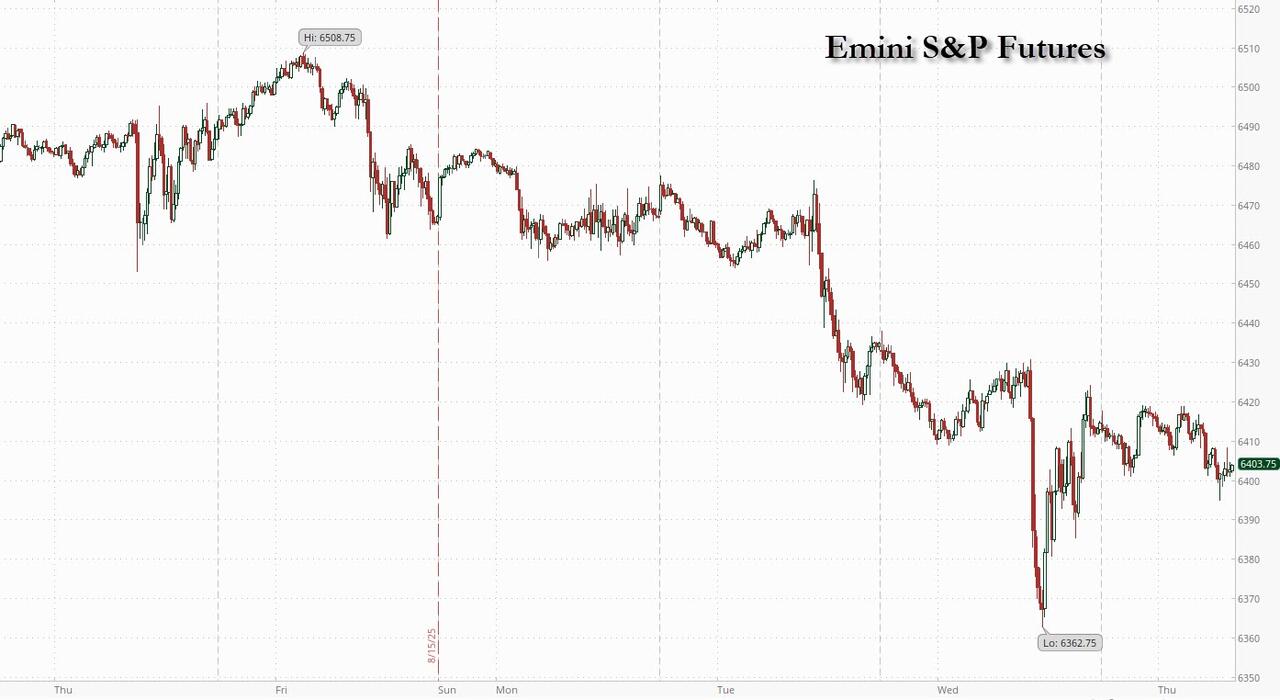

Futures Slide For Fifth Day As Jackson Hole Jitters Rise

US equity futures dropped, extending the recent selloff into its fifth day, as traders stayed guarded ahead of the Federal Reserve’s gathering at Jackson Hole. As of 8:00am, S&P 500 futures fell 0.2%, while Nasdaq 100 futures were flat after a two-day selloff that erased 2% off the index. In premarket trading, Nvidia rose 0.8% while most Magnificent Seven peers posted losses. Retail giant Walmart brought Q2 earnings season to an unofficial close after reporting an EPS miss (68c vs exp. 74c) and even though it lifted guidance (now expects net sales to rise 3.75% to 4.75% this year, versus previous forecast of a 3% to 4%) that wasn’t enough for the market, however, and the stock dropped in premarket trading. European stocks dropped 0.3%, erasing an earlier gain, and snapping a three-day winning streak. US treasuries fell, pushing the yield on the 10-year higher to 4.31%. The dollar strengthened and reversed all of yesterday’s losses while Brent crude rose to the highest in two weeks even as the rest of the commodity complex was mixed. It’s a busy economic calendar: we get weekly jobless claims and August Philadelphia Fed business outlook (8:30am), S&P Global US PMIs (9:45am) and July leading index and existing home sales (10am). The Fed speaker slate includes Atlanta Fed President Bostic at 7:30am, the last central bank official slated to speak before Chair Powell’s discourse at Jackson Hole Friday

{kind=link}

In premarket trading, Mag 7 stocks are mostly lower (Nvidia +0.8%, Tesla unchanged, Microsoft -0.1%, Alphabet -0.2%, Amazon -0.3%, Meta -0.3%, Apple -0.5%). Here are some other notable premarket movers:

Aegon ADRs (AEG) are up 5% after the Dutch insurance company posted better-than-expected results and said it planned to increase its share buyback. Management said the company may redomicile to the US, a move that Morgan Stanley said would “make sense.”

Boeing Co. (BA) gains 1.5% as the company is heading closer toward finalizing a deal with China to sell as many as 500 aircraft, according to people familiar with the matter.

Canadian Solar (CSIQ) falls 11% after forecasting third-quarter revenue below analyst expectations.

Coty (COTY) falls 20% after the personal care products company forecast steep sales declines and reported a wider-than-expected loss for the fourth quarter.

Dayforce (DAY) rises 1.4% after entering into a definitive agreement with Thoma Bravo to become a privately held company in an all-cash transaction with an enterprise value of $12.3 billion.

Hewlett Packard Enterprise (HPE) gains 3.1% after being raised to overweight from equal-weight at Morgan Stanley as analysts note that recently-closed Juniper deal will be an earnings upside.

SharkNinja (SN) trades lower by 2% as holders affiliated with Chairperson CJ Xuning Wang offer 5 million shares in the household-appliance maker via JPMorgan, BofA Securities.

Two Harbors Investment (TWO) falls 3% after the mortgage REIT resolved litigation with Pine River via a one-time $375m cash settlement and cut its quarterly dividend to 34c a share.

Walmart (WMT) slips 2.4% after the world’s largest retailer posted second quarter profit that disappointed.

In corporate news, FanDuel, the online gambling division of Flutter Entertainment, is teaming up with CME Group, the largest US derivatives exchange, to offer bets on stocks, commodity prices and even inflation. Google introduced a new slate of consumer gadgets, including several smartphones, a watch and new wireless earbuds, all meant to show off the company’s latest advances in artificial intelligence. Musk‘s Starlink service is said to be in conversation with Emirates and other Middle Eastern airlines, with winning business in the region potentially marking a watershed moment in Starlink’s global competition.

This week has seen pressure on momentum names (read tech stocks) particularly the largest names, amid worries that their sharp rally since April has moved too far, too fast. Traders are also cautious as the Jackson Hole symposium kicks off later today, with investors awaiting Fed Chair Jerome Powell’s speech at 10am ET Friday for guidance on the path for interest rates. Despite the pullback in stocks this week, the VIX hasn’t really budged, and Goldman said it’s time to buy the dip in momentum stocks (and the overall market according to JPMorgan).

The market’s direction today will also be shaped by PMIs, home sales data and Walmart earnings (which missed but boosted its revenue forecast). For the euro area, the Composite Purchasing Managers’ Index compiled by S&P Global grew at the quickest pace in 15 months as manufacturing exited a three-year downturn.

“What we are currently seeing is profit-taking and a natural flight to quality ahead of Jerome Powell’s speech in Jackson Hole,” said John Plassard, head of investment strategy at Cité Gestion. But “let’s not beat around the bush: this is not the end of tech, and even less so for stocks linked to artificial intelligence.”

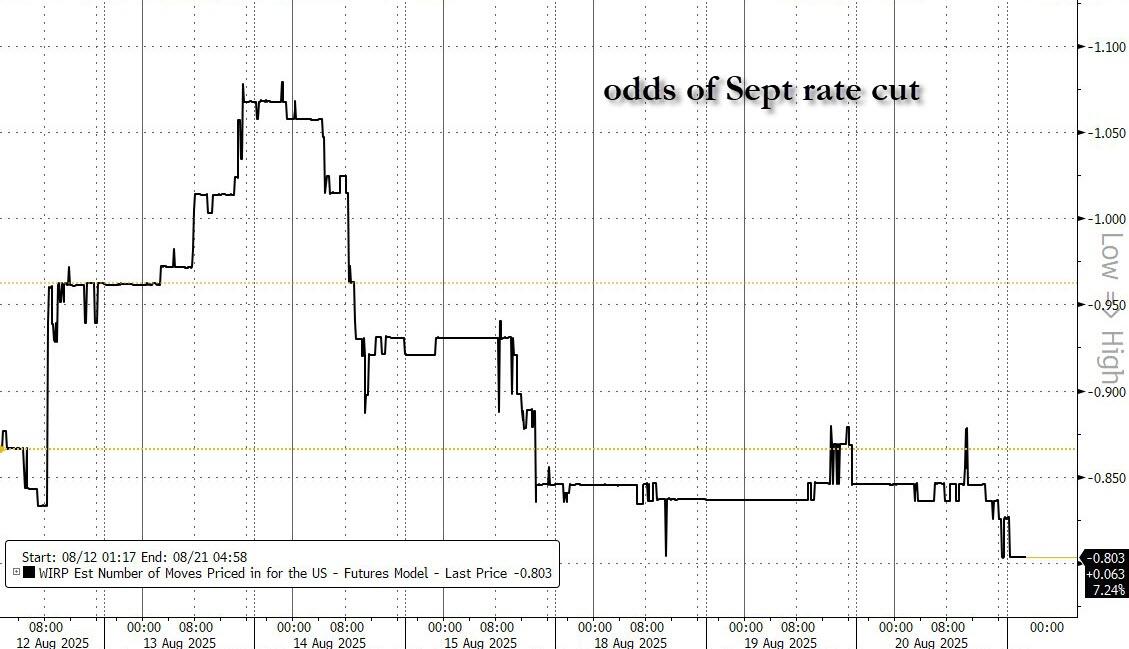

Swaps are currently pricing in 80% chance of a Fed quarter-point cut in September, and at least three more over the next year, some strategists warned that the market may be too optimistic about the pace and depth of easing.

{kind=link}

“All it’s going to take is a bit of stickiness in inflation and actually a labor market print which shows it’s not falling off a cliff for the market to say, ‘hang on,’” Karen Ward, chief market strategist for EMEA at JPMorgan Asset Management, told Bloomberg TV.

In his latest effort to stack the Fed board, Trump and his allies are demanding Fed Governor Lisa Cook resign over alleged owner-occupancy fraud. For her part, Cook signaled her intention to remain at the central bank.

Yesterday, the latest FOMC Minutes for the July 29-30 meeting showed most officials viewed inflation risks as outweighing labor-market concerns, with tariffs fueling a growing divide within the rate-setting committee, though the discussions came before subsequent dramatic dire revisions to jobs data.

On the geopolitical front, US Vice President JD Vance said negotiations over ending Russia’s war in Ukraine are focused on security guarantees for Ukraine and territory Russia wants to control — including Ukrainian territory that Russia isn’t occupying — as the US tries to broker a peace deal between the two nations. Brent crude rose 0.8%.

The Stoxx 600 falls 0.2% with media, consumer product and chemical shares leading declines. Nordics represented several of the region’s biggest movers, with hearing-aid maker GN Store Nord surging 19% after reporting earnings, while Norwegian oil firm Aker BP jumped after a large oil find in the North Sea. UK retailer WH Smith plunged after signaling North American profit will be much weaker than previously hoped. Here are the biggest movers Thursday:

Aegon shares jump as much as 7.4%, reaching a 10-year high, after the Dutch insurance company posted better-than-expected results and said it planned to increase its share buyback

GN Store Nord gains as much as 19% after the Danish hearing aid and audio equipment firm’s 2Q earnings beat estimates across the board. Analysts see a strong showing following weaker reports from European peers

Aker BP shares rise as much as 4.6% after the Norwegian industrial investment company announced a “significant oil discovery” as it completed the Omega Alfa exploration campaign in the Norwegian North Sea

ALK-Abello gains as much as 5.9%, the most since May, after the Danish allergy drugmaker reported 2Q earnings. Analysts say that while the report holds few surprises after the company pre-released figures, they reassured

Salmar gains as much as 6.1%, the most since April, after the Norwegian salmon firm reported its latest earnings, which DNB Carnegie described as in line, with “positive” cost and volume guidance for the rest of the year

DNO gains as much as 11%, the most since 2023, after the Norwegian oil company reported its latest earnings and hiked its dividend per share by around 20%. DNB Carnegie expects the raised payouts to support the shares

Renishaw shares rise as much as 8.9% to the highest since February after the precision measuring equipment maker indicated its adjusted pretax profit for the full year will be at the high end of the guidance range

WH Smith shares plummet as much as 38%, the biggest drop on record, after the retailer warned headline trading profit from North America will be significantly lower than previously hoped

CTS Eventim shares slide as much as 20%, the most since 2007, after the events firm reported 2Q Ebitda well below estimates. The firm cited “intense and persistent cost pressures” for live events and headwinds in other divisions

Novonesis falls as much as 7.8% after the Danish biotechnology group reported earnings. Analysts say a profitability miss and merely reiterated margin guidance disappointed, and will lead to slight consensus cuts

European stocks in the beauty and personal care sector fell after US company Coty reported a wider adjusted loss per share in 4Q than analysts expected, while forecasting steep sales declines will continue

Sensirion falls as much as 8.2% after both Berenberg and Research Partners downgraded the semiconductor device manufacturer to hold from buy following its first-half earnings

UK housebuilders are under pressure on Thursday as London builders are taking longer to start home constructions after receiving permits, with a slump in demand threatening to derail the government’s plan to build 1.5m homes

Kojamo declines as much as 5.9% following its second-quarter results, with JPMorgan retaining its underweight rating and a cautious stance on the real estate company

Earlier in the session, Asian stocks traded in a tight range, as a rebound in some tech stocks was offset by declines in Japan. The MSCI Asia Pacific Index fell 0.2%, with Japan’s Daiichi Sankyo among the top drags after a series of block trades at a discount. Hon Hai and TSMC were among the biggest boosts for the gauge. Shares hit a record high in Australia, while those in South Korea and Taiwan also advanced. Investors are awaiting cues from the Jackson Hole symposium, where Federal Reserve Chair Jerome Powell is expected to speak on Friday. Nvidia’s results next week will be another key test, with expectations for improving global tech earnings having bolstered sentiment. Equities also traded higher in mainland China, Vietnam and New Zealand on Thursday. MSCI equity gauges for every nation in the region are trading above their 200-day moving averages for the first time since 2021, according to Sentimentrader.com.

In FX, the euro and pound both edge higher against the greenback after the better-than-expected PMI data. The Norwegian krone is the best-performing G-10 currency, rising 0.5% after Norway’s GDP grew more than forecast in the second quarter.

In rates, treasuries are under pressure in early US trading amid steeper losses for most European bond markets sparked by stronger-than-anticipated August preliminary PMI gauges. US yields are higher by 1bp-2bp, the 10-year by about 1.8bp at 4.31%, vs increases of 3bp-4bp for UK and most euro-zone counterparts. US session features 30-year TIPS reopening auction at 1pm New York time. Week’s major focal point is Fed Chair Powell’s Jackson Hole speech on Friday. UK gilts are leading declines in European government bonds after the UK private sector expanded at the strongest pace in 12 months. UK 10-year yields rise 3 bps to 4.70%. German 10-year borrowing costs add 2 bps to 2.73% after the euro area’s private sector grew at the quickest pace in 15 months.

Looking at today’s calendar, US economic data calendar includes weekly jobless claims and August Philadelphia Fed business outlook (8:30am), August preliminary S&P Global US PMIs (9:45am) and July leading index and existing home sales (10am). Fed speaker slate includes Atlanta Fed President Bostic at 7:30am, the last central bank official slated to speak before Chair Powell’s discourse at Jackson Hole Friday

Market Snapshot

S&P 500 mini -0.1%

Nasdaq 100 mini little changed

Russell 2000 mini -0.3%

Stoxx Europe 600 -0.2%

DAX -0.1%

CAC 40 -0.5%

10-year Treasury yield +1 basis point at 4.3%

VIX +0.2 points at 15.93

Bloomberg Dollar Index little changed at 1207.17

euro little changed at $1.1658

WTI crude +1% at $63.35/barrel

Top Overnight News

Fed reserve governor Lisa Cook has defied calls from Trump to resign, saying she has “no intention of being bullied to step down” after FHFA Director Bill Pulte posted he was making a criminal referral based on a mortgage application from four years ago: FT

The Texas House approved a new congressional map that may add up to five GOP seats in the 2026 midterms. In California, the state’s top court declined to halt Governor Gavin Newsom’s own redistricting plan, which he’s pursuing to offset the moves in Texas and elsewhere. BBG

Meta Platforms has frozen hiring in its artificial-intelligence division after spending months scooping up 50-plus AI researchers and engineers. WSJ

South Korea will unveil an additional $150 billion in US investment from private firms during Lee Jae Myung’s summit with Trump, local media said. BBG

The euro area’s private sector expanded at the quickest pace in 15 months, PMI data showed, adding to evidence of the region’s resilience. Manufacturing ended a three-year downturn despite higher US levies. UK composite PMI also rose more than expected. BBG

China is aggressively trying to persuade domestic tech firms to avoid buying Nvidia chips following “insulting” remarks from Commerce Sec Lutnick. FT

Japan’s 20-year yields hit their highest since 1999 amid fiscal concerns and fading demand from key investors. Yields on 30-year notes approached a new high. BBG

India’s flash PMIs for Aug are strong, including manufacturing (59.8, up from 59.1 in Jul) and especially services (65.6, a big jump from 60.5 in Jul). S&P

Russia warned on Wednesday that it should effectively hold veto power over any action to assist Ukraine after a peace deal is reached, rendering planned Western security guarantees for Kyiv moot and delivering a setback to negotiations championed by President Trump. Russia’s Lavrov also played down likelihood of a summit between Russia/Ukraine leaders happening soon. WSJ

Trade/Tariffs

China’s Commerce Minister talked with Kazakhstan’s Trade Minister and said China is ready to work with Kazakhstan to promote the upgrading of bilateral trade, while China is ready to strengthen cooperation in emerging fields and accelerate the cultivation of new trade formats.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed, albeit with a mildly positive bias as the region attempted to shrug off the lacklustre lead from Wall St, where sentiment was dampened amid continued tech weakness and hawkish-leaning FOMC Minutes. ASX 200 outperformed amid a slew of earnings releases and breached the 9,000 level for the first time in history. Nikkei 225 was dragged lower by weakness in pharmaceuticals and automakers, with the latter not helped by reports that Japanese automakers are passing some of the expense of US tariffs through to American car buyers, which is a change from their strategy of absorbing the impact. Hang Seng and Shanghai Comp were mixed with the Hong Kong benchmark led lower by underperformance in tech stocks including Baidu and Xiaomi, despite both recently reporting a jump in profits, while the mainland remained propped up following the PBoC’s liquidity efforts.

Top Asian News

Asian petrochemicals shares rise as China is set to launch a sweeping overhaul of its petrochemicals and oil refining sector to phase out smaller facilities and target outdated operations for upgrades.

Chinese biomedical shares rise after Premier Li Qiang toured company sites and emphasized the need to increase scientific and technological backing as well as policy support for the sector.

Chinese crypto-linked stocks rally after a report that the government is considering a plan for expanded yuan use and stablecoins.

Sonic Healthcare shares slide as much as 10%, the most since May 2024, after the Australian diagnostics and pathology firm reported net income for the full year that missed the average analyst estimate.

South Korea’s Financial Services Commission urges financial firms to provide necessary support in the course of the nation’s petrochemical industry restructuring, according to a statement from the financial regulator.

European bourses (STOXX 600 -0.2%) are trading with little in the way of a clear bias. Geopolitical tensions resurfaced early doors after Ukraine’s Air Force stated that Russia used 574 drones and 40 missiles in an overnight attack. Focus also on EZ PMIs which saw the saw the composite move further into expansionary territory. European equity sectors show a mostly negative tilt with stock-specific updates relatively light. Energy names sit at the top of the leaderboard amid upside in underlying crude prices. To the downside, Media names lag with Wolters Kluwer (-2.2%) a notable underperformer in the sector following a PT reduction at Morgan Stanley.

Top European News

The euro area’s private sector expanded at the quickest pace in 15 months, PMI data showed, adding to evidence of the region’s resilience. Manufacturing ended a three-year downturn despite higher US levies. UK composite PMI also rose more than expected.

FX

Steady trade for DXY after a session yesterday, which was dominated by newsflow surrounding the Fed. US rates markets endured a steepening of the curve, led by the front-end amid reporting that President Trump could fire Fed Governor Cook amid alleged mortgage fraud. Thereafter, attention pivoted to the account of the July policy announcement, which was viewed with a hawkish lens. DXY sits towards the mid-point of Wednesday’s 98.07-44 range.

EUR saw some pressure early doors after comments from Ukraine’s Air Force that Russia used 574 drones and 40 missiles in an overnight attack. This has helped reinforce the message that despite a more encouraging direction of travel for peace talks, the reality on the ground remains tense between Russia and Ukraine. Some of the pessimism was faded following flash PMI metrics from across the Eurozone with a solid report from France kickstarting the recovery and followed by a mostly positive German release. The EZ-wide print saw the composite move further into expansionary territory. EUR/USD sits just above its 50DMA at 1.1645.

JPY is fractionally weaker vs. the USD after a session of gains on Wednesday, which were in part driven by a refocus on interest-rate differentials as the front-end of the US curve was dragged lower by the possibility of Fed Governor Cook being removed from her position. Overnight, there was little follow-through seen from mixed flash Japanese PMI metrics for August, which saw the manufacturing metric tick higher from its prior (but remain sub-50) and services fall from its previous (but remain above 50). USD/JPY sits within Wednesday’s 146.87-147.81.

GBP is the marginal outperformer across the majors following a better-than-expected outturn for flash August services and composite PMIs, which rose further into expansionary territory. Cable has picked up from its 1.3436 session low with a current session peak at 1.3476.

Antipodeans are both are a touch softer vs. the USD with NZD unable to launch much of a recovery from Wednesday’s RBNZ-induced losses and AUD failing to garner any support from upticks in flash PMI metrics for August. AUD/USD is at its lowest level since June 23rd with focus on a test of the 0.64 mark and the 200DMA @ 0.6386.

Fixed Income

USTs began the European session around the unchanged mark, with price action fairly tentative in a continuation of the lacklustre trade seen overnight. As the European morning kicked off, trade has largely been dictated by Bunds, which have had a number of regional PMIs to digest (more in Bunds below). US paper currently trades lower by a handful of ticks, in a 111-24 to 111-29 range, currently contained within the prior day’s confines. Looking ahead, weekly initial jobless claims and US PMIs alongside Fed speak from Bostic and Schmid.

Bund Sept’25 started the European session around the unchanged mark and then slipped on both the French and then German PMI metrics, which overall highlighted the ongoing strength in the Manufacturing sector, whilst Services was a little more subdued. The EZ wide figure confirmed the strong Manufacturing / slightly softer Services picture, with the former surprisingly climbing into expansionary territory. In terms of the commentary, it highlighted that “U.S. trade policy is leaving its mark. Foreign orders in the eurozone manufacturing sector have declined for the second month in a row”.

Gilts traded subdued throughout the European morning, taking leads from the hotter-than-expected PMI metrics in Europe. Into the region’s own figures, UK paper traded lower by around 15 ticks. Thereafter, on the region’s own PMI metrics, Gilts fell from 90.99 to 90.91 before trimming half of the move; currently trading in a 90.82 to 91.22 range. Unlike in Europe, the upside in Composite was thanks to strength in the Services sector whilst Manufacturing was subdued. It is worth highlighting that the accompanying release was fairly downbeat; “Payroll numbers also continue to be cut at an aggressive rate”; “the demand environment remains both uneven and fragile”.

France sells EUR 10.499bln vs exp. EUR 8.5-10.5bln 2.40% 2028, 2.50% 2030, and 2.70% 2031 OAT.

Commodities

Modestly positive trade in the crude complex in what has been a quiet session thus far, but with eyes remaining on geopolitics amid a couple of notable updates. WTI resides in a USD 62.78-63.40/bbl range while Brent sits in a USD 66.88-67.49/bbl parameter.

Softer trade across precious metals, albeit modest in spot gold and silver, with newsflow on the lighter side and with the metals largely moving in tandem with the dollar. Price action this morning sees the precious metals complex subdued, with spot gold on either side of its 50 DMA (~3,348.10/oz) in a USD 3,334.28.56-3,352.30/oz range.

Subdued price action across the base metals complex – in fitting with the broader market mood as traders look ahead to the Jackson Hole Symposium. 3M LME copper prices reside in a USD 9,689.45-9,739.40/t range.

Geopolitics: Middle East

UN Secretary General Guterres called for an immediate ceasefire in Gaza to avoid massive death and destruction in Gaza City, while he called for Israel to reverse its decision to expand the illegal settlement expansion in the West Bank.

Geopolitics: UKRAINE

Ukraine’s Air Force said Russia used 574 drones and 40 missiles in an overnight attack.

Moscow to host first nuclear summit on September 25″, according to Al Arabiya.

Ukraine President Zelensky said Kyiv wants to have an understanding of security guarantees within 7-10 days, followed by bilateral and trilateral leaders meetings. If Russia is not ready for a bilateral leaders meeting, Ukraine and Europe want to see strong US reaction. ‘Flamingo’ missile is Ukraine’s most successful missile, mass production expected by early next year. Ukrainian proposal for US drone deal entails production worth USD 50bln over five years. Ten million drones expected to be produced yearly as part of the deal. China not included in security guarantees because China did not help after the Russian invasion. On Budapest as venue for peace talks: “For now, this is challenging.”Ukraine will not legally recognise Russia’s occupation of its territories. There is no signal that Moscow is prepared to end the war and have substantial conversations. Ukraine has tested a new long-range missile.

Ukrainian President Zelenksy’s Chief of Staff warned against repeating mistakes of the 1994 Budapest memorandum on security guarantees and said Ukraine’s allies have started active work on the military aspect of security guarantees, while a contingency plan is being developed with partners in case Russia extends the war or violates agreements from leaders’ meetings.

US VP Vance said on Fox News that Europeans are going to have to take the lion’s share of the burden in security. It was separately reported that a Pentagon top policy official told a small group of allies Tuesday night that the US plans to play a minimal role in any Ukraine security guarantees, according to POLITICO citing Defense Undersecretary for Policy Colby.

Turkish defence ministry source said ceasefire between Russia and Ukraine needed before discussing peacekeeping mission framework, via Reuters citing sources.

Russia attacked a key Ukrainian gas compressor station vital for storage operations, according to Reuters sources.

Ukraine military said it hit a Russian oil refinery, drone warehouse and fuel base overnight.

Geopolitics: Other

North Korea has a heavily fortified, covert military base that could house its newest long-range ballistic missiles, which are potentially capable of striking the US mainland, according to a new report cited by the WSJ.

US Event Calendar

8:30 am: Aug 16 Initial Jobless Claims, est. 225.33k, prior 224k

8:30 am: Aug 9 Continuing Claims, est. 1960k, prior 1953k

8:30 am: Aug Philadelphia Fed Business Outlook, est. 6.5, prior 15.9

9:45 am: Aug P S&P Global U.S. Manufacturing PMI, est. 49.7, prior 49.8

9:45 am: Aug P S&P Global U.S. Services PMI, est. 54.2, prior 55.7

9:45 am: Aug P S&P Global U.S. Composite PMI, est. 53.5, prior 55.1

10:00 am: Jul Leading Index, est. -0.1%, prior -0.3%

10:00 am: Jul Existing Home Sales, est. 3.92m, prior 3.93m

10:00 am: Jul Existing Home Sales MoM, est. -0.25%, prior -2.7%

DB’s Jim Reid concludes the overnight wrap

While the headline market moves were fairly muted over the past 24 hours, investors had to navigate a couple of major narratives. One was renewed concerns over Fed independence as President Trump suggested that Fed Governor Cook should resign, which pushed gold (+0.98%) to its best day since the weak July payrolls report on August 1. The other was continued pressure on tech stocks as the Mag-7 (-1.11%) posted consecutive declines of more than 1% for the first time since the post-Liberation Day sell-off in early April. This sent the S&P 500 (-0.24%) lower for a fourth session running even as the index recovered most of its -1% intra-day decline.

The topic of the US administration’s influence over the Fed came back into the headlines as Trump posted that Fed Governor “Cook must resign, now!!!”. His post followed news that Federal Housing Finance Agency (FHFA) Director Bill Pulte had written a criminal investigation referral letter to Attorney General Pam Bondi alleging that Governor Lisa Cook may have committed mortgage fraud. Pulte has been one of the staunchest Fed critics within the administration, earlier calling for an investigation into Chair Powell over the Fed’s building renovations. Yesterday Pulte claimed that the allegations give Trump “cause to fire” Governor Cook. Later in the day, Cook said in a statement that she had “no intention of being bullied to step down from my position”.

Governor Cook was nominated to the Federal Reserve Board by Joe Biden in 2022 and our US economists see her as leaning slightly towards to dovish end within the FOMC. Were Governor Cook to resign or be fired, that would create another opening for Trump to fill on the seven-person Board. With Stephen Miran nominated to take the seat recently vacated by Governor Kugler and two Fed Governors – Bowman and Waller – dissenting to vote for a rate cut at the July meeting, this would increase the prospects of a dovish majority emerging on the Board, especially if Chair Powell relinquishes his seat next year. That said, if concerns over threats to Fed independence increase, Powell could choose to serve out the rest of his board term (which ends in 2028) even after his term as Chair ends next May.

The news was a reminder of the lingering concerns over future Fed independence and risks of fiscal dominance, though the extent of the market reaction was fairly modest. The most sustained reaction was in gold (+0.98%) as mentioned at the top. The dollar index fell by a couple of tenths following the news but was back to little changed (-0.05%) by the close. Front-end yields fell by 3-4bps, but that move came amid a broader risk-off mood early in the session and also reversed later on.

By the close, 10yr Treasury yields were -1.5bps lower at 4.29% but 2yr yields were unchanged at 3.75%. This curve flattening was also supported by hawkish-leaning minutes of the July FOMC meeting. These showed that most of the FOMC “judged the upside risk to inflation” as greater than the “downside risk to employment”, with several participants noting the “risk of longer-term inflation expectations becoming unanchored”. That said, the minutes did suggest easing would be warranted “if labor market conditions were to weaken materially”, and given the weak jobs report that followed the July decision, the relative focus on employment versus inflation risks will likely have shifted since. So, while pricing of September rate cut inched down yesterday to its lowest since the August 1 jobs report, a 25bp cut was still 83% priced.

US equities saw an even larger round trip, with a rout for tech stocks early in session leaving the S&P 500 more than -1% down intra-day but recovering to -0.24% by the close. The NASDAQ fell -0.67%, having been almost -2% down early on, while the Mag-7 slid by -1.11% after a -1.67% drop on Tuesday. The last time the Mag-7 saw consecutive declines of more than 1% was during the post-Liberation Day collapse in early April. The tech sell-off may have been exacerbated by reporting of an MIT study claiming that 95% of enterprises adopting AI saw no measurable increase in profits. Here at DB research, we remain optimistic on the productivity impact of AI but the report is a reminder that successful integration of new technologies takes time and that it’s still uncertain who will be the biggest end beneficiaries of the AI wave. Outside of tech, US equities had a decent day, with most of the S&P 500 sectors advancing, led by energy (+0.86%) which benefited as Brent crude prices rose +1.60% to $66.84/bbl.

Turning to Europe, we saw the latest rate decision from Sweden’s Riksbank, which kept rates on hold at 2.00% as expected while continuing to signal “some probability of a further interest rate cut this year”. Market pricing of another rate cut by year-end inched down to 88% from 91% the day before. We also heard from ECB President Lagarde, who said that “Recent trade deals have alleviated, but certainly not eliminated, global uncertainty” and noted that the euro area economy was likely to see slower growth this quarter. So that was arguably a bit more dovish in tone than her press conference last month, though Lagarde gave away little on the policy outlook.

Expectations of ECB easing ticked up on the day, with 21bps of cuts now priced by next June, the highest this has been in almost two weeks. In turn, European government bonds rallied with 10yr bund yields falling -3.2bps to 2.72%, and OAT (-2.2bps) and BTP (-3.0bps) yields similarly moving lower. Bunds were also supported by Germany’s PPI inflation print (-1.5% yoy vs -1.4% expected) falling to a 13-month low in July. Meanwhile, the euro area final headline CPI for July came in line with the flash reading at 2.0%.

Over in the UK, gilts yields saw a larger rally, with 10yr yields down -6.8bps to 4.67%. This came despite July CPI coming in slightly stronger than expected at +3.8% yoy for both headline and core inflation (vs +3.7% expected), which marked the highest headline reading since January 2024. A saving grace noted by our UK economist Sanjay Raja is that with the volatile transport and travel services components driving the upside, most core services metrics ticked down on the month (see Sanjay’s reaction here). Money markets moved to price in more BoE easing for early 2026 following the release, with the amount of cuts priced by next June rising +5.5bps to 38bps.

The repricing in UK rates helped the FTSE 100 outperform (+1.01%). The Stoxx 600 rose +0.24% but continental indices were more subdued, with the CAC (+0.06%) posting a marginal gain but the DAX (-0.69%) and FTSE MIB (-0.36%) losing ground.

Overnight, sentiment has turned risk-on again in most Asian equity markets. The KOSPI is up +0.73%, while the S&P/ASX 200 (+0.90%) is leading the way after a strong flash PMI print. Australia’s composite PMI rose from 53.8 to 54.9 and the manufacturing index reached a 35-month high of 52.9. Chinese stocks are on also the rise, with the CSI (+0.72%) and the Shanghai Composite (+0.33%) higher though the Hang Seng (-0.10%) is lagging. Meanwhile, US equity futures on the S&P 500 and NASDAQ 100 are little changed after yesterday’s decline.

The one Asian market defying the regional positive trend is Japan, with the Nikkei down -0.58%. That comes despite Japan’s composite PMI rising to a 6-month high of 51.9 in the August flash reading (up from 51.6 in July), as stabilization in manufacturing (49.9 vs 48.9 in July) has offset slowing services growth (52.7 vs 53.6 in July). However, long-end JGB yields are inching higher to new multi-decade highs ahead of the July inflation print tomorrow morning, with the 30yr yield up +0.7bps to 3.18%, a new all-time high since this tenor was introduced in 1999.

To the day ahead, the main highlight will be the August flash PMI prints in Europe and the US. Other data releases include the August Philadelphia Fed business outlook, July existing home sales and weekly jobless claims in the US as well as August Eurozone consumer confidence. Earnings include Walmart, Intuit, and Workday. The Fed’s Bostic is due to speak, while the Kansas City Fed’s Jackson Hole symposium begins this evening with the main events on Friday and Saturday.

Tyler Durden

Thu, 08/21/2025 – 08:07