Goldman Finds “Sharp Declines” In Import Prices As Foreigners Absorb Trump’s Tariffs

Back in late June, we were first to point out something startling: contrary to conventional wisdom according to which prices of heavily-tariffed goods would surge and spark runaway inflation (just skim this from certified idiot Paul Krugman), we found just the opposite, namely that Japanese passenger car export prices had plunged by the most on record, demonstrating that it was foreign producers that were eating the bulk of the tariffs, certainly in this particular case.

well would you look at that: guess who is eating all those tariff costs (hint, it’s not US consumers) pic.twitter.com/iwdKyeqTII

— zerohedge (@zerohedge) June 22, 2025

Three days later, our chart ended up in front of Fed Chair Jerome Powell during his periodic grilling in Congress, where he was unable to give a clear explanation as to why the export prices of Japanese autos would be plunging in response to sharply higher tariffs (the answer, of course, is simple: foreign producers simply can not pass through costs to the US market without losing much if not all of their market share, so they have no choice but to eat the loss).

well would you look at that: three days later Powell has to discuss this chart https://t.co/6AfkRRSjJp pic.twitter.com/SOGjff2Fsl

— zerohedge (@zerohedge) June 25, 2025

Fast forward to today when Goldman, similar to Morgan Stanley over the weekend, tried to analyze why those tariffs which it – and so many other economists predicted incorrectly – would already have sent inflation soaring, have failed to do so. While there is a bunch of stuff in the report (which pro subs can read at their leisure here), what was most notable is the “discovery” that it’s not just Japanese car makers.

As Goldman’s Jan Hatzius reveals, “we find that US import prices on tariffed goods have declined somewhat, suggesting that foreign exporters have absorbed some tariff costs by lowering their export prices to the US, unlike during the 2018-2019 trade war.”

Our updated analysis shows that a 1pp increase in the product-level tariff rate led to a 0.25% cumulative decline in import prices over the first three months of implementation, with minimal impact thereafter.

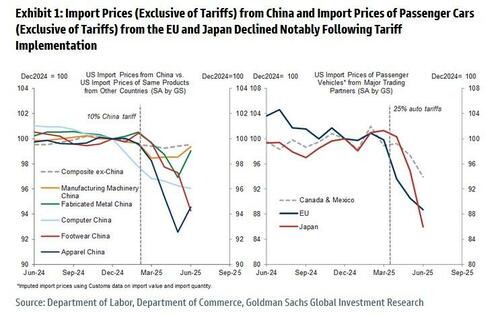

Of course, here Goldman had to mix fact with projection to not sound like a bunch of wrong, confused career economists. When one strips away hypothesis and forecast, here is what actually happened: “following the implementation of China and auto tariffs, import prices (exclusive of tariffs) of both consumer and non-consumer goods from China, as well as import prices of passenger cars (exclusive of tariffs) from the EU and Japan, all experienced sharp declines.”

{kind=link}

Looking forward, Goldman concludes that whereas “foreign exporters had absorbed 14% of the cost of all tariffs implemented so far through June, their share will rise to 25% if the more recent tariffs follow the same pattern as the earliest tariffs on China.“

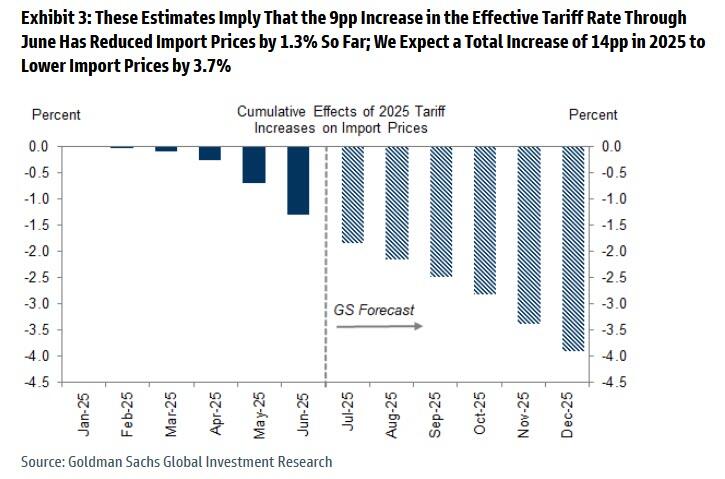

This also means that the 9% increase in the effective tariff rate through June has reduced import prices by at least 1.3% so far, and that the total 14% increase in the effective tariff rate that Goldman expects in 2025 will likely reduce import prices by 3.7%, if not much more assuming foreign producers continue to keep prices reduced to remain competitive with lower-cost domestic producers.

{kind=link}

The rest of the Goldman note goes on to do what Morgan Stanley tried to do yesterday: forecast just when all those tariffs will eventually finally show up in inflation… an exercise they have to do because both giant banks were very wrong in incorrectly assuming that inflation would already be far higher than it is so far. Don’t be surprise if tomorrow’s CPI comes in tame yet again, prompting even more revisions to Goldman’s inflation ETA.

Much more in the full Goldman note, available to pro subscribers.

Tyler Durden

Mon, 08/11/2025 – 15:45