell from neutral, warning its current market cap reflects far more ambitious adoption curves and economics for its humanoid robots than he sees likely

Sartorius shares drop as much as 3.6% in Frankfurt, reversing an earlier 4.6% gain. Barclays analysts said it expected “some slight share price weakness today on implied downside risk to consensus estimates”

De Nora drops as much as 10% as Kepler Cheuvreux trimmed its price target on the Italian water technologies specialist, noting 2026 will be a lackluster year,

Asian stocks extended a rally on Tuesday, more than erasing the previous session’s decline, on a rebound in precious metals and resurgent excitement around artificial intelligence. The MSCI Asia Pacific Index rose as much as 3.1%, and was on pace for the best day since April 10. Most regional markets were in the green, with South Korean’s Kospi surging 6.8% as Samsung Electronics and SK Hynix helped lead the broader Asian benchmark higher. Stocks also rose more than 3% in Japan, and closed higher in Taiwan and Australia as well. Hong Kong shares edged down. Indian equities also rallied after President Donald Trump announced tariff cuts on the country’s goods. Risk sentiment broadly recovered on Tuesday, with investors piling back into semiconductors and AI-related shares. Palantir Technologies forecast fiscal 2026 revenue that significantly beat expectations, while Elon Musk’s SpaceX confirmed a $1.25 trillion merger with xAI.

The rout in metals prices is disruptive for equities in the short term and has “created some spillover effects from a liquidity perspective,” Kinger Lau, chief China equity strategist at Goldman Sachs, said in a Bloomberg Television interview. Equities are expected to continue rising this year, driven by AI implementation and investment that will support earnings growth, he added

In FX, the dollar pared an earlier fall with the yen now the weakest of the G-10 currencies, down 0.2%. The Aussie is still leading after the RBA hiked interest rates.

In rates,treasuries posted a small retreat, with the 10-year yield up one basis point at 4.29%. European government bonds also dip.

In commodities, oil prices are steady with WTI crude futures near $62 a barrel. Spot silver is up 8% to about $86/oz while gold is near $4,900/oz.

Looking at today’s calendar, Wards total vehicle sales are expected during the day. JOLTS jobs data for December was on the schedule but has been delayed by the partial government shutdown. Fed speaker slate includes Barkin (8am) and Bowman (9:40am)

Market Snapshot

S&P 500 mini +0.1%

Nasdaq 100 mini +0.4%

Russell 2000 mini +0.1%

Stoxx Europe 600 +0.3%

DAX +0.4%, CAC 40 +0.1%

10-year Treasury yield +1 basis point at 4.29%

VIX -0.1 points at 16.24

Bloomberg Dollar Index little changed at 1190.87

euro little changed at $1.1789

WTI crude +0.1% at $62.22/barrel

Top Overnight News

Republican opposition to Trump’s deal with Democrats to end the partial US government shutdown began to crumble late Monday. The president told House holdouts via social media to pass the measure “IMMEDIATELY!” A chamber vote is expected today. BBG

Elon Musk is merging SpaceX and xAI in a deal valuing the new entity at $1.25 trillion, with SpaceX still planning an IPO later this year, according to people familiar. BBG

Reports out Monday afternoon said OpenAI is unsatisfied with some of Nvidia’s latest artificial intelligence chips, and it has sought alternatives since last year, eight sources familiar with the matter said, potentially complicating the relationship between the two highest-profile players in the AI boom. RTRS

US President Trump said announcing the creation of US strategic critical minerals reserve. We are launching Project Vault today. USD 2bln from the private sector. USD 10bln funding from US Exim Bank.

Australia’s central bank has lifted interest rates for the first time since 2023,one of the first big economies to tighten its monetary policy, in an effort to combat inflation. The Bank increased rates by 25bps to 3.85%. FT

China has let the interest rate on a one-year policy loan to banks drop to a record low, according to people familiar with the situation, lowering funding costs so as to revive economic growth. BBG

Demand softened at Japan’s 10-year bond auction as investors grew cautious ahead of a snap election, keeping yields elevated amid equity gains and ongoing fiscal concerns. BBG

Ukraine has agreed with western partners that persistent Russian violations of any future ceasefire agreement would be met by a coordinated military response from Europe and the US. FT

French inflation fell more sharply than expected last month to a 5 year low, raising further possibility that eurozone inflation could be below the European Central Bank’s target for longer this year. Consumer prices were 0.4% higher than in January 2025, down from a 0.7% increase in December. WSJ

Euro-zone banks unexpectedly tightened corporate credit standards at the end of 2025, the ECB said in its quarterly Bank Lending Survey. BBG

President Trump said he is seeking USD 1bln of damages from Harvard.

House Rules panel advances the Senate funding package.

Trade/Tariffs

Kremlin’s Spokesperson said Russia have not heard any statement from India about halting Russian oil purchases, adding that they intend to continue developing their relations with India.

Earnings

NXP Semiconductors NV (NXPI) Q4 2025 (USD): Adj. EPS 3.35 (exp. 3.31), Revenue 3.34bln (exp. 3.31bln). Q1 Guidance:. EPS 2.77-3.17 (exp. 2.99). Revenue 3.05-3.15bln (exp. 3.09bln).

OpenAI has determined it needs alternatives to NVIDIA’s (NVDA) latest AI chips in some cases, has sought alternatives since last year. OpenAI is unsatisfied with the speed at which NVIDIA’s hardware can spit out answers to ChatGPT users for complex problems.

Palantir Technologies Inc. (PLTR) Q4 2025 (USD): Adj. EPS 0.25 EPS (exp. 0.23), Revenue 1.41bln (exp. 1.34bln). Said sales to US businesses in 2026 are expected to grow at least 115% to more than USD 3.14bln.Outlook:. FY revenue 7.182-7.198bln (exp. 6.3bln). FY adj. operating income 4.126-4.142bln (exp. 3.14bln). Q1 adj. operating income 870-874mln (exp. 641mln). Q1 revenue 1.532-1.536bln (exp. 1.33bln).

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly higher with several bourses firmly recovering from the prior day’s sell-off, as the region took impetus from the positive handover from Wall Street, where markets rallied after a strong ISM Manufacturing report. ASX 200 climbed higher with tech and miners leading the advances, although further upside was capped as the focus turned to the RBA which hiked rates for the first time in over two years and sounded hawkish on inflation. Nikkei 225 surged following recent currency weakness and gained a firm footing above 54,000 to hit a record intraday high. KOSPI outperformed in a turnaround from the prior day’s bloodbath with the Korea Exchange activating a sidecar earlier in the session to briefly halt program trading after a sharp rise in the local benchmark. Hang Seng and Shanghai Comp initially lagged with early pressure seen across tech stocks, despite no immediate obvious catalysts, and with some attributing it to VAT hike concerns, while the Hang Seng TECH Index briefly re-entered bear market territory after dropping more than 20% from its October high. However, Chinese markets then pared their losses alongside the broad rally in Asia.

Top Asian News

China’s No1/central document includes plans to improve and consolidate soybean production. Intend to stabilise food and oil output. To diversify agricultural product imports.

Earthquake of magnitude 5.0 hits near the east coast of Honshu, Japan.

Japanese Finance Minister Katayama continues to refrain from commenting on intervention data and said PM Takaichi talked about FX benefits as a general fact, and didn’t specifically emphasise merits in a weak yen.

Nintendo (7974 JT) President said memory price rises not having a major impact on earnings.

Nintendo (7974 JT) – Q3 (JPY): Operating income 155.21bln (exp. 180.7bln), 9M switch sales -66% Y/Y; sees FY net sales 2.25tln (exp. 2.37tln).

European bourses (+0.4%) opened entirely in the green, but sentiment has since waned a touch off best levels, with a couple of indices now slightly in the red. European sectors opened with a positive bias but are now mixed. Basic Resources outperform, led higher by strength in underlying metals prices. Media lags, pressured by losses in Publicis (-7.4%) and ProSiebenSat.1 Media (-2.2%) post-earnings.

Top European News

French Finance Minister said the G7 needs to agree on a joint instrument to address global macroeconomic imbalances. Joint instruments can have a sectoral focus, such as rare earths.

French Finance Minister Lescure said that the 2026 budget will reduce the deficit to 5.0% from 5.4%, GDP growth of 1% so far in 2026 is a good start.

FX

DXY resumed trade overnight on a softer footing following yesterday’s post-ISM recovery (which printed its first expansion in 12 months and at the fastest pace since 2022). The index gradually pared those losses as the morning progressed, to now trade flat, and at the upper end of a 97.34-97.62 range. On the data front, it was also announced that the BLS has delayed the December JOLTS report due today and the January NFP report that was scheduled for Friday owing to the partial government shutdown. With a House vote expected as early as today, the data could be published next week if the vote passes, ING posits.

Antipodeans are firmer with outperformance in the AUD amid the rebound in risk appetite and metal prices, while further upside was seen after the RBA meeting, where the central bank hiked the Cash Rate by 25bps to 3.85%, as expected, and stated inflation is likely to remain above target for some time. Governor Bullock declined to provide any forward guidance on the future path of interest rates. AUD/USD has come off best levels amid the aforementioned recovery in the DXY but still holds onto most of its gains in a 0.6945-0.7050 current daily range.

Other G10s are flat/lower against the USD, with EUR & GBP flat whilst the JPY lags a touch. For the latter, there was some commentary via Japanese Finance Minister Katayama who reiterated that PM’s Takaichi latest commentary on a weak JPY was a general fact and didn’t specifically emphasise merits in a weak JPY. Focus now on the Japanese snap election, where discussions regarding an LDP “supermajority” is getting more attention. Elsewhere, EUR digested a cooler-than-expected prelim French HICP report which had little impact on the single currency.

Central Banks

RBA hikes the Cash Rate by 25bps to 3.85%, as expected, with the decision unanimous, while it stated that inflation is likely to remain above target for some time. A wide range of data confirms inflation has picked up materially. Broad measures of wage growth continue to be strong. Uncertainty in the global economy remains significant but has so far not affected Australia. Job market conditions are a little tight. Capacity pressures are greater than previously assessed. Private-sector demand is growing faster than expected. There are uncertainties about the outlook for domestic economic activity and inflation and the extent to which monetary policy is restrictive. Quarterly Statement on Monetary Policy:. Underlying inflation is higher than expected. Underlying inflation rose to 3.4% over the year to the December quarter, which was higher than expected three months ago and substantially higher than expected in the August Statement. GDP growth has continued to pick up, with private demand growth surprisingly strong. GDP grew by 2.1% over the year to the September quarter, which was around our estimate of the economy’s potential growth rate. Labour market conditions have been stable. The unemployment rate has been broadly stable at around 4.25% in recent quarters.

RBA Governor Bullock said does not know if this will be a tightening cycle and cannot rule anything out or in.

RBA Governor Bullock said pulse of inflation is too strong and that high inflation hurts all Australians. said:. Board thinks inflation will take longer to return to the target. We cannot allow inflation to get away from us. Will not give forward guidance and the board will remain focused on data. Did not discuss a 50bps rate increase.

US President Trump said Fed chair nominee will do good and that investigation into Fed Chair Powell should be taken to the end.

ECB Bank Lending Survey (Q4) : Overall credit terms and conditions tightened for loans to firms and consumer credit, while they eased for housing loans.

BOK Minutes suggests one board member said further rate cuts should only be considered after risks related to FX and housing markets ease.

ECB Bank Lending Survey (Jan): Banks tightened credit standards for firms, citing higher perceived risks amid lower risk tolerance; Credit standards eased slightly for housing loans, but tightened further for consumer credit.

Fixed Income

JGBs spent the overnight session under modest pressure, with losses of just under 15 ticks at most in a narrow 131.41-60 band. Specifics for Japan are a little light as markets count down to Sunday’s election, and the narrative is increasingly pointing to a convincing LDP victory, with a ‘super majority’ featuring more in discussions around the potential outcome.

USTs are under modest pressure after contained APAC trade. Pressure that is most pronounced at the short end, with yields bid across the curve and flattening as things stand, in a marginal extension on the post-ISM flattener. Today’s docket has been trimmed by the US shutdown, as the BLS will not be updating until there is a resolution and as such, JOLTS will not print. While a funding deal should pass very shortly, Friday’s NFP will also be pushed until at least next week. Currently, USTs trade at the low-end of 111-15 to 111-20+ parameters, at a WTD low, taking out last week’s trough by half a tick but clear of the 111-09 YTD base.

Bunds came under pressure early doors, directionally in-fitting with the above, but with magnitudes a little more pronounced in limited newsflow and light volumes. A move that was perhaps a function of the constructive European risk tone at the time. Bunds as low as 127.74 at the time and currently hold a handful of ticks above that trough with losses of c. 15 ticks on the session. Data-wise, French prelim. HICP came in cooler-than-expected across the board, lifting EGBs generally at the time. A series that works to offset some of the hawkish impulses from the prelim. Thereafter, a 2035 Green Bund auction had little impact on the benchmark.

Gilts gapped lower by 12 ticks, acknowledging the above. UK specifics are very light aside from a well received 2035 auction, which garnered a b/c above the 3x mark. Focus now turns to the BoE on Thursday, where rates are expected to be kept unchanged.

UK sold GBP 4.25bln 4.75% 2035 Gilt: b/c 3.63x (prev. 3.26x), average yield 4.585% (prev. 4.456%), tail 0.2bps (prev. 0.3bps).

Germany sells EUR 1.35bln vs exp. EUR 1.5bln 2.50% 2035 Green Bund: b/c 2.01x (prev. 2.2x), average yield 2.79% (prev. 2.52%), retention 10.0% (prev. 4.2%)

Ireland’s NTMA raises EUR 5bln from the sale of its new 10 year benchmark bond.

South Korea is to sell 3-year and 5-year USD-denominated bonds.

Italy’s Tesoro opens book to sell new 15-year BTP bond via syndication, with guidance seen +10bps to 2040 BTP.

Commodities

Crude benchmarks continued to extend on Monday’s losses, with WTI and Brent nearing USD 61/bbl and USD 65/bbl, respectively. Oil prices traded muted throughout the APAC session but were pressured following comments by Russia’s Deputy PM Novak, saying they have a surplus in fuel supplies. Since, benchmarks have edged a little higher to now trade flat on the session.

Nat Gas futures continue to fall, with Dutch TTF returning to EUR 32/MWh as concerns over the Arctic storm affecting gas production ease.

Precious metals have brushed off the recent tarnish following the aggressive selloff in recent sessions. Spot gold has regained the USD 4900/oz handle as being as low as USD 4400/oz in Monday’s session. Investors have been highlighting that the selloff is just a correction and that underlying drivers for gold, mainly central bank buying and ETF inflows, remain strong.

3M LME Copper continues to rebound, alongside precious metals, as the red metal extends to a session high of USD 13.48k/t. The bounce from the recent selloff comes amid a broader reversal of the risk tone and reports that China could expand its strategic copper reserves. China maintains stockpiles of major base metals such as copper and cobalt to stabilise commodity prices and ease raw material cost pressures. The expansion of the reserves comes amid the recent volatility of metals prices.

Russian Deputy PM Novak said oil demand and supply are in balance.

Kuwait Petroleum Corp. intends to invite global oil firms to assist Kuwait Oil in the development of offshore fields, Bloomberg reported.

China raises its gas and diesel prices by CNY 205 and 195 respectively, effective February 4th.

Russia’s Deputy PM Novak said they have a surplus in fuel supplies, adding that domestic diesel and gas supplies are sufficient.

Shanghai Gold Exchange to adjust margin rations to 17% (prev. 16%) for some gold and silver contracts, and widen the daily price limit to 16% (prev. 15%) as of the 4th February settlement.

China could expand its strategic copper reserves and explore a commercial reserve system with state-owned firms.

Geopolitics: Ukraine

Russian Deputy PM Novak said oil demand and supply are in balance.

Kremlin’s Spokesperson said Russia have not heard any statement from India about halting Russian oil purchases, adding that they intend to continue developing their relations with India.

Russia’s Deputy Foreign Minister Ryabkov said the modernisation of their nuclear triad is at a very advanced stage.

Russia’s Deputy PM Novak said they have a surplus in fuel supplies, adding that domestic diesel and gas supplies are sufficient.

Russia and China held new round of stability talks to support multilateralism.

Ukraine agrees multi-tier plan for enforcing any ceasefire with Russia, according to FT.

reported note that witnesses say loud explosions heard in Ukraine’s capital of Kyiv.

US President Trump said doing very well with Ukraine and Russia and think we’ll have some good news. said:. Putin agreed to no missiles going into Kyiv. We are talking with Iran and we’ll see how that goes.

Geopolitics: Middle East

Iran’s Vice President said a new chapter of Iran’s nuclear achievements will be unveiled.

Iranian official said that a US aircraft carrier has retreated and is now near Yemen.

Geopolitics: Other

Russia and China held new round of stability talks to support multilateralism.

Venezuela’s Interim President Rodriguez met with US Envoy Loro Dogu.

US Event Calendar

8:00 am: Fed’s Barkin Speaks on US Economy

9:40 am: Fed’s Bowman in Moderated Conversation

DB’s Jim Reid concludes the overnight wrap

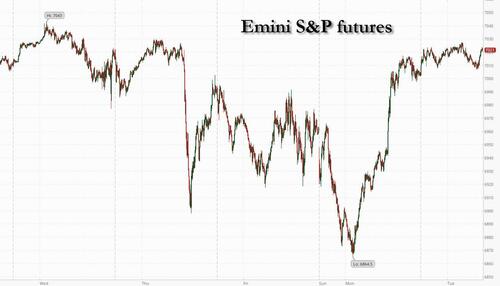

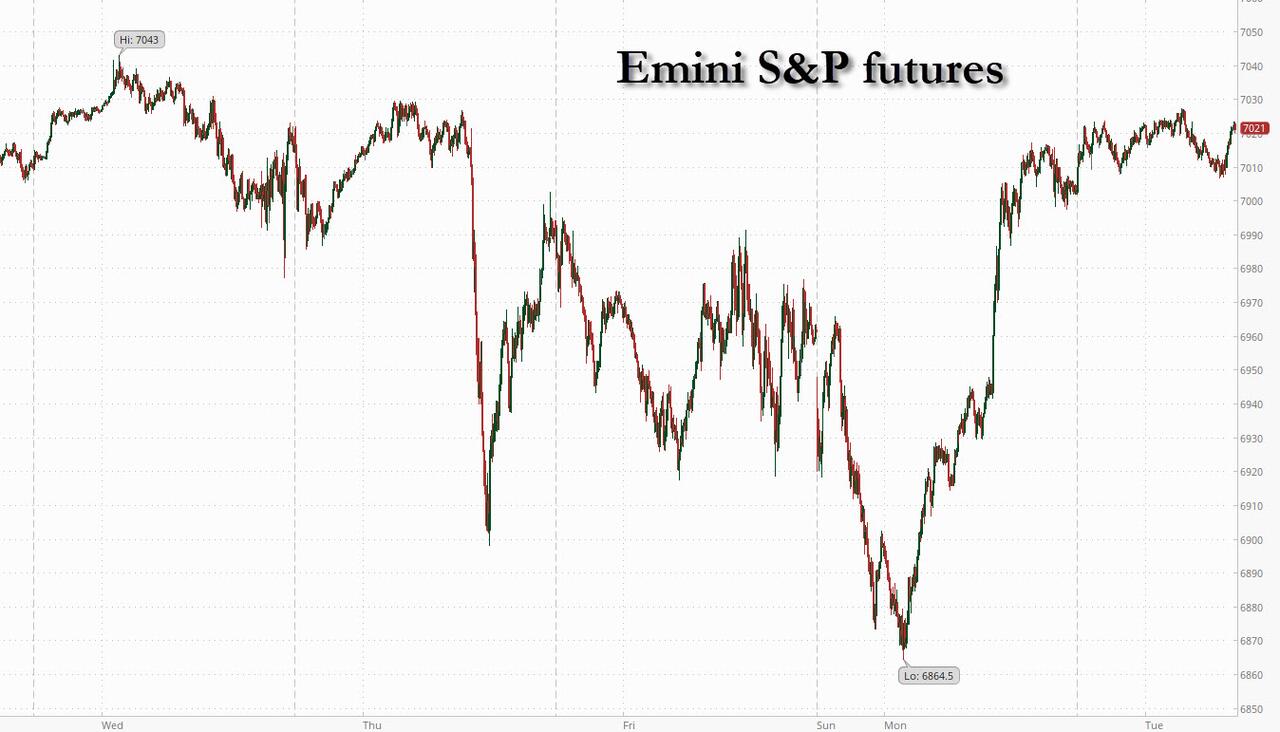

Markets have seen a huge turnaround over the last 24 hours, with the S&P 500 (+0.54%) closing just shy of its record high, with another +0.25% gain in futures this morning after being over -2% lower than current levels this time yesterday. The recovery had several drivers, but the biggest was the ISM manufacturing index, which unexpectedly surged to its highest level since 2022. So that led to growing optimism on the 2026 outlook, along with a classic risk-on move. Meanwhile in Europe, it was a similar story as the STOXX 600 (+1.03%) hit another all-time high, whilst the sharp decline in oil prices helped to ease concern on the inflation side. So it was generally a strong day, with precious metals still the obvious exception, as gold prices (-4.76%) fell to $4,661/oz, whilst silver (-6.96%) saw a fresh plunge that left it down by nearly a third in the last two sessions. However, the yo-yo moves in precious metals have seen gold (+3.46%) and silver (+5.40%) erase most of yesterday’s losses overnight.

That ISM manufacturing print was critical, because it cemented the prevailing narrative of strong data resilience, which has supported markets despite the array of surprising headlines in recent weeks. Indeed, the headline print was back in expansionary territory at 52.6 in January (vs. 48.5 expected), placing it above every economist’s estimate on Bloomberg. And the details were also very strong, with the new orders component surging to 57.1, up +9.7pts on the December print, making it the sharpest monthly jump since June 2020 and the Covid recovery. Clearly it’s only one piece of data, but it’s one of the first we have covering 2026, and it confirmed the robust signals from other sources like the PMIs and the weekly jobless claims.

One of the clearest reactions to the ISM was in US Treasury markets, with yields moving higher as investors priced out the chance of Fed rate cuts. For instance, futures had been pricing in an 87% chance of another rate cut by the June FOMC (which would be Warsh’s first as Chair if confirmed), but that was down to 70% by the close. And in turn, the 2yr yield (+4.9bps) rose to 3.57%, whilst the 10yr yield (+4.2bps) rose to 4.28%. That was particularly noticeable among real yields too, as the 2yr real yield rose by +9.1bps. Higher yields supported the dollar index (+0.66%), which has had its best two-day run since last spring.

Yields were little changed after the latest quarterly borrowing estimates from the US Treasury, which came in at $574bn for Q1 and $109bn for Q2. The Q2 figure was a bit higher than expected, but this was mostly due to an increased end-of-June cash balance target of $900bn, which our strategists expect to be met with higher bill issuance.

While yesterday’s US data delivered positive news, we heard that the BLS will not be releasing the January jobs report on Friday as scheduled due to the partial government shutdown that started last Saturday. In the latest on the shutdown, Trump called on House Republicans to immediately pass the funding deal that was approved by the Senate late last week. Trump’s intervention came as House Speaker Johnson has sought to avoid a push for amendments by conservative Republicans, with a House vote on the package expected today.

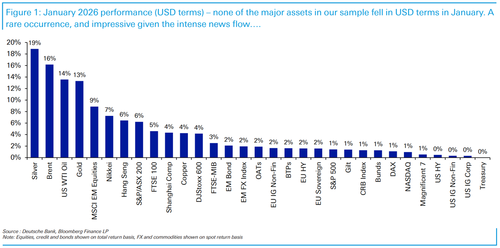

Although precious metals are rallying back this morning it’s worth highlighting Friday and Monday’s losses in aggregate. Gold was down a further -4.76% yesterday, which left them down -13.28% in total over the last 2 sessions, making it the biggest 2-day plunge since 2013, and the second biggest since the 1980s. For silver there was an even bigger slide, with prices down -6.96% to $79.27/oz, which brought the 2-day slide to an historic -31.48%. Indeed, that 2-day move for silver is the biggest fall since Bloomberg’s daily data starts back in 1950, so this is genuinely unparalleled in any of our careers unless you’re reading this in your 90s. If you are, then a special hello this morning.

Meanwhile for oil, yesterday also brought some big declines as investor concern eased about geopolitical risk. In part, that followed Trump’s weekend comments that was hopeful about some sort of deal with Iran. And then yesterday, Axios reported that the US Special Envoy Steve Witkoff would meet Iranian foreign minister Abbas Araghchi in Istanbul on Friday. So that helped to take out some of the geopolitical risk premium, and it marked a sharp turnaround from January when Brent crude saw its biggest monthly jump in 4 years. So by the close, Brent crude fell -4.36% to $66.30/bbl, and WTI was down -4.71% to $62.14/bbl. Moreover, that eased investor concern on the inflation side too, with the US 2yr inflation swap down -4.7bps on the day to 2.55%, its biggest daily drop of 2026 so far.

Against that backdrop, it was a strong day for equities on both sides of the Atlantic. So the S&P 500 (+0.54%) recovered from a run of 3 consecutive declines last week, closing just -0.03% below its record high from last Tuesday. Admittedly, the Mag 7 (-0.10%) continued to struggle, posting a 3rd consecutive decline, but small-caps had a very strong performance, with the Russell 2000 up +1.02%, while consumer staples (+1.58%) and industrials (+1.26%) sectors led the gains for the S&P 500.

Meanwhile, we had news of fresh tariff relief, as Trump posted that the US would cut the main tariff on India from 25% to 18%, while also removing the additional 25% tariff the US imposed on India last August citing its purchases of Russian oil. Trump said India would stop purchases of Russian oil, buy “over $500 BILLION DOLLARS of U.S. Energy, Technology, Agricultural, Coal, and many other products” and remove tariff and non-tariff barriers against the US, though the official details of the pact are not yet clear.

Earlier in Europe, the STOXX 600 (+1.03%) and the FTSE 100 (+1.15%) both hit record highs, whilst Italy’s FTSE MIB (+1.05%) closed at its highest level since 2000. That came as the final PMI readings in Europe were revised in a positive direction, with the Euro Area manufacturing PMI up to 49.5 (vs. flash 49.4), alongside upward revisions in Germany, France and the UK.

Asian equity markets are experiencing a significant rebound this morning, with the KOSPI (+6.13%) seeing a stunning surge in AI-related shares, while the Nikkei (+3.89%) is also witnessing a notable increase, supported by a weaker yen. The S&P/ASX 200 (+0.90%) saw its gains trimmed after the RBA raised the key rate to address rising price pressures (details below). In other areas, Chinese stocks are underperforming compared to their regional counterparts, with the Hang Seng flat and the Shanghai Comp +0.64%. As well as S&P futures (+0.25%) being higher as discussed at the top, Nasdaq futures are half a percent higher as I type.

Returning to the RBA, they raised their benchmark cash target rate by 25 basis points to 3.85%, up from 3.65%, in a unanimous decision by the rate-setting board. The central bank anticipates further potential hikes to address what it perceives as persistently high inflation. This decision follows a resurgence in Australian inflation observed in late 2025, which has also seen core inflation rise above the RBA’s annual target of 2% to 3%. Furthermore, the RBA’s economic outlook, as outlined in its monetary policy statement, now projects headline inflation to reach 4.2% by mid-year, significantly higher than earlier expectations. Additionally, it anticipates that underlying inflation—a trimmed mean measure closely monitored by the RBA—will accelerate to 3.7% by June, up from the current rate of 3.4%. In the short term, the RBA has revised its forecast for economic growth to 2.1% by June this year, an increase from the previous estimate of 1.9%. Following this decision, the Australian dollar (+0.86%) is gaining strength after two consecutive sessions of declines, trading at 0.7008 against the US dollar, while yields on the policy-sensitive 3-year government bonds have risen by +6.9 basis points to 4.31%, marking the highest level since November 2023. Meanwhile, 10-year yields have increased by +3.7 basis points to reach 4.84% as we finalise this report.

Against this background, markets have raised their expectations for a rate increase in May to 79%, with the market anticipating a cumulative tightening of 36 basis points this year.

Looking at the day ahead, data releases include the January flash CPI print from France, along with the US JOLTS report of job openings for December. From central banks, we’ll hear from the Fed’s Barkin and Bowman, and also get the ECB’s Bank Lending Survey. Finally, today’s earnings include AMD and Pfizer.

Tyler Durden

Tue, 02/03/2026 – 08:32