Shocking, Record Explosion In Student Loan Delinquencies Marks The Start Of Next Debt Crisis

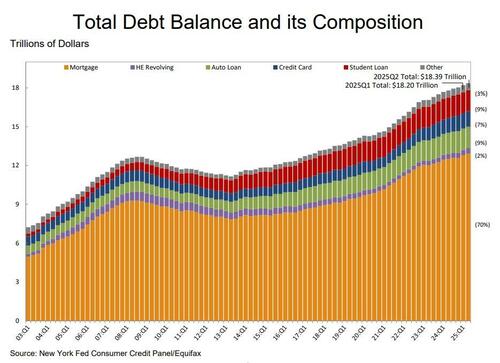

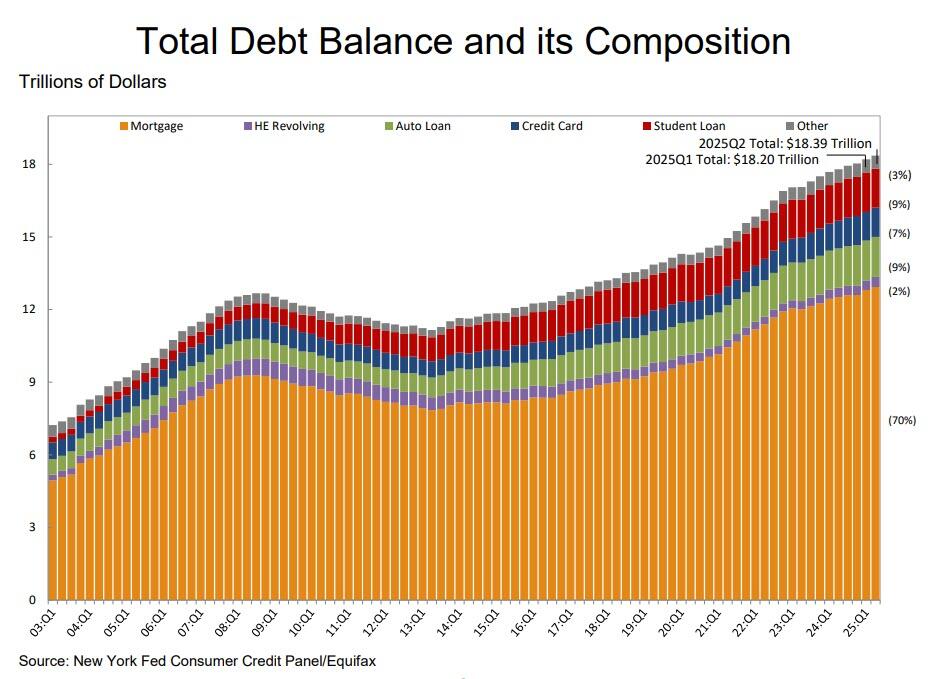

Total household debt rose by $185 billion in the second quarter of 2025, a 1% rise from Q1 2025. Balances now stand at $18.39 trillion and have increased by $4.24 trillion since the end of 2019, just before the pandemic recession.

Before is a snapshot of the latest Q2 data, courtesy of the NY Fed:

Balances

Mortgage balances grew by $131 billion during the second quarter of 2025 and totaled $12.94 trillion at the end of June.

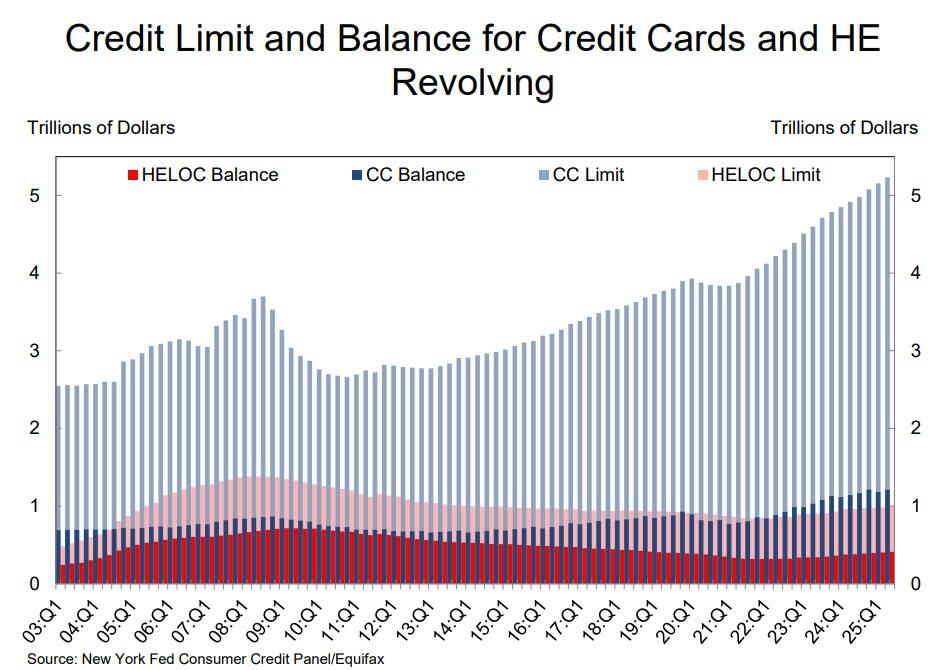

Balances on home equity lines of credit (HELOC) rose by $9 billion, the thirteenth consecutive quarterly increase. There is now $411 billion in outstanding HELOC balances, $94 billion above the low reached in the first quarter of 2022.

Credit card balances rose by $27 billion during the second quarter and now total $1.21 trillion outstanding and are 5.87% above the level a year ago.

Auto loan balances rose by $13 billion, and now stand at $1.66 trillion.

Other balances, which include retail cards and consumer finance loans, were roughly unchanged at $540 billion.

Student loan balances edged up by $7 billion and now stand at $1.64 trillion.

In total, non-housing balances increased by $45 billion, a 0.9% increase from 2025Q1.

{kind=link}

Originations

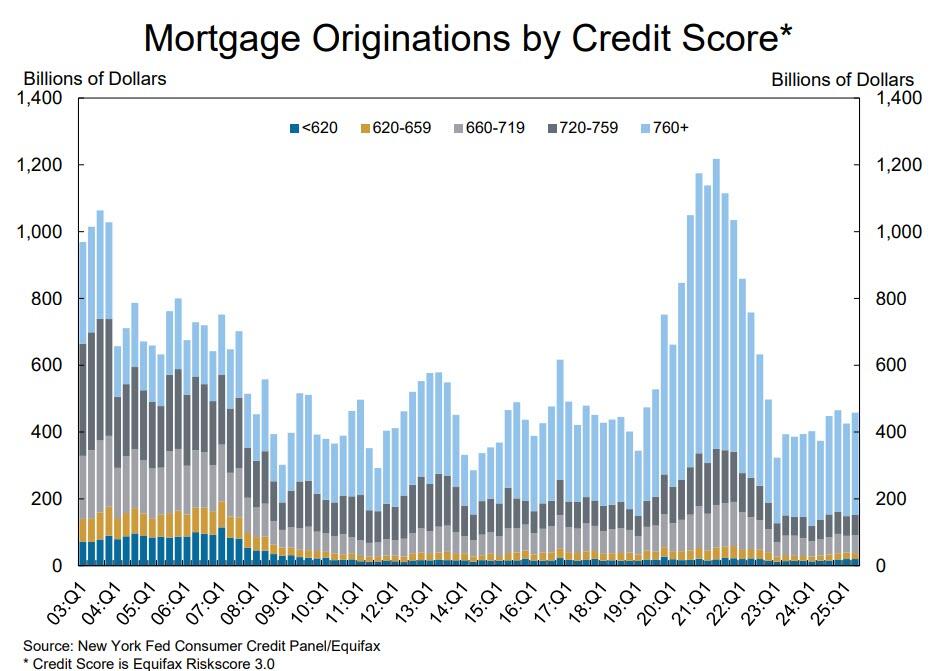

Mortgage originations increased slightly, with $458 billion newly originated in Q2.

There were $188 billion in new auto loans and leases during Q2, an increase from the $166 billion observed in the first quarter of 2025.

Aggregate limits on credit cards continued to rise, with a $78 billion (1.5%) uptick in the second quarter.

Home equity lines of credit (HELOC) limits rose by $18 billion, continuing the growth in HELOC limits that began in 2022

{kind=link}

Credit Quality

Credit quality of newly originated loans was mixed: The credit scores of newly originated auto loans decreased, as the median score for auto loan originations decreased by 6 points.

There was an improvement in the credit quality of mortgages, as the median score of newly originated mortgage loans increased by 5 points and the tenth percentile score increased by 13 points.

{kind=link}

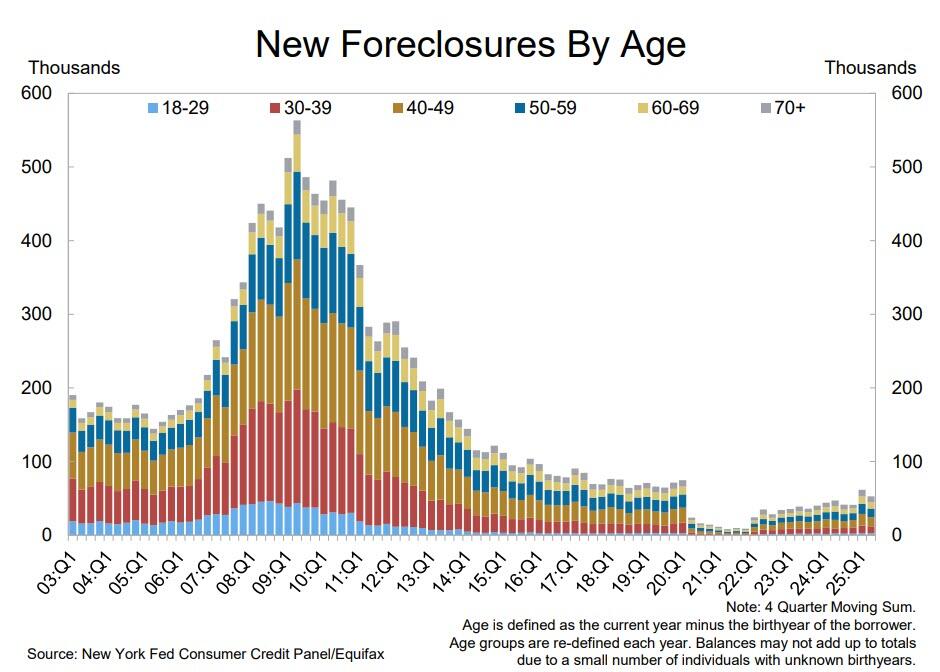

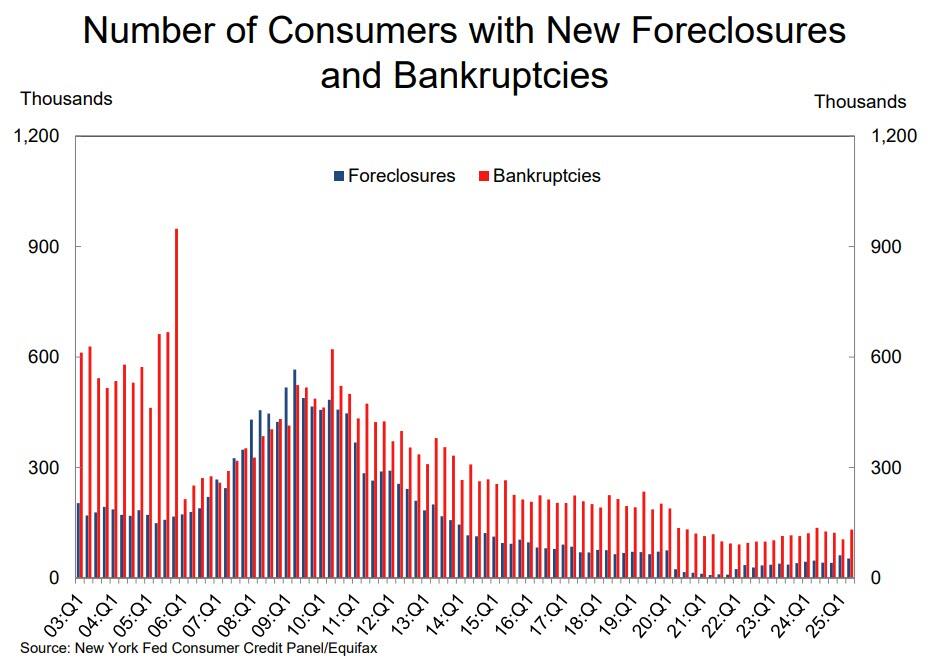

About 53,000 individuals had new foreclosure notations on their credit reports, a decline from the previous quarter

{kind=link}

All of the above is more or less as expected: yes, the US consumer is drowning in (ever more) debt, but that’s hardly a surprise: since life for middle class Americans is now largely unaffordable, most Americans have no choice but to take on even more debt.

There was, however, one big shock, and it had to do with the trillions in student debt in general, and the end of the repayment moratorium in particular (see “Trump Admin Begins Collecting On Student Loans In Default“).

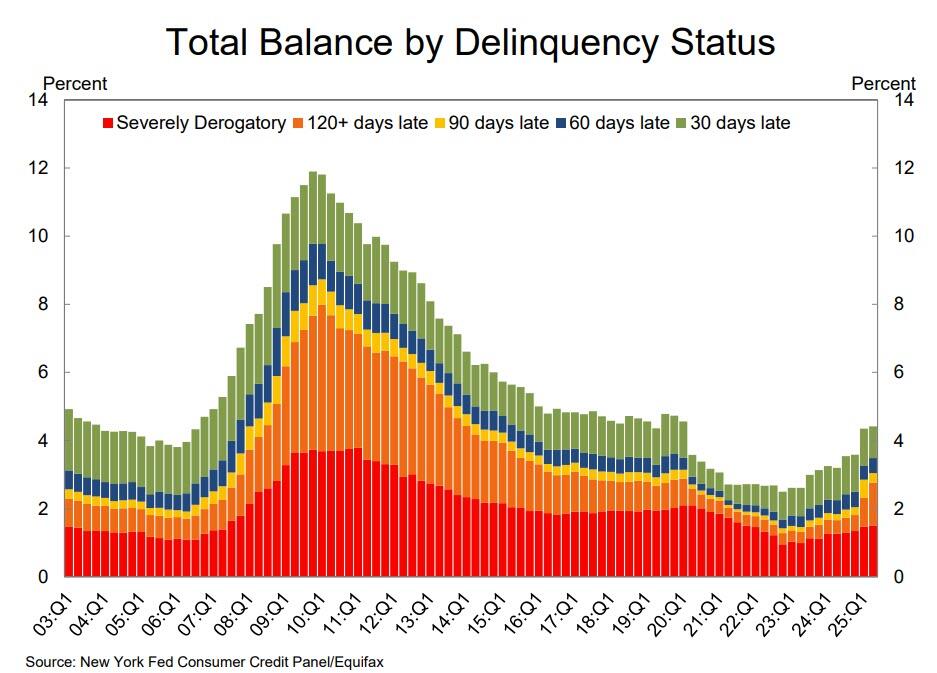

As the NY Fed notes, aggregate delinquency rates “remained elevated in the second quarter of 2025” which is putting it mildly. As of the end of June, 4.4% of outstanding debt was in some stage of delinquency, which is 0.1% higher than the first quarter.

{kind=link}

And while transition into early delinquency held steady for nearly all debt types; the exception was for student loans, which saw another uptick in the rate at which balances went from current to delinquent due to the resumption of reporting of delinquent student loans on credit reports after a nearly 5-year pause due to the pandemic.

Student loan delinquencies have been on the rise since the beginning of the year, after the government ended Biden’s years-long payment freeze.

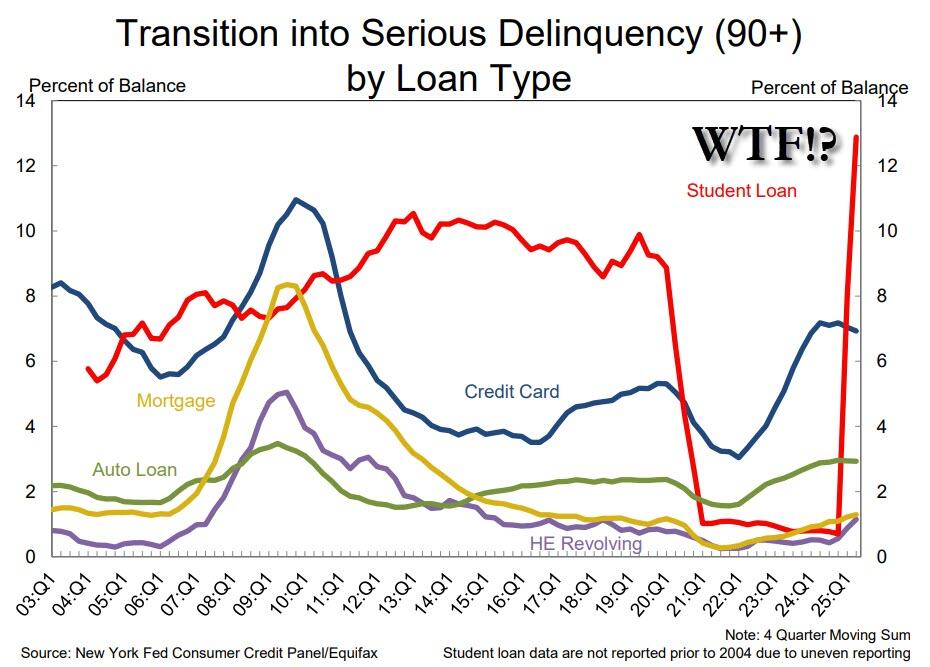

As the charts below show, transition rates into serious delinquency, defined as 90 or more days past due, were largely stable for auto loans and credit cards (although both were elevated compared to previous years), edged up slightly for mortgages and HELOCs … and absolutely exploded higher for student loans, as the share of student-loan debt entering serious delinquency was 12.9%, the highest in 21 years of data!

{kind=link}

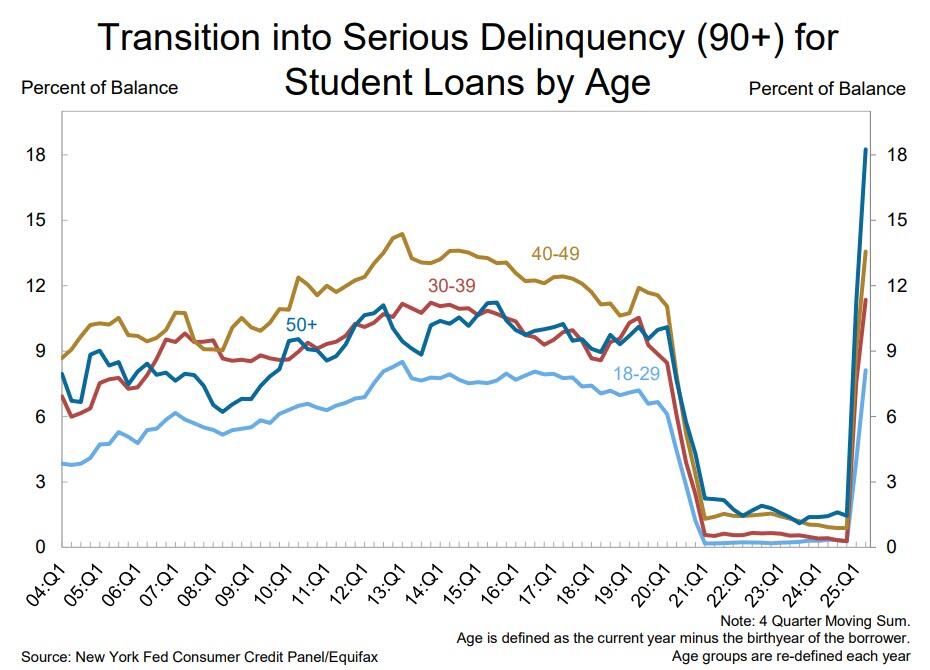

In fact, as one can clearly see there has never been such a catastrophic deterioration in student loan in US history across borrowers of virtually all ages, but especially those 50 and over!

{kind=link}

The record surge in delinquencies suggests American households, especially those with student loans, are facing increasing financial distress this year amid high interest rates and a slowdown in hiring. Recent data showed consumer spending fell in the first six months of 2025, even before tariffs started to boost prices.

While transitions into delinquency is the start of the bankruptcy pipeline, the end is also getting busier, and about 131.000 consumers had a bankruptcy notation added to their credit reports in Q2, an increase from the previous quarter. Expect this number to explode once all those student loan delinquencies transition to defaults in a few months at which point the student loan crisis becomes front and center.

{kind=link}

The dramatic deterioration will be another factor forcing the Fed to cut rates in September. Last week, Fed chair Jerome Powell said of delinquency rates, “Essentially, you have a consumer that’s in good shape and is spending,” though admittedly “not at a rapid rate.” Actually, turns out the consumer – when it comes to student loans – is now broker than ever.

In a briefing with reporters, New York Fed researchers said student-loan delinquencies would likely continue to rise, eventually returning to pre-pandemic levels. Between late 2012 and early 2020, the share of student debt that was seriously delinquent ranged between 10.7% and 11.8%.

“This quarter’s flow of household debt into serious delinquency was mixed across debt types, with credit card and auto loans holding steady, student loans continuing to rise and mortgages edging up slightly,” Joelle Scally, an economic policy adviser at the New York Fed, said in a press release, underplaying the clearly catastrophic surge in student loan delinquencies, and soon, defaults which will result in tens of millions of consumers suddenly finding themselves carved out from the US consumer economy just as the student loan crisis goes front and center.

Full New York Fed Household Credit slideshow can be found here.

Tyler Durden

Tue, 08/05/2025 – 17:20