No THAC0 Tuesday

By Michael Every of Rabobank

No TACO And No THAC0

The Global Daily yesterday noted lots of reasons to worry about this Gulf War 3 – today there are far more. However, as made clear since the start of this crisis, there is no way to say, “This is silly,” or to ‘go home’ and return to ‘normality’. Everyone in the war except the US *is* at home.

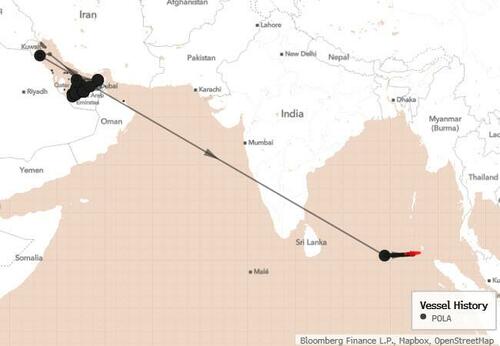

Israel is targeting Iran’s leaders and PM Netanyahu says the country is only “over halfway” to its war goals, with no timeline for ending the conflict. Key Gulf states are urging Trump to intensify the war, even as Trump may bill them for it. Iran’s parliament just passed a bill imposing tolls on Hormuz, seizing that key waterway, and is pressing Yemen’s Houthis to renew attacks on Red Sea shipping, which would massively exacerbate this crisis – Bloomberg warns of $140 oil if so; a disavowed report just said Egypt, who wants the war to end, warned the Houthis it would then attack them. The Iranian ambassador refused to leave Lebanon when ordered to by its government; and Iran just struck Israel’s oil refinery in Haifa, and a fully laden oil Kuwaiti oil tanker in Dubai. In short, the Middle East has its own agency.

The implications for the US in this war are also far beyond oil prices and the mid-terms: Trump’s ‘reverse perestroika’ and 21st century US hegemony may pivot on who wins. If the US wins, it de facto controls Middle East energy and can build a new architecture there. Yet financial press op-eds arguing for a ‘blueprint for Chinese global leadership’ could be right if the US loses – in which case everyone clinging to the flotsam and jetsam of the ‘rules-based order’ loses too.

Only if one starts with that strategic geopolitical imperative is Trump’s potential willingness to climb the escalatory ladder predictable, as is that there can’t be the ‘TACO’ markets want. That thinking underlines our geopolitical base case this war is largely over in 2-3 weeks, on favourable terms to the US – which is what Secretary of State Rubio just told the G7 too: but only after things get much worse first. If they get worse and stay there, so will the economic projections.

Notably, Trump has now warned the faction of the Iranian leadership he’s dealing with –reportedly led by parliamentary speaker Ghalibaf– that if it won’t strike a deal soon that includes reopening Hormuz, the US will destroy Iran’s electricity network and energy before leaving. Yet Trump is also reportedly telling aides that he’s willing to leave Hormuz in the hands of a smashed regime. Either outcome would leave Iran, the Middle East, and probably the global energy system in structural chaos. Meanwhile, thousands of US army paratroopers and marines are close to positions around Iran, offering the US other strategic options: but to what end? Tehran? A uranium hunt? It seems logical. A bridgehead in Hormuz via its smaller islands? Perhaps so. The obvious, but dangerous, target of Kharg island and its oil facilities?

A key complaint, after no TACO, is that the US isn’t clear in its objectives: in the last 24 hours we’ve seen conflicting messages from Bessent, Trump, and Rubio over what the US is trying to do re: Hormuz. Yet here one has to raise another geostrategic point: why does the US have to say exactly what it intends to do? Voters and traders want to know, but the ‘fog of war’ is a critical advantage and Trump is a past master at misdirection. Yes, perhaps there isn’t a US plan, and markets would be wise to price in that uncertainty; but nobody in power is going to tell a journalist or analyst what their war plans are, just what they *want* them to hear and then tell others. For any D&D players reading, there is no THAC0 in war. (But those decision-makers may front-run their actions in markets, so keep your eyes open for those loaded dice.)

In energy, Brent was down at $111 this morning in Asia despite the Kuwaiti oil tanker being hit, with WTI at $102 and 1-month TTF gas at €54.8, while jet fuel in Singapore is at a new high of $233.5, showing more pressure there. European and African oil markets are getting tighter as Asia buys more to fill its supply gaps. Expect that to continue ahead.

In related news, the IMF warned the UK faces one of the biggest energy shocks; Brussels says Europeans should consider traveling less to avoid energy shortages; and a report has it that EU member states’ national fuel price measures are threatening to worsen the energy crisis; China is looking to restart US energy imports as it sees its position in aluminium and EVs strengthened; and Australia’s PM has stated that fuel rationing will only kick in at an “extraordinary” supply hit, without specifying what that is.

Re: uncertainty, Gulf War 3 is exponentially accelerating the evolution/devolution of the global system which was already ongoing.

Spain has closed its airspace to the US military over the war, widening a rift with it. Rubio has just stated that after this is all over, NATO must be “re-examined” – and he’s the US good cop. Don’t think comfortable plans for accelerated European military spending by 2035 will hold up if the US were to make as radical a move vs NATO (and/or Greenland) as it did vs Iran once the Middle East dust has settled. That’s for an EU where, as Politico notes, ‘Europe’s crisis tourism: how the Iran war swallowed the EU’s geopolitical agenda.’

In the US, there is a rush to shift to new defence systems, so cheap drones are not fought with million-dollar missiles. That will entail a major military-industrial structural shake-up, with lessons learned from Ukraine, whose prowess Germany’s Rheinmetall CEO was recently mocking.

The USTR says he now sees only a limited role for the WTO after its recent meeting in Cameroon failed to see any reforms: Politico notes, ‘As the WTO flounders, the world’s middle powers go their own way.’ The US is also pressuring the EU to join its AI chips ‘club’, as the EU is pushing the US to join it in a common 50% steel tariff vs. China. Does the dust eventually settle with EU-US cooperation or separation – and if so at what cost to both?

Meanwhile, in Australia the RBA minutes’ key line was: “it was not possible to predict the future path for the cash rate target with any confidence, given the high degree of uncertainty around the breadth and duration of the current conflict in the Middle East.” It added that the direct effect of oil prices remaining around $100 would on its own lift headline CPI to around 5% in Q2, 0.75% higher than expected in February, and sustained higher oil prices would boost inflation more broadly over time. A majority agreed further tightening in policy would likely be required in the near term, but a minority was already worrying about the ‘stag’ part of stagflation.

The RBA is right about the Middle East – and let’s repeat that one then has to look at that complex region through a broad geopolitical lens, not a narrow “because markets/elections” one that said this war wasn’t going to happen. Oh – and that today saw half a million young Aussie workers get up to 42% pay increase due to changes to minimum wage rates.

Tyler Durden

Tue, 03/31/2026 – 09:55