Futures Slide As Renewed Tariff Turmoil Shakes Global Markets

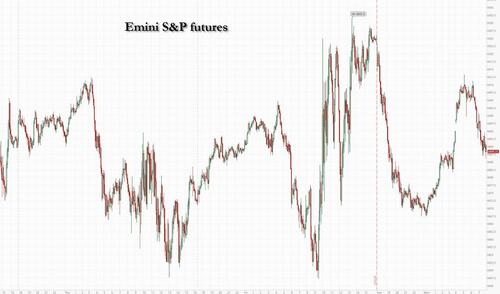

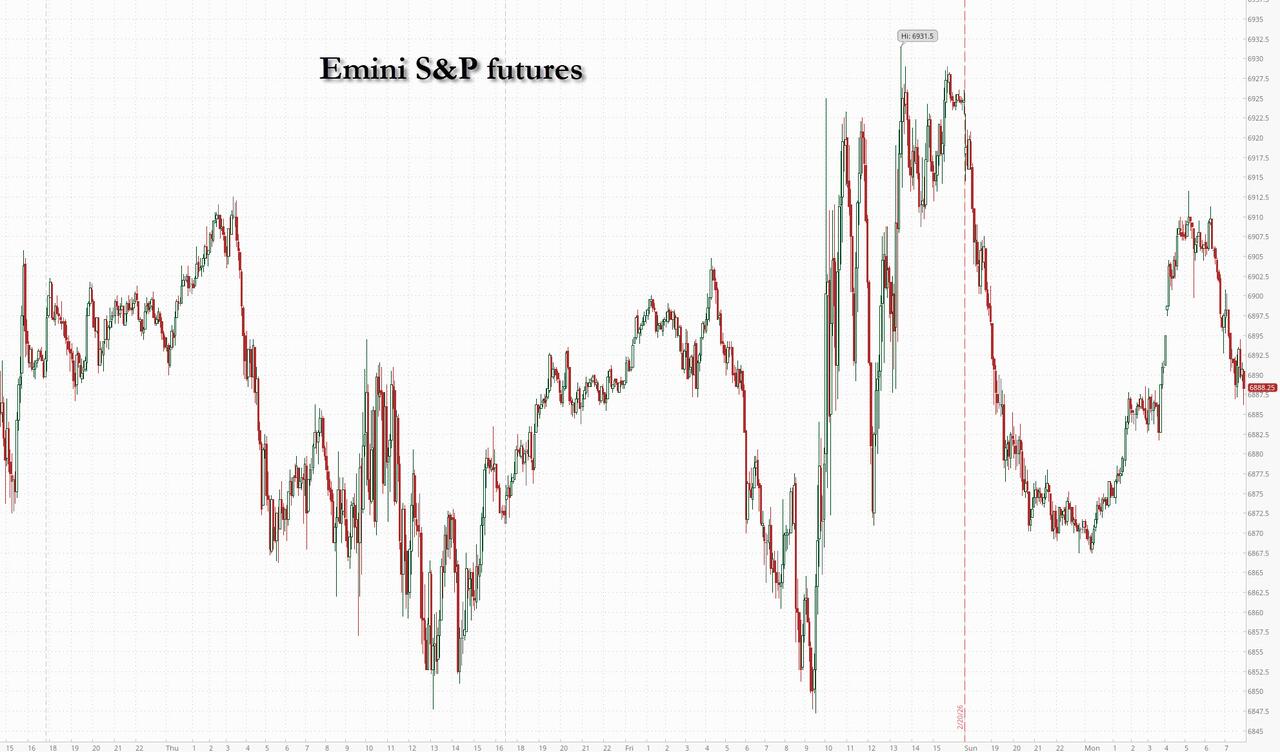

Stock futures slumped after Trump’s weekend tariff tantrum added uncertainty to American trade policy and was another blow to bullish outlooks for 2026. The Supreme Court’s tariff ruling means a big source of fiscal revenue from 2025 may have to be refunded (although if it is refunded to US consumers, who bore the brunt of tariffs as most liberals analysts concluded, it would represent a huge pre-midterm stimulus). As of 8:00am ET, S&P futures were 0.5% lower, giving up almost all Friday gains, while Nasdaq 100 contracts sliding -0.6%. In pre-market trading, there is a defensive tone as Mag7 names are mostly lower, Semis are coming for sale (NVDA flat ahead of earnings on Wednesday); and, most sectors are seeing weakness with pockets of positive performance in HC, Aero/Def, Materials, and Utilities. “We started 2026 with a bullish outlook — but not even two months into the year, many of our assumptions are being challenged,” wrote the Bloomberg Economics team led by Anna Wong. The risk of war in Iran and the AI scare are also denting optimism. The dollar recouped losses while bond yields are flat-to-down 1bp after spiking on Friday on fears the SCOTUS ruling will unleash much more debt issuance. Commodities are seeing weakness in Energy with WTI down 60bp, Ags being sold perhaps on lower tariffs, and precious metals maintain their incessant bid. Today we get factory orders and the final December durable goods report. Key events this week include Trump’s State of the Union Address tomorrow, Nvidia earnings on Wednesday and PPI data on Friday.

{kind=link}

In premarket trading, Magnificent Seven are mostly lower, with the lone exception being GOOGL which rises 0.3% as Wells Fargo upgrades to overweight, calling the search giant an “AI winner.” Others are all down (Nvidia -0.2%, Microsoft -0.5%, Apple -0.5%, Meta Platforms -0.7%, Amazon -0.9%, Tesla -0.9%)

Arcellx Inc. (ACLX) soars 78% after Gilead Sciences Inc. agreed to buy the biotech in a deal with an equity value of up to $7.8 billion.

Domino’s Pizza Inc. (DPZ) climbs 4% after the company reported a larger-than-expected rise in comparable sales, as consumers were drawn to the pizza chain’s budget-friendly pies.

International Paper (IP) falls 6% and Smurfit (SW) drops 6% as analysts note that a surprise price drop in domestic containerboard is negative for packaging companies.

MoonLake Immunotherapeutics (MLTX) rises 4% after the drug developer gave topline results from a mid-stage trial of its experimental therapy for patients with an inflammatory disease that mainly affects the spine.

Vanda Pharmaceuticals (VNDA) climbs 40% after the FDA approved the firm’s oral medication for treating manic or mixed episodes in bipolar I disorder and schizophrenia in adults.

Veris Residential (VRE) rises 12% after agreeing to be acquired by an investor consortium led by Affinius Capital in partnership with Vista Hill Partners, in an all-cash transaction for $19 per share.

VF Corp. (VFC) declines 3% as JPMorgan cuts its rating on the apparel and shoe company to underweight and trims profit estimates for upcoming years.

In corporate news, Honeywell slashed its price to acquire Johnson Matthey’s Catalyst Technologies business in a move to save the deal from falling apart. OpenAI is projecting that its revenue will grow at a fast clip in the next few years and exceed $280 billion in 2030, according to a person familiar. Hynix pledged to boost output of AI memory chips to meet a surge in demand.

The latest questions over tariffs following the SCOTUS rejection of Trump’s signature trade policy are giving traders another focal point in markets that have been grappling with concerns about artificial intelligence and tensions in the Middle East. Investors will also closely follow Trump’s State of the Union address on Tuesday and Nvidia Corp.’s earnings the following day.

“Markets quickly realized that the ruling might not change much in the near term and will rather increase uncertainties,” said Stephan Kemper, chief investment strategist at BNP Paribas Wealth Management. “Donald Trump is not known to avoid a fight or give up easily.”

Trump responded to the ruling by imposing a new 10% global levy, vowing to use other powers to maintain his signature trade policies. He upped that to 15% the next day. US Trade Rep Jamieson Greer said the tariff-policy defeat won’t unravel individual deals the administration has sealed with trading partners. Still, the EU is poised to freeze the ratification process of its deal with the US and is seeking more details from the Trump administration. However, senior US officials, including Trade Representative Jamieson Greer, signaled over the weekend that the court decision wouldn’t unravel agreements already negotiated.

“The question is about the benefit of the rebates versus the extra uncertainty that the trade issues are causing, and for me the latter wins,” JPMorgan Asset Management Global Market Strategist Hugh Gimber told Bloomberg TV. “That for me risks putting business activity on hold, because companies simply don’t know what’s to come further down the line.”

For JPMorgan strategists, an equity-market pullback driven by global tariff policies or an escalation in Iran could create dip-buying opportunities as long as the macro backdrop remains positive. “Adverse geopolitical headlines” could lead to de-risking given the recent rally and stretched technicals, wrote the team led by Mislav Matejka. “But we believe that these will not be long-lasting, and should be seen as buying opportunities.”

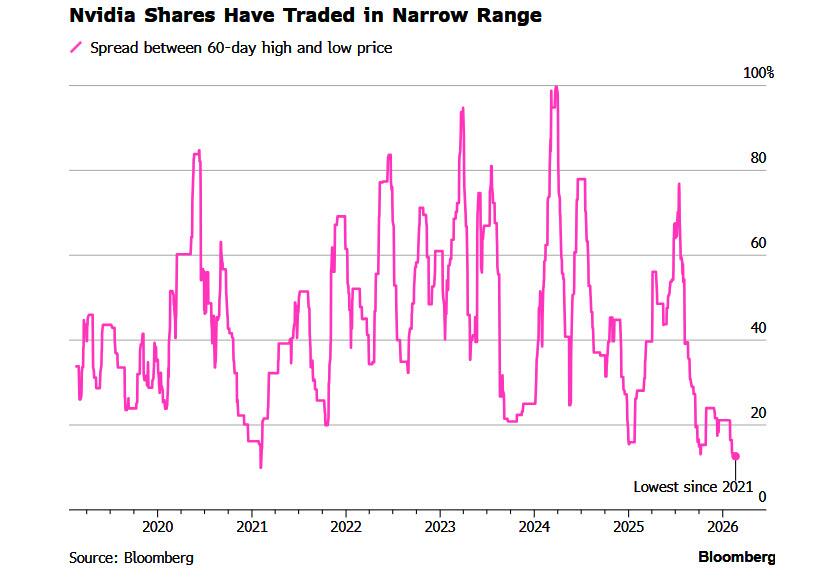

Meanwhile, the hunt for AI losers (and winners) continues in both public and private markets. Today’s Big Take looks at the fallout in private credit after Blue Owl, a prominent software lender, permanently shut the gates on one of its funds. The biggest AI event this week comes in the form of Nvidia results. Still, the chip giant’s stock is stuck in a range and even blowout earnings may not lift it according to Bloomberg.

{kind=link}

“We started 2026 with a bullish outlook — but not even two months into the year, many of our assumptions are being challenged,” wrote the Bloomberg Economics team led by Anna Wong. The Supreme Court’s tariff ruling means a big source of fiscal revenue from 2025 may have to be refunded. The risk of war in Iran and the AI scare are also denting optimism.

European indices are mixed, Stoxx 600 is down 0.4%. Trade uncertainty dominates the macro conversation with the EU set to halt its trade deal with the US. Technology and health care shares led declines, while banks and utilities were the biggest outperformers. Here are the biggest movers Monday:

Novo Nordisk shares fall 11% after the firm said its Cagrisema product fell short of Lilly’s Zepbound in a trial

Enel shares rise as much as 6.1%, the most since March 2022, after the Italian energy company forecast higher-than-expected dividends and EPS growth, and announced a €1 billion share buyback

ABN Amro Bank shares rise as much as 3.7%, the most since November, after BofA Global Research raises its recommendation on the lender to buy from neutral

JD Sports shares climb as much as 6.5% after the sportswear retailer said it plans to return £200 million to shareholders through buybacks in its 2027 fiscal year

Quilter shares rise as much as 3.9% after being placed on JP Morgan’s Positive Catalyst Watch ahead of its results for the full year of 2025 as analysts see upside risk due to the British wealth manager’s expected share buyback

Johnson Matthey shares fall as much as 17%, most since 2021, after Honeywell cut the price it’s paying for the UK company’s Catalyst Technologies business

Belimo shares fall as much as 12% after analysts expressed concerns over the heating and cooling equipment maker’s guidance for 2026 and the delayed impact of tariff decisions

Pernod Ricard shares drop as much as 4% after being downgraded at Deutsche Bank, with analysts pointing to the stock’s year-to-date outperformance and uncertainty about the alcoholic beverage maker’s growth

EQT falls as much as 4.5% on Monday as Citi trims its price target, while maintaining its buy rating on the Stockholm-based investment firm, amid concerns that AI-driven volatility could slow private-markets activity

Earlier in the session, Asia’s equities rose to hover near record highs, driven by gains in tech, while investors weigh the impact of US President Donald Trump’s latest slate of tariffs on the region. The MSCI Asia Pacific ex-Japan Index advanced as much as 1.3%, with Tencent and Alibaba among the biggest boosts to the gauge. Hong Kong’s Hang Seng Index gained 2.8%, while tech-heavy benchmarks in Taiwan and South Korea rose as well. After the US Supreme Court ruled Friday that Trump’s use of the International Emergency Economic Powers Act to impose duties was illegal, China and India now stand to gain from lower tariff rates on exports to the US. Investors across the region are eyeing more economic turbulence after Trump’s latest vow to hike his global levy to 15%, from the 10% announced just a day earlier. The markets have largely looked past concerns over tariffs and are more focused on other factors such as the broader economic landscape and the AI trade, she said. Trading in Japan and onshore China is shut today and will resume tomorrow

In FX, the dollar kicked the session off on the backfoot versus most majors but has since turned positive. Trade sensitive currencies such as Aussie dollar, Swedish krona and Norwegian krone underperform.

In rates, treasuries were marginally higher, with the 10-year yield falling one basis point to 4.07%. US natural gas prices rose as a winter storm swept the northeastern region.

In commodities, spot gold and silver have benefited from the risk aversion, up 1% and 2.6% respectively. Oil has pared the bulk of its declines, with US and Iran discussions set to resume this week. US natural gas prices jumped as powerful winter storms swept the northeastern region. Bitcoin briefly slid below $65,000 on Monday for the second time this month. Bitcoin is down 2% but recovering after a brief foray below $65,000.

The US economic calendar slate includes January Chicago Fed national activity index (8:30am), December factory orders (10am) and February Dallas Fed manufacturing activity (11am). Fed speaker slate includes Waller, speaking on the economic outlook at 8am

Market Snapshot

&P 500 mini -0.5%

Nasdaq 100 mini -0.6%

Russell 2000 mini -0.6%

Stoxx Europe 600 -0.3%

DAX -0.6%

CAC 40 +0.1%

10-year Treasury yield -1 basis point at 4.08%

VIX +0.8 points at 19.92

Bloomberg Dollar Index little changed at 1187.86

euro +0.1% at $1.1798

WTI crude -0.6% at $66.06/barrel

Top Overnight News

Iran has indicated it is prepared to make concessions on its nuclear program in talks with the U.S. in return for the lifting of sanctions and recognition of its right to enrich uranium, as it seeks to avert a U.S. attack. RTRS

Mexico Takes On Cartels as Killing of Drug Kingpin Sparks Violence… Gunmen Wreak Chaos in Mexican Coastal Retreat After Cartel Killing: WSJ

The European Union is poised to freeze the ratification process of its trade deal with the US and is seeking more details from President Donald Trump’s administration on its new tariff program: BBG

India is studying the implications for its bilateral trade deal with Washington after the US Supreme Court scrapped President Donald Trump’s decision to impose tariffs: BBG

German business confidence brightened more than anticipated in February, with an expectations index increasing to 90.5 from a revised 89.6 in January. BBG

India postponed talks on an interim trade deal with the US. China and Brazil are top winners from the Supreme Court decision, while the UK risks emerging as the main loser, according to Global Trade Alert. BBG

UK job vacancies dropped to their lowest in five years and graduate posts fell to a record low in January. BBG

The European Central Bank is asking individual lenders for details on their lending to areas including data centers amid concern over hidden credit exposures and financial-sector disruption: BBG

Blue Owl’s selloff is deepening fears about liquidity risks and excesses in the $1.8 trillion private credit market. Private equity returned fewer profits to investors for a fourth year as firms sit on $3.8 trillion of unsold assets. BBG

South Korea’s exports climbed 47.3% year on year in the first 20 days of February, fueled by AI-driven chip demand. The BOK said the country’s 2026 growth outlook improved on strong chip demand. BBG

U.S. Elite Troops Hardened by War on Terror Retrain for Arctic Combat: WSJ

Novo Nordisk Shares Plunge After Obesity Drug Fails to Beat Zepbound: WSJ

Singapore’s core CPI fell short of expectations in Jan, coming in at +1% (vs. the Street +1.5%) while the headline number was inline at +1.4%. BBG

Venezuela’s Leaders Killed the Economy. They Are Still In Charge.: WSJ

US natural gas futures jumped as the East Coast storm spiked heating demand and LNG exports climbed. BBG

Trade/Tarfiffs

US President Trump said on Saturday that he will increase the global tariff that was announced on Friday from 10% to 15% with immediate effect. Trump also stated that the 15% level is the maximum allowed by law and is still temporary, as Section 122 tariffs, and they will use the 150 days that the temporary tariff allows to work on issuing other legally permissible tariffs.

EU is set to freeze trade deal approval over US President Trump’s tariff risk, Bloomberg reports.

US officials said that tariff deal partners should honour their agreements, while USTR Greer said he sought to separate the tariff agreements from the 15% global tariff that US President Trump recently announced.

White House clarified that goods shipped under the USMCA will be exempt from the new global tariff that US President Trump announced on Friday, although risks regarding the future of the USMCA loom.

German Chancellor Merz said expect the tariff burden on the German economy to be reduced following the US Supreme Court decision, while he added that they will have a very clear European position on this, as tariff policy is a matter for the EU, not individual member states, and he will go to Washington with a coordinated European position.

US to cease collecting duties under IEEPA from 00:01EST/05:01GMT on February 24th, according to the Customs Agency.

Goldman Sachs analysts indicate most Asian economies will experience slightly lower US tariffs after the Supreme Court ruling on IEEPA tariffs, with China expected to see the largest decline.

China’s MOFCOM said it is assessing the US Supreme Court’s ruling on tariffs and urges the US to lift unilateral tariffs on trading partners. US tariffs on reciprocal goods and fentanyl breach trade rules and US law, and are not in the interest of any party.

South Korea’s Industry Minister said chips are not subject to Trump’s new tariffs and noted uncertainty regarding US tariffs refund and that consultations with the US on tariffs and trade agreements will continue.

South Korea’s Finance Minister said the trade deal with the US is still valid.

Japanese ruling LDP tax chief Onodera said the US tariff situation was a real mess following the SCOTUS tariff ruling.

US Treasury Secretary Bessent said nothing has changed on tariff revenue and trade deals; The tariff collection is closer to USD 130bln, probably not USD 175bln. Will get back to same tariff level for countries, and it will be less direct. Thinks that every country will honour the trade deals. Would call on all countries to honour their agreements and move forward.

All countries with trade agreements now drop to a 10% tariff, and the 10% rate applies until new authorities and processes kick in, according to CNBC citing a White House official.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed amid trade uncertainty as the region digested the latest tariff developments after the US Supreme Court ruled against IEEPA tariffs on Friday, prompting President Trump to impose a global 10% flat-rate tariff, which he later raised to 15% over the weekend, while there were a couple of key market closures in the region with mainland China and Japan observing holidays. ASX 200 was dragged lower with underperformance seen in tech, healthcare and real estate, while participants also reflected on a deluge of earnings releases and the recent Trump 15% global tariff rate announcement, which would increase the levies on Australia from the previously agreed 10%. KOSPI initially benefitted from the tech strength amid gains in the likes of industry heavyweights Samsung Electronics and SK Hynix, while South Korea’s Industry Minister also noted that chips were not subject to Trump’s new tariffs. However, the index then gradually gave back all its gains. Hang Seng rallied with tech stocks dominating the list of best performers in Hong Kong and with the local benchmark underpinned as a proxy to China, which is seen as the likely biggest winner from the US Supreme Court tariff ruling.

Top Asian News

China reportedly experienced robust consumer activity across sectors during the Spring Festival holiday, according to China Daily.

South Korea’s Vice Finance Minister said to closely watch financial markets.

European bourses (STOXX 600 -0.3%) show a mixed picture following the shifting tariff environment in recent days. The IBEX 35 (+0.8%) and FTSE MIB (+0.7%) outperform their peers, while the AEX (-0.3%) and DAX 40 (-0.5%) lag. European sectors are mixed. Consumer Products and Services (+1.1%), Banks (+0.8%) and Utilities (+0.9%) gain at the start of the week, aided by multiple broker upgrades for banks while Enel (+5.9%) supports the Utilities sector. The Co. updated its 2026-28 strategic plan, raising its planned investment to EUR 53bln from EUR 43bln, seeing cuts of up to EUR 700mln by 2028 and approved the execution of a new tranche of its share buyback programme. On the other hand, Technology (-1.4%) and Health Care (-1.6%) underperform. European tech giant ASML (-1.9%) seems to have been hit on OpenAI planning USD 600bln in compute spending by 2030 (prev. cited USD 1.4tln).

Top European News

German Ifo Business Climate (Feb) 88.6 vs. Exp. 88.4 (Prev. 87.6).

German Ifo Expectations (Feb) 90.5 vs. Exp. 90.3 (Prev. 89.5).

German Ifo Current Conditions (Feb) 86.7 vs. Exp. 86.3 (Prev. 85.7).

Italian Inflation Rate MoM Final (Jan) M/M 0.4% vs. Exp. 0.4% (Prev. 0.2%).

FX

DXY is slightly lower this morning and trades within a 97.35 to 97.70 range. Further pressure could see a test of its 21 DMA at 97.15. All focus today on Trump’s latest decision to impose a sweeping 15% Section 122 import tariff, following the SCOTUS decision to rule IEEPA tariffs as unlawful. The implications of the decision are mixed, with the likes of the UK and Australia now worse off, whilst the likes of Brazil and China benefit from the lower rates. SEB writes that the preliminary estimate of the global average tariff rate is now marginally lower at 12%, which is 1-2 percentage points lower than the prior rate. The Budget Lab also sees the effective tariff rate at 13.7% (prev. 16% under IEEPA taxes).

As it stands, there is some near-term certainty regarding Section 122 tariffs, which can be implemented for a maximum of 150 days. Thereafter, any extension would need to be passed through Congress. Therefore, uncertainty stems from several points; a) how the US aims to “make-up” for lost tariff revenue, b) how trade partners react to the latest levies, c) the potential use of other trade-related policies (Section 301, Section 338, Section 232).

G10s are broadly firmer against the USD; the GBP and EUR leads, whilst the Aussie lags a touch. The latter is slightly underperforming, given Australia no longer benefits from its previously negotiated 10% rate, under IEEPA.

For the EUR specifically, European Parliament’s trade chief is to propose freezing the ratification of the EU’s trade agreement with the US until they receive details from the Trump administration regarding its trade policy. On data, the German Ifo report improved from the prior and surpassed expectations, suggesting the region’s recovery is underway. Elsewhere, Japan’s ruling LDP tax chief Onodera, described the US tariff situation as a real mess. USD/JPY currently trades shy of the 155.00 mark, with the high of the day at 154.90, a touch above its 100 DMA at 154.90.

Central Banks

Fed’s Hammack (2026 voter) said inflation has made amazing progress, but is still a problem, and the Fed can be very patient in considering future rate cuts. Hammack said monetary policy is only modestly restrictive and the economy was stronger than anticipated by December, while she added that tariffs have the potential to further complicate the inflation outlook.

ECB’s Lagarde receives around EUR 140k a year as Bank for International Settlements board member, despite the ECB ban on third-party payments to staff, according to FT.

BoK Governor Rhee said FX market conditions have improved but still need to be stabilised.

Fixed Income

A relatively contained start for fixed income as markets continue to digest the latest tariff measures, and with APAC conditions thin on account of Japan’s holiday for the Emperor’s Birthday.

USTs are firmer by a few ticks in thin 112-27+ to 113-02+ parameters, within but at the top end of Friday’s 112-23+ to 112-03+ confine; as a reminder, last week’s peak was 113-14. Focus is primarily on the tariff situation, as the latest POTUS measures in response to the SCOTUS ruling have effectively lowered the global rate by a pp or two. However, we of course remain attentive to any further updates by President Trump and/or his administration in the near term. Additionally, we await remarks from Fed’s Waller (voter), commentary that will be scrutinised for his tariff take. Thus far, Logan (2026) said the SCOTUS decision has led to more uncertainty and upside inflation risks remain, but noted that policy is well-positioned. Musalem (2028) stated that if the new tariffs are one-for-one, the outlook would be unchanged, but added that the ruling could introduce uncertainty. Note, the remarks were made before the weekend’s move to 15%.

Bunds are contained, but at the lower end of c. 20 ticks parameters. The benchmark has found itself under modest pressure this morning as European cash bourses trade mixed and with futures attempting a move into the green. Ahead, supply from the bloc is scheduled, but the main focus will be on how the Hungarian block on Ukraine-related policies/sanctions by the EU shakes out.

Gilts gapped higher by 11 ticks and then climbed a handful further to a 92.51 peak. Upside that comes as the 15% global effective tariff lifts the UK above the 10% it used to be subject to, and thus skews the bias towards a March vs April cut by the BoE. The main input into that debate this week will be the appearance of Governor Bailey at the TSC.

Commodities

Crude benchmarks are more subdued in the early European session as the market continued to digest Trump’s 15% tariff decision in response to SCOTUS’ striking down his IEEPA tariffs. It’s worth noting that crude benchmarks have had their best year thus far since 2022 (the same year Russia invaded Ukraine), and as geopolitical tension continues to persist, US-Iran talks are set to resume this week.

Precious metals have kicked off the week glowing amid uncertainties from tariffs and geopolitical tension with Iran, increasing their prospect as a haven. Following the SCOTUS decision, US President Trump raised global tariffs to 15% over the weekend, fuelling market uncertainty. Following the tariff updates, the USD weakened, consequently aiding precious metals. Focus also remains on the US and Iran, with a NYT report that US President Trump is reportedly considering a targeted strike on Iran, followed by a larger attack on Iran. Iran also responded, saying that any US attacks, including limited strikes, will be considered an act of aggression. Any further escalation after both countries are set to meet on Thursday will further elevate the precious metals. XAU and XAG are trading at the upper range of USD 5117.815-5146.990/oz and USD 84.227-87.663/oz, respectively.

Copper appears to be paring some of its recent gains as markets digested the latest tariff developments, with US President Trump’s 15% flat-rate tariff seen as benefiting countries such as China and Brazil the most, while weighing on longer-term allies. Activity for the red metal has also picked up this morning, whilst mainland Chinese markets are due to reopen tomorrow. 3M LME copper trades in a tight range of USD 12,928-13,063/t. In other news, JPMorgan forecasts a copper deficit of 130k tonnes in 2026 and a 230k in the aluminium market in 2026

JPMorgan forecasts a copper deficit of 130k tonnes in 2026.

Lebanese bankers and politicians are eyeing a sale or lease of part of the central bank’s large gold reserves to rescue banks and the economy, according to FT.

Japan is mining for deep sea rare earths to combat China’s chokehold, according to FT.

Goldman Sachs raises its 2026 Q4 Brent oil forecast by USD 6 to USD 60/bbl.

Morgan Stanley raises its near-term Brent forecasts as geopolitical risk premium likely persists for a period, still expects prices to soften to USD 60/bbl later in 2026.

Chevron (CVX) announces an agreement for Iraq’s West Qurna 2 oil field.

Geopolitics – Middle East

US President Trump reportedly considers a targeted strike on Iran, followed by a larger attack and is open to deposing the Supreme Leader by force if Iran is stubborn, according to NYT.

US officials warned that if US President Trump orders strikes on Iran, Tehran could retaliate through proxies such as Hezbollah or Al-Qaeda, against American targets abroad.

US-Iran talks are set to resume in Geneva on Thursday, according to Omani mediators, while Iranian Foreign Minister Araghchi expects to meet with US Special Envoy Witkoff for discussions and reiterated that Iran will not be pressured by the military buildup in the region.

Iran said any US attack, including limited strikes, will be considered an act of aggression.

Iran Foreign Ministry spokesperson said there are discussions about the presence of IAEA’s Grossi in the third round of negotiations, Iran International reported; adds that Iran is working on a draft for any possible understanding.

Iran’s Foreign Ministry said they hope to have another round of talks with the US in the coming days. Regarding IAEA Grossi’s view that there cannot be an agreement unless the inspection of bombed nuclear facilities is allowed, Iran said it does not accept that precondition.

South Korean Embassy in Iran advised Korean nationals to leave Iran amid increasing tensions over a possible US military strike on Tehran, according to Yonhap.

Palestinian media reported that Israeli artillery shelling is targeting areas in northeast Gaza City, according to Sky News Arabia.

US officials warned if US President Trump orders strikes on Iran, Tehran could retaliate through proxies such as Hezbollah or Al-Qaeda against American targets abroad.

Palestinian media reported Israeli warplanes launched two raids on Khan Yunus in the southern Gaza Strip, according to Sky News Arabia.

US forces begin withdrawing their troops from Syria to Iraqi Kurdistan, according to Al Jazeera.

Geopolitics – Ukraine

Russian Defence Ministry said Russian forces struck Ukrainian transport, energy and fuel infrastructure.

EU Foreign Representative Kallas said she is not optimistic regarding potential progress in peace talks with Russia. Strong statements from Hungary indicate they will not change their stance on Russian sanctions today.

Hungarian Foreign Minister said they will block EU decisions in relation to Ukraine until flows to the nation resume through the Druzhba pipeline.

US Event Calendar

8:30 am: United States Jan Chicago Fed Nat Activity Index, est. -0.08, prior -0.04

10:00 am: United States Dec Factory Orders, est. -0.6%, prior 2.7%

10:00 am: United States Dec F Durable Goods Orders, est. -1.4%, prior -1.4%

10:00 am: United States Dec F Durables Ex Transportation, est. 0.9%, prior 0.9%

10:30 am: United States Feb Dallas Fed Manf. Activity, est. -0.75, prior -1.2

DB’s Jim Reid concludes the overnight wrap

As we start a new week, a great deal has happened since early Friday afternoon European time. By now, readers will be aware that the US Supreme Court ruled, by a 6–3 margin, that the administration’s use of the International Emergency Economic Powers Act (IEEPA) to impose broad based tariffs was unconstitutional.

In the immediate aftermath, the administration signaled that it would pursue a 10% global tariff under Section 122 authority. By Saturday, this was increased to 15%—which, importantly, is the maximum tariff that can be imposed using this route. Key implementation details remain unclear, including the treatment of existing trade agreements and how refunds (with interest) will be handled for tariffs collected under the now invalid IEEPA framework.

This leaves a substantial amount of uncertainty, even if markets initially welcomed the perceived clarity of “only” a 10% tariff on Friday. Looking ahead, the reality is that the 15% tariff imposed under Section 122 can only remain in place for 150 days (late July), after which Congressional approval would be required to extend it. Section 122 was designed as a temporary tool to address emergency balance of payments issues and would likely face further legal challenges if rolled over repeatedly.

That raises a key political question: will a small number of Republicans in either chamber be reluctant to support what could be framed as an extension of a consumer tax hike just three and a half months before the mid term elections? At that point, the administration faces a binary choice: try to secure an extension or allow the tariff to lapse. The latter appears the more likely outcome. In that scenario, the administration would probably pivot to other legal authorities—most notably Section 232 (national security) or Section 301 (unfair trade practices)—to re establish a more durable tariff regime. While the groundwork for such a move has almost certainly been laid, these measures are narrower in scope and would themselves be vulnerable to legal challenge.

Importantly US Trade Representative Greer seemed to suggest yesterday that trade deals already agreed will remain in place and not be exposed to the new higher rate. In addition, the new Section 122 tariff info sheet confirmed that the temporary duty taking effect midnight tomorrow will exempt various categories that were previously exempt under IEEPA tariffs, such as critical minerals, pharma, electronics and USMCA-compliant goods. Put together, the Yale Budget Lab estimates the effective tariff rate at 14% under the 15% Section 122 tariffs, down from 16% before the Supreme Court IEEPEA ruling, and that this would fall to 9% if the Section 122 tariffs expired.

This confirms the DB house view that we continue to expect the effective tariff rate to fall in 2026. Indeed, since October the average customs duty collected has already declined by around two percentage points, to roughly 11%, largely due to carve outs and exemptions. Some of this easing has been attributed to the administration’s weak showing in local elections in early November, highlighting the domestic political constraints on another aggressive tariff escalation.

It will be interesting to see if the assurances from the likes of Greer ease concerns of those who have already agreed deals. Ahead of an emergency meeting today, European Parliament trade committee chair Bernd Lange suggested freezing ratification of the Turnberry Agreement “until we have a comprehensive legal assessment and clear commitments from the US.” As he put it: “Nobody can make sense of it anymore—only unanswered questions and growing uncertainty for the EU and other US trading partners.” So the only thing that’s certain is that we are certain that we don’t quite know how this is going to pan out but net net we still believe the effective tariff rate is coming down in 2026.

The weekend news has helped S&P (-0.74%) and Nasdaq (-0.94%) futures decline along with the Dollar index (-0.34%). Euro Stoxx futures (-0.54%) are also lower. US and European bond futures are rallying slightly with US cash trading closed due to the holiday in Japan. Elsewhere in Asia markets are more bouyant with the Hang Seng (+2.29%) leading gains after significant losses last week, buoyed by strength in technology, industrial, and automotive stocks, whereas the KOSPI (+0.18%) is just about holding onto its gains after an initial rise of over +1.0%. In contrast, the S&P/ASX 200 (-0.69%) is lower.

If we can move on from the latest tariff news, we will also have more geopolitical headlines to contend with this week, as the latest round of US-Iran talks is expected in Geneva on Thursday. The talks come amid a recent buildup of US forces in the region and yesterday the New York Times was the latest outlet to report that Trump is considering an initial targeted strike against Iran in the coming days, which could be followed by a larger attack if Iran does not give in to US nuclear demands. Brent oil prices are -1.21% lower this morning trading at $70.85/bbl as we go to press as some of the weekend risk premium is being unwound.

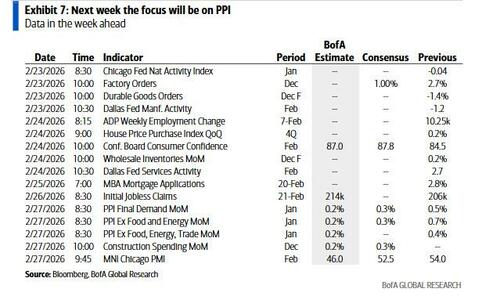

Other highlights for the week ahead include the State of the Union address in the US (late tomorrow), US PPI and preliminary CPIs in Europe (both Friday). In earnings, the focus will be on Nvidia, Salesforce (both Wednesday) and Home Depot (tomorrow). Nvidia’s earnings could be the most important of these but expect lots of headlines from the State of the Union speech.

Friday’s US PPI release—where headline and core inflation are both forecast at 0.3%—will matter less in isolation than for its implications for the core PCE deflator. While January CPI surprised to the downside relative to our expectations, the implications for core PCE continue to appear less favourable, with our economists currently looking for a 0.4% monthly increase. Depending on the strength of key PPI components such as medical services, airfares, and portfolio management fees, a 0.5% increase in January core PCE cannot be ruled out, which would lift the year-over-year rate to around 3.1%. So an important release, especially in the sub-components.

There is a fair degree of Fed speak this week, with Waller (today and tomorrow) a highlight given he dissented in favour of a 25bps cut in January due to concerns over the labour market. However, we’ve subsequently seen a firm January jobs report and a firm December core PCE print, so will he shift his stance a bit? See the day-by-day week ahead at the end as usual for the rest of the Fed speakers and the key global data.

Elsewhere in the world, we have the German Ifo today and the preliminary European February CPI prints including for countries such as Germany, France and Spain, among others, on Friday. There will also be economic sentiment measures for key economies including consumer confidence in the UK, Germany and France, as well as the ECB’s consumer expectations survey due Friday.

Over in Asia, it’s a busy week ahead for Japan with key releases including the Tokyo CPI for February and the January industrial production both due on Friday. Our Chief Japan Economist expects core CPI inflation (ex. fresh food) of 1.7% YoY (2.0% in January) and core-core CPI inflation (ex. fresh food and energy) of 2.4% (2.4% in January). For industrial production, he sees a robust 4.5% MoM gain. See more in his full week-ahead here. Elsewhere, inflation will also be in focus in Australia and our economists expect a -0.2% MoM headline print and a 0.24% MoM trimmed mean print.

Other than Nvidia on Wednesday, other tech firms reporting include Salesforce, Intuit, Snowflake and CoreWeave. Amongst US consumer firms, the focus will be on Home Depot, TJX and Lowe’s. Over in Europe, there will be results from HSBC and Allianz in financials as well as other large firms such as Deutsche Telekom, Schneider Electric, Iberdrola and Rolls-Royce.

Recapping last week now, which was full of fast-shifting narratives, moving on from AI worries to fears of geopolitical escalation between the US and Iran to a clearly upbeat tone on Friday after the Supreme Court ruling on IEEPA tariffs. With all said and done, the S&P 500 rose +1.07% (+0.69% on Friday). Tech stocks led the recovery, with the NASDAQ (+1.51%, +0.90% on Friday) rising for the first time in six weeks and the Mag-7 (+2.31%, +1.55% Friday) having its best week since November. But it was the equal-weighted S&P (+0.55%, +0.50% Friday) that ended the week at a new record high. Those gains came even as private credit worries resurfaced after Blue Owl Capital (-12.11% over the week) announced it wouldn’t re-open a withdrawal from one of its retail-focused private credit funds, which also weighed on other private equity companies.

The equity gains were even stronger in Europe, as the Stoxx 600 advanced +2.08% over the week (+0.84% on Friday) to a fresh high, with the FTSE 100 (+2.30%, +0.56% on Friday), and CAC 40 (+2.45%, +1.39% on Friday) also breaking new records. In addition to the breather from the AI turmoil and the SCOTUS overrule of IEEPA tariffs, European markets were supported by better-than-expected flash PMIs on Friday. The Euro Area composite PMI (51.9 versus 51.5 exp, 51.3 prev.) rose after three consecutive declines, led by Germany (53.1 vs 52.3 est.), supporting our European analysts’ view that Germany is starting to benefit from its fiscal expansion.

Over in the US, data releases included strong January industrial production (+0.7% m/m vs +0.4% est.) on Wednesday and initial jobless claims (206k vs 225k est.) on Thursday. While Q4 GDP growth came in weaker (+1.4% q/q vs +2.8% q/q expected) on Friday, this was accompanied by a stronger core PCE inflation reading for December (+0.4% m/m vs +0.3% m/m expected) which brought the annual rate of the Fed’s preferred inflation gauge back up to +3.0% for the first time in ten months. With investors dialling back their expectations for Fed rate cuts this year and the SCOTUS ruling raising questions over the US fiscal outlook, the Treasury curve moved higher, with the 2yr yield up +7.0bps (+1.9bps Friday) and the 10yr up +3.6bps to 4.09% (+1.7bps Friday).

European bonds outperformed, with yields on 10yr bunds (-1.7bps, -0.5bps Friday) and OATs (-4.1bps, -1.5bps on Friday) falling. And 10yr gilt yields (-6.3bps, -1.5bps Friday) saw a larger decline, after weaker labour market data on Wednesday raised expectations that the BoE will cut rates in March, with pricing of a March rate cut rising from 71% to 81% over the week.

Finally, oil saw its largest two-day jump since October 2025, as reports circulated that a conflict between the US and Iran could be imminent and Trump escalated his rhetoric against Tehran. Brent crude rose +5.92% over the week (+0.14% on Friday). Metals also rallied, with gold (+1.30%, +2.23% Friday) rising to $5,107/oz.

Tyler Durden

Mon, 02/23/2026 – 08:37