Kite Realty Group (NYSE: KRG) delivered impressive Q4 2025 earnings results. FFO totaled $2.10 for the full year 2025. Also, management demonstrated solid execution in Q4. So the market responded positively to KRG’s performance. Market cap reached $5.3 billion, reflecting growing investor confidence.

KRG Q4 2025 Earnings: Financial Performance

The company’s Q4 2025 earnings showed momentum. Operations improved across the board. FFO came in at $0.52 in Q4. This compares to $0.55 in Q4 2024. So full-year 2025 FFO reached $2.10. Also, core FFO came in at $0.51 for Q4. It was $2.06 for the full year. In fact, these results exceeded initial guidance.

KRG Q4 2025 Earnings: Key Takeaways

Same-property NOI growth of 2.9% for full year 2025, with Q4 growth of 1.7%

Portfolio leased at 95.1%, up from 94.2% in prior year

Leasing volume reached 4.6 million SF with 13.8% blended cash spreads

ABR per SF improved to $22.63, up from $21.15 in prior year

Market cap of $5.3 billion reflects investor confidence

Investment-grade credit ratings (BBB from S&P, Baa2 from Moody’s)

A debt service coverage ratio of 4.2x demonstrates financial stability

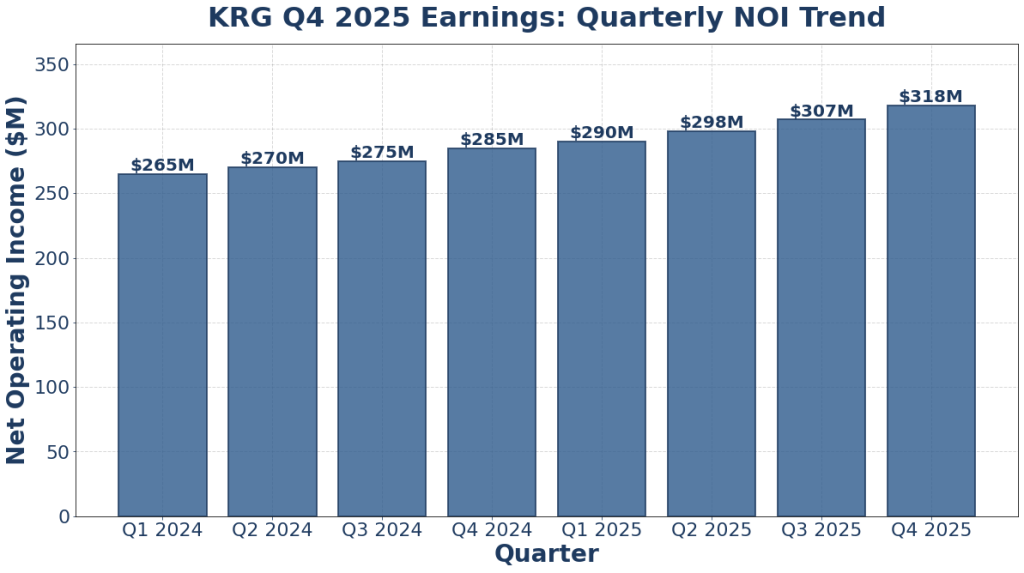

Figure 1: KRG Q4 2025 Earnings Quarterly NOI Trend Chart

KRG Q4 2025 Earnings: Portfolio Highlights

The company operates 169 properties. They total 27 million square feet. Also, these are concentrated in Sun Belt markets. So 67% of annualized base rent comes from Sun Belt states. Portfolio composition is diverse. It includes neighborhood centers (39%). Plus, community centers (19%), power centers (14%), and mixed-use assets (27%). In fact, top tenants include TJX Companies (2.6%). Also, Ross Stores (1.9%) and PetSmart (1.6%) round out the top list.

Figure 2: KRG Q4 2025 Earnings Quarterly ABR per SF Growth

KRG Q4 2025 Earnings: 2026 Guidance

Management guides 2026 FFO in the range of $2.06 to $2.12. So the midpoint implies $2.09. This represents modest growth from 2025. Also, same-property NOI growth is expected in the range of 2.25%-3.25%. The midpoint is 2.75%. Plus, bad debt reserve is estimated at 1.0% of revenues. Interest expense is projected at $121.0 million net of interest income.

KRG Q4 2025 Earnings: Balance Sheet Strengths

Kite Realty maintains a fortress balance sheet. So this provides significant financial flexibility. Net debt to adjusted EBITDA stands at 4.9x, down from 5.1x. Also, available liquidity exceeds $1.0 billion. Plus, 84% of debt is fixed rate. The weighted average interest rate is 4.35%. In fact, the company has unencumbered NOI representing 89% of total NOI.

KRG Q4 2025 Earnings: Industry Trends

The retail REIT sector benefits from favorable supply-demand dynamics. So open-air retail continues to outperform enclosed malls. Also, grocery-anchored centers remain resilient and stable. Plus, Sun Belt population growth trends support KRG’s geographic positioning. Fixed rent bumps embedded in the portfolio support future growth. In fact, these embedded bumps average 156 basis points across the portfolio.

Summary

KRG Q4 2025 earnings validated the company’s model. So same-property NOI growth and higher rents signal momentum. Leasing metrics also remain solid. The company’s focus on high-growth Sun Belt markets positions it well. Also, management’s 2026 guidance reflects measured optimism. For investors seeking exposure to retail real estate, KRG offers great value. In fact, the combination of growth and financial stability is appealing.

Click Here to visit the AlphaStreet website.

The post KRG Q4 2025 Earnings Soar: Massive Momentum Stuns Market first appeared on AlphaStreet News.