US Futures, Global Markets Hit New Record Highs After US-EU Trade Deal

Another day, another all time high.

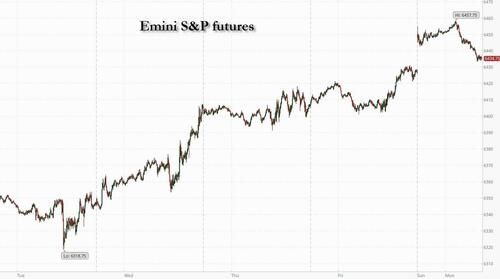

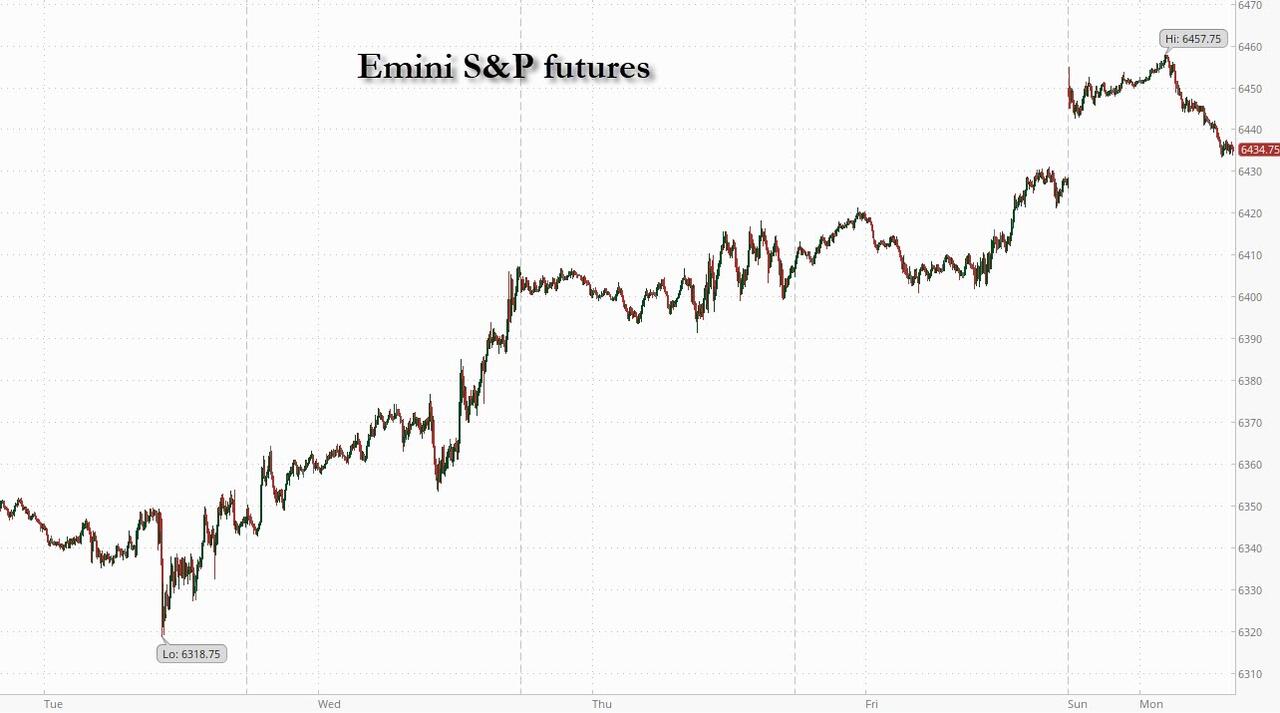

US equity futures and global markets are at a fresh all time high (but the gains are fading) on a trade-induced, global risk-on rally, sparked by Sunday’s US/EU deal for 15% tariffs on European exports to the US, while we also learned that US/China will extend the trade truce by 90-days as they resume negotiations today. As of 8:00am ET, S&P futures are up 0.2%, well off session highs, while Nasdaq futures gain 0.3%. Pre-market, all Mag7 names are higher with semis outperforming. Cyclicals are poised to outperform, led by Fins/Industrials. Bond yields are up 1bp, reversing an earlier drop, as the USD appreciates on the back of a slide in the euro and yen. Commodities are mixed with crude higher, natgas lower, precious metals flat, base metals down, and Ags mixed. Today’s macro data is light with on Dallas Fed Mfg Activity but it’s a crazy busy week with the Fed decision on deck, 38% of all companies reporting, the jobs report on Friday and much more (full preview coming).

{kind=link}

In premarket trading, Mag 7 names are all higher (Tesla +1.6%, Nvidia +0.7%, Amazon +0.6%, Meta +0.4%, Alphabet +0.4%, Microsoft +0.3%, Apple +0.2%).

US energy stocks moved higher after Trump said the EU agreed to buy $750 billion in American energy products and invest $600 billion in the US on top of existing expenditures. LNG stocks including Cheniere Energy (LNG) and Venture Global (VG) rise after the EU committed to big purchases of American energy products as part of the trade deal. Cheniere +5%, Venture Global +6%.

ASML’s US-listed shares (ASML) gain 3% after a key customer, Samsung, won a contract to make AI chips for Tesla.

ATAI Life Sciences (ATAI) sinks 11%. The company is a majority shareholder of Recognify Life Sciences, whose Phase 2b trial missed a primary endpoint.

Revvity (RVTY) falls 7% after the life sciences firm trimmed its adjusted earnings-per-share forecast for the full year.

Sarepta (SRPT) is down 2% as the FDA probes the death of an 8-year-old boy in Brazil who received the drugmaker’s Elevidys. Brazilian authorities have said that the death was unlikely to be due to the drug.

In the biggest news over the weekend, Trump and European Commission President Ursula von der Leyen announced the EU deal on Sunday at his golf club in Turnberry, Scotland, although they didn’t disclose the full details of the pact or release any written materials. And even as fears of a damaging trade war ease, optimism is tempered by the risks posed from the US jobs report, Fed and BOJ meetings and earnings from megacap companies this week. Early gains in European automakers faded and the euro slid to its lowest in a week against the dollar as investors digested more negative aspects of the accord.

US energy stocks moved higher after Trump said the EU agreed to buy $750 billion in American energy products and invest $600 billion in the US on top of existing expenditures.

“This deal removes any uncertainty which has been reflected in the positive market movements this morning,” Michael Browne, global investment strategist at Franklin Templeton Institute, wrote in a note. “We will now have to see what the tariffs mean for businesses and how they will be absorbed, but it will vary by sectors.”

Elsewhere, Treasury Secretary Scott Bessent and Chinese Vice Premier He Lifeng are scheduled to meet in Stockholm on Monday amid a report their two countries are expected to extend their tariff truce by another three months. “Markets like certainty and we should expect a deal very soon,” according to Franklin Templeton Institute’s Browne.

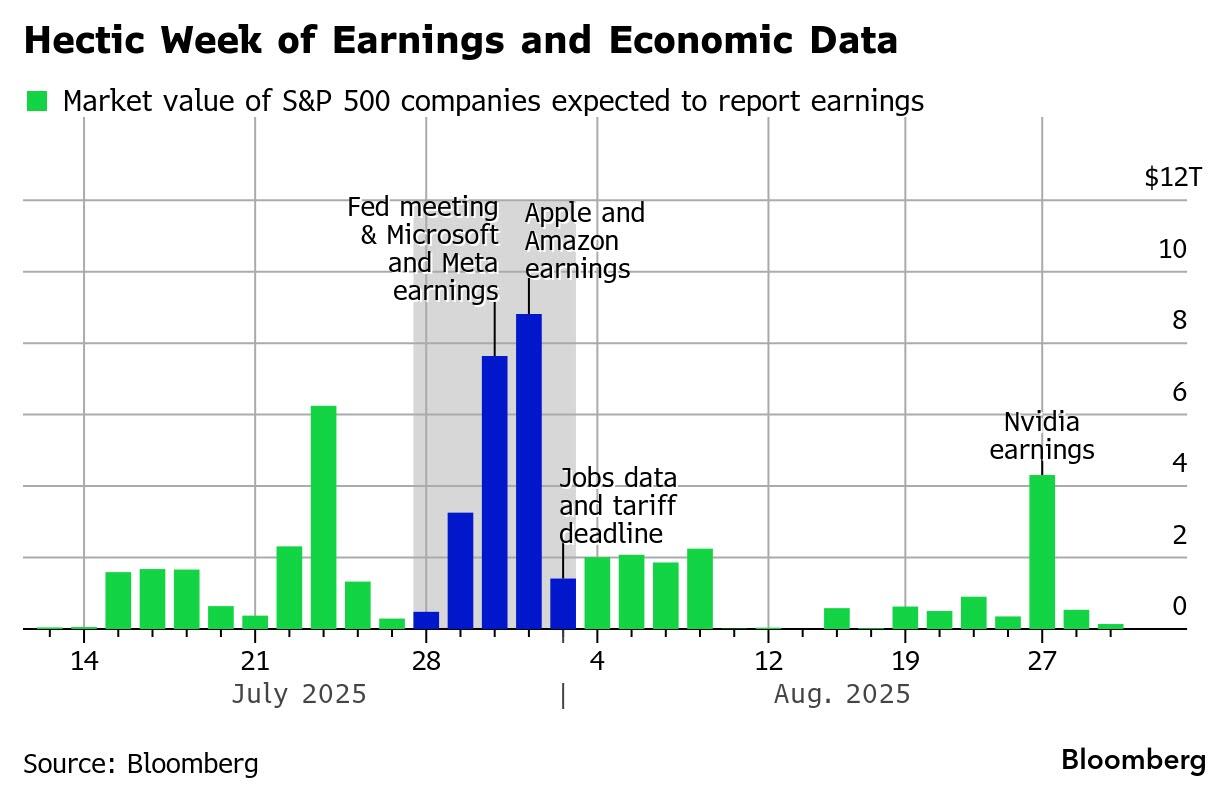

Meanwhile, Mag 7 members Apple, Amazon.com, Microsoft and Meta are all due to report numbers. Robust corporate earnings have bolstered investor confidence in US stocks, as companies head for their highest share of beats since the second quarter of 2021.

{kind=link}

Progress in trade deals, positive economic data and corporate resilience have offset worries that stocks are overheating. More than 80% of S&P 500 companies have exceeded profit estimates, according to data compiled by Bloomberg Intelligence.

Later in the week, the Bank of Japan is set to keep interest rates unchanged with traders on alert for any signs of future guidance by the central bank.

In geopolitical news, leaders of Thailand and Cambodia are set for talks Monday to halt the deadliest clashes between the neighbors in more than a decade.

European stocks and US futures both advance after the European Union secured a trade deal with President Donald Trump over the weekend, further easing fears of a damaging trade war ahead of the Aug. 1 deadline. The Stoxx 600 climbs 0.6% with technology, real estate and health care names leading gains. Automotive stocks jumped in early trading but later slipped as investors focused on more negative aspects of the deal. European chipmakers rise after Samsung won a contract to build AI chips for Tesla. Here are the biggest movers Monday:

ASML and other European semiconductor equipment stocks gain after their key customer, Samsung, wins a contract to make AI chips for Tesla, while a US-EU trade agreement that exempts tariffs on semiconductor equipment gives a further boost

Forvia shares rise as much as 12%, to their highest intraday level in over a year. The firm delivered operating profit ahead of analyst expectations in the first half and confirmed its guidance for the full year

Ceres Power Holdings soars as much as 34%, the most since 2024, after Doosan became the first of its strategic licensing partners to start mass-market production of fuel cell stacks using the company’s solid oxide technology

ProSieben shares surge 11% to €7.79 apiece after MFE decided to raise its takeover bid for the German broadcaster, with the Italian firm now offering €4.48 in cash and 1.3 of its Class A shares for one share in ProSieben

Landis+Gyr gains as much as 5.2%, reaching its highest since late October, following an upgrade to buy at Berenberg, which sees a potential divestment of the Swiss energy management firm’s EMEA business as a key catalyst

European pharma stocks advance after senior American officials told reporters the US has agreed to set a 15% tariff on pharmaceutical imports from the EU as part of the broader trade deal struck at the weekend

European car shares erase earlier EU-US trade-deal inspired gains as analysts point out more negative aspects of the accord and after Audi cut its outlook. Audi says the tariffs and restructuring costs are weighing on earnings

Shares in European defense companies fall, missing out on a broader rally inspired by a EU-US trade deal, under which Europe is set to buy military equipment from the US

Heineken shares drop as much as 2% after volumes fell more than anticipated due to retailer disputes across Europe, although analysts at Citi said these have been resolved as they pointed to better exit rates in June

Loomis shares fall as much as 7.1% after SEB cut its rating on the Swedish cash handling and security firm to hold from buy, saying stock now offers more neutral risk/reward due to lower volumes in France and Sweden

Computacenter shares drop as much as 6.4%, with analysts saying the IT company’s first-half adjusted operating profit is disappointing as consensus had forecast a larger rise in earnings

SP Group falls as much as 6.1% after DNB Carnegie cut its price target on the Danish plastics industry group, saying that the firm is unlikely to recover its lost first-half sales volumes in the rest of the year

PGE shares drop as much as 3.6% after Poland’s biggest power utility reported 11.b zloty write-offs in the first half of the year, mostly in its conventional electricity generation segment

Earlier in the session, Asian equities declined as investors assessed a US trade deal with the European Union and considered the potential for negotiations with other nations, including China. The MSCI Asia Pacific Index dropped 0.3%, with Advantest weighing on the gauge after a UBS downgrade. Japanese and Indian shares were among the biggest decliners in the region. Samsung rose after it signed a $16.5 billion pact to make chips for Tesla. Shares in Hong Kong, China, Indonesia and Taiwan advanced. The MSCI Asian benchmark climbed last week to the highest since March 2021, as US deals with Japan and other nations buoyed optimism ahead of President Donal Trump’s Aug. 1 tariff deadline.

“The rally since ‘Liberation Day’ is due to a change in sentiment and expectations, rather than a change in fundamentals,” Chi Lo, senior market strategist, APAC at BNP Paribas Asset Management, said in a Bloomberg TV interview. “If we get a shock, such as China-US trade talks not going as expected, that could be a trigger for a pullback,” he added.

In FX, the dollar strengthens for a third straight session with the Bloomberg Dollar Spot Index up 0.4%. The antipodean currencies are leading losses against the greenback among the G-10 currencies, falling around 0.7% each. The euro is not far behind with a 0.6% drop having erased an earlier gain. The pound has been the most resilient, albeit still losing 0.2%.

In rates, treasuries are little changed in early US trading, off day’s best levels reached during London morning following weekend announcement of a US-EU trade accord. Yields are back within 1bp of Friday’s closing levels after declining by 2bp-3bp; dominant themes last week included progress toward trade agreements averting steeper US tariffs on imports, and US administration pressure on Fed Chair Jerome Powell to step down before his term ends next year. 10Y Treasurys are trading at 4.40%, up 1bp from Friday’s close, erasing an earlier drop. An accelerated and compressed coupon auction cycle begins with $69b 2-year note sale at 11:30am and $70b 5-year at 1pm; it concludes Tuesday with $44 billion 7-year, the last coupon auction of the May-July financing quarter. Quarterly refunding announcement for August-to-October is ahead Wednesday.

In commodities, spot gold is steady near $3,338/oz. WTI rises 0.6% to near $65.60 a barrel. Bitcoin is hovering just below $119,000.

Looking at today’s US economic data calendar, we only have July’s Dallas Fed manufacturing activity (10:30am); key employment indicators are ahead this week including JOLTS job openings, ADP employment change and employment report. Fed officials are in external communications blackout ahead of their July 30 rate decision; swap contracts linked to future Fed rate decisions continue to fully price in one quarter-point rate cut this year in October, and most of a second one by year-end.

Market Snapshot

S&P 500 mini +0.3%

Nasdaq 100 mini +0.5%

Russell 2000 mini +0.5%

Stoxx Europe 600 +0.5%

DAX +0.2%, CAC 40 +0.5%

10-year Treasury yield -2 basis points at 4.37%

VIX +0.3 points at 15.2

Bloomberg Dollar Index +0.4% at 1202.83

euro -0.5% at $1.168

WTI crude +0.8% at $65.71/barrel

Top Overnight News

Futures climbed (SPX futs +15 bps, NDX futs +30bps) after the US and the EU reached a trade agreement that set a lower-than-threatened 15% tariff on most goods, including cars, from Aug. 1. Germany and France weren’t willing to risk a trade war with the US, pushing the EU to conclude the deal. BBG

The US has frozen restrictions on technology exports to China to avoid hurting trade talks with Beijing and help Trump secure a meeting with Xi Jinping this year. The commerce department’s Bureau of Industry and Security, which runs export controls, has been told in recent months to avoid tough moves on China, according to current and former US officials. FT

U.S. President Donald Trump said on Sunday his administration was close to reaching a trade deal with China, but gave no other details. “We’re very close to a deal with China. We really sort of made a deal with China, but we’ll see how that goes,” Trump said. RTRS

China will begin providing subsidies of ~$500 per child under the age of 3 to parents across the nation as it looks to boost birthrates. BBG

Months of intense negotiations appear unlikely to produce a trade deal between the US and India before the August 1 deadline, despite Trump having teased one for months as “coming soon”, according to three people familiar with the situation. SCMP

Israel rolled back curbs on food distribution to Gaza in an effort to defuse an international outcry. Meanwhile, Houthi militants vowed to target ships dealing with Israeli ports. BBG

Tesla tapped Samsung to produce its next-gen chips in a $16.5 billion deal running through 2033. Elon Musk later said on X that “$16.5B is just the bare minimum.” Samsung shares jumped to their highest since September, while Tesla rose in premarket trading. BBG

Investors pulled $3.9 billion from Treasuries in June and added $10 billion to US and European IG company debt amid rising US fiscal deficits, EPFR data show. BBG

NASA spokesperson said about 20% of the workforce is set to depart the agency as part of an overall effort to become streamlined and more efficient amid concerns about mission safety.

Boeing is bracing for a strike at its defense hub after workers rejected a contract offer that included a 20% wage increase over four years. IAM District 837 members in St. Louis voted to reject the Boeing (BA) defence contract, while the Co. said it was disappointed that employees voted down the richest contract offer it’s ever presented to IAM 837 and stated that no talks are scheduled with the union.

US Lawmakers said to be quickly souring on the OBBB’s tax hike on gamblers, according to Punchbowl

Trade/Tariffs: US-EU Deal

US President Trump announced a deal with the EU involving a 15% tariff and stated the EU will buy USD 750bln in US energy and is opening up all countries, while he added the EU will purchase US military equipment and will make USD 600bln in US investments. Trump added that the deal is the biggest ever made and will be great for cars, as well as noted that agriculture is also to have a big impact. Furthermore, Trump said they are looking at deals with three to four other countries and countries will probably receive a letter of clarification or confirmation this week.

European Commission President von der Leyen confirmed there will be 15% tariffs across the board and said the trade deal creates certainty and stability for businesses on both sides of the Atlantic. Von der Leyen said the deal reaffirms the transatlantic partnership and the 15% tariff rate is for a vast majority of EU exports including cars, semiconductors and pharmaceuticals, while she added that they agreed on zero-for-zero tariffs on certain agricultural products and on strategic products such as aircraft component parts and certain chemicals. Furthermore, she commented that tariffs will be cut and a quota system in place for steel, while there will be major purchases of US LNG and details on the trade deal framework will happen over the next few weeks.

US senior administration official said the EU agreed to open markets to all but a few products, while President Trump suggested the EU buy USD 1tln of US energy during his term, but the EU settled at USD 750bln and agreed to 15% tariffs on autos, semiconductors and pharmaceuticals. The admin official stated that EU leaders accepted that US would stick to 50% tariffs on steel and aluminium and the EU wants to continue discussing steel and aluminium tariffs. The official stated that President Trump has the ability to change tariffs back if countries don’t live up to their commitments and the EU lowered tariffs on many products in the agriculture sector, but not all. Furthermore, the aircraft investigation is still in progress in which the tariff will be zero for now and it is likely that aircraft won’t face tariffs, but must wait for the probe to end, while the spirits issue is still to be decided and the US did not include it due to large EU agricultural surpluses.

USTR Greer and Commerce Secretary Lutnick travelled to Scotland for the EU trade talks, while Lutnick stated the US will release the results of the Section 232 regarding chip imports in two weeks and separately commented that there are no more extensions to the August 1st deadline for tariffs.

German Chancellor Merz said it is good that the EU and US reached a deal on tariffs and the deal avoids a conflict that would have hit the German economy, particularly in the autos sector, while Merz added that they protected their core interests even if he would have liked to see further facilitation of transatlantic trade.

French European affairs minister said the trade deal between the EU Commission and the US will bring temporary stability, but it’s still an unbalanced deal, while the minister added that the deal has merits of exempting certain key French sectors such as aeronautics, spirits and medicines.

Dutch PM Schoof said the EU-US agreement is vital for an open economy like theirs, while he added that it is important to work out the details of the framework trade deal as quickly as possible.

French trade minister on the EU-US framework trade deal, says more talks are needed concerning digital services; spirits should be exempted.

“EU officials expect there to be a joint statement with the US on yesterday’s deal – not-legally binding, working to have it ASAP. “, according to SCMP’s Bermingham “This is expected to be along the lines of the US-Indonesia statement from roughly a week ago.”

EU Official says the EU has agreed to cut its car import duty to 2.50% as part of EU-US trade deal. EU official, on US/EU trade deal, says discussions ongoing regarding wines and spirits.

Germany’s engineering federation VDMA says US and EU must not make trade agreement a new normal; trade deal will cost German auto firms billions every year.

German Chemicals Association VCI, on EU-US trade deal, says, has taken note of “certain chemicals” but do not know which are meant by this.

German Economy Minister says there will be a requirement for some sectoral adaptation after the EU-US deal Need for further negotiations on aluminium and steel.

Trade/Tariffs: US-China

US President Trump is said to freeze export controls in order to secure a trade deal with China, according to FT. It was separately reported that US and China are expected to extend the trade truce by 90 days, according to SCMP.

South Korea’s Finance Minister and Foreign Minister will meet with US counterparts this week, while South Korea is preparing a trade package and is drawing a mutually agreeable plan including a shipbuilding partnership. It was separately reported that South Korea suggested tens of billions of dollars worth of shipbuilding projects to the US in trade talks, according to Yonhap.

UK government said PM Starmer is to meet US President Trump for wide-ranging talks in Scotland and they are expected to discuss progress on implementing the UK-US trade deal, hopes for a ceasefire in the Middle East, and applying pressure on Russia’s Putin to end the war in Ukraine.

Chinese Foreign Minister held a phone call with South Korean counterpart, says the two sides should jointly oppose “decoupling”.

A high-level delegation of US executives will travel to China this week to meet Chinese officials, in a visit organised by the US-China Business Council, according to Reuters sources; US government was not involved in organisation of visit.

US-China trade talks to start Monday “afternoon” local time in Sweden, according to Reuters sources.

A more detailed look at global markets courtesy of Newsquawk

European bourses (STOXX 600 +0.7%) opened entirely in the green, benefiting from the EU-US trade agreement. As the morning progressed, indices waned off best levels, but still remain in the green. Nothing behind the slight pressure, but likely some profit-taking ahead of this week’s key risk events, which include US PCE, NFP and a slew of earnings. European sectors hold a strong positive bias. Healthcare has been buoyed by the EU-US trade deal, where the EU secured a 15% rate for a vast majority of EU exports including cars, semiconductors and pharmaceuticals. Autos were initially strengthened by the announcement, but now trade mixed as traders digest the financial implications of the tariff – Germany’s VDMA said that the “trade deal will cost German auto firms billions every year”. Media is found at the foot of the pile, joined by Basic Resources.

Top European News

ECB’s Cipollone said the economy is sending conflicting signals and needs to see how trade will affect prices.

Germany is reportedly to avoid EU punishment for breaching budget rules, according to FT,

Several were killed in a train crash in Germany near the town of Biberach, close to the border with France.

S&P affirmed Luxembourg at AAA; Outlook Stable, while Fitch lowered Finland’s sovereign rating from AA+ to AA; Outlook Revised to Negative from Stable.

ECB’s Kazimir says “I do not see any significant change that would force my hand to act in September; it would take something like clear signs of unravelling the labour market for me to act” “Sees no looming spectre of inflation undershoot and risks are not tilted to the downside”. US-EU trade deal reduces uncertainty but unclear how it impact inflation.

APAC stocks were ultimately mixed despite early tailwinds following the announcement of the US-EU trade deal, while gains were capped ahead of a slew of risk events this week and with Japan pressured amid political uncertainty. ASX 200 traded higher but with upside limited amid light catalysts and ongoing global trade uncertainty, while participants digested quarterly activity updates. Nikkei 225 wiped out its opening gains and dipped into negative territory amid political headwinds with Japan’s ruling LDP said to have collected enough signatures on Friday to call a general meeting that will hold PM Ishiba accountable for the party’s recent crushing election loss, while participants also brace for the BoJ policy meeting this week where analysts reportedly see the BoJ providing a less gloomy view and signalling the potential for resuming rate hikes later in the year. Hang Seng and Shanghai Comp were mixed ahead of US-China trade talks in Sweden and with the trade truce expected to be extended for 90 days.

Top Asian News

PBoC conducted CNY 400bln 1-year Medium Term Lending Facility with the rate at 2.00% for a CNY 100bln net injection.

Chinese Premier Li said at the World AI Conference that China will help establish an international AI collaboration group and that AI should be an international public good that benefits humanity, while he stated global AI development is accelerating and AI is moving from perceiving the world to changing the world.

China’s Agriculture Ministry announced a plan to promote the consumption of agricultural products.

Beijing issued a warning of geological disasters such as landslides for 10 of its 16 districts.

US Commerce Secretary Lutnick said President Trump really likes TikTok, but it has to move to US ownership.

Many called for Japanese PM Ishiba’s resignation at Japan LDP meeting, according to Kyodo.

FX

The USD picked up strength in early European trade after a steady APAC session. There was no headline coinciding with the move at the time but appeared to be more a case of Europe reacting to the EU-US trade agreement. The EU-US agreement removes another area of uncertainty for the market and could also be followed by some positive mood music between the US and China with both sides set to meet in Stockholm this afternoon. Reporting ahead of the meeting suggests a potential 90-day extension of the current 90-day truce. DXY has made its way back onto a 98 handle with a current session high at 98.06. Next upside target comes via the 50DMA at 98.30.

The obvious focus for the Eurozone at the start of the week has been on the trade front following the EU-US trade agreement. The deal will see EU goods subject to a 15% tariff (including autos, semiconductors, pharma), 0% tariff on aircraft parts (for now), make USD 750bln in energy purchases from the US and USD 600bln in US investments. The deal is broadly as expected given the reporting last week and is not “as bad as feared” given the 30% tariff rate, which was looming over negotiations. However, EUR has been unable to capitalise on the removal of uncertainty and is softer vs. the USD and EUR. Part of this may be a “buy the rumour, sell the fact” trade and also the view that, whilst the worst case has been avoided, it is still a sub-optimal trade arrangement for the EU. It is also worth noting that at this stage, it is just an agreement and still subject to formal ratification by both sides.

JPY is also suffering at the hands of the firmer USD with USD/JPY back above the 148 mark. Sentiment in Japan remains suppressed by political headwinds with Japan’s ruling LDP said to have collected enough signatures on Friday to call a general meeting that will hold PM Ishiba accountable for the party’s recent crushing election loss. Participants are also bracing for this week’s BoJ policy announcement, which is expected to see policy settings left unchanged. As it stands, markets price around 19bps of tightening by year-end. USD/JPY has ventured as high as 148.34 with the next upside target coming via the 21st July high at 148.66.

GBP is softer vs. the USD but to a lesser extent than peers with the pound benefiting from cross-related selling in EUR/GBP. Macro drivers for the UK are light aside from UK PM Starmer being set to meet US President Trump for wide-ranging talks in Scotland; expected to discuss progress on implementing the UK-US trade deal. The data slate is a light one for the UK this week. Cable is just about holding above the 1.34 mark with a session low at 1.3407. EUR/GBP is eyeing a test of 0.87 to the downside with a current session low at 0.8705.

Antipodeans are the G10 underperformers, after initially being buoyed by the risk tone. Though as sentiment slowly waned across markets, the Aussie and Kiwi also lost their allure, to currently trade just off session lows.

Fixed Income

USTs/Bunds began lower, in-fitting with the positive risk tone, held in the red but off lows in contained overnight trade. JGB’s on the other hand were bid alongside a deterioration in risk sentiment in Japan amid political headwinds and ahead of the BoJ announcement later in the week.

As for the European morning, the fixed income complex caught a bid around the European cash open. No clear fresh catalyst for the upside, but potentially in tandem with a slight deterioration in the risk tone and a paring of the hawkishness seen late last week, with the EU-US deal welcome but still a growth headwind vs the revised April baseline of 10%. USTs are currently trading flat/incrementally firmer, and towards the upper end of a 110-26 to 111-03 range. No Tier 1 data releases today, so more focus on the US-China meeting in Sweden, US supply (2yr & 5yr note due) and then Treasury Financing Estimates thereafter before Wednesday’s refunding. Morgan Stanley does not expect the Treasury to increase coupon sizes at all this year, and have pushed out their call for the next coupon increase to February 2027 (prev. May 2026).

For Bunds, they caught a bid around the European cash open and have continued to climb, currently at session highs in a 129.12-74 range. Further upside could see a potential test of its 50% fib retracement of last week’s move at 129.80, and then the round 130.00 mark. On the firmer fixed environment and associated lower yield action, Rabobank makes the point that diminished trade uncertainty is potentially causing a moderation in term premia.

Gilts are also higher to a similar degree as Bunds, and ultimately following peers. UK paper currently trades towards the upper end of a 91.57-85 range. More focus has been on the EU, but reports recently have suggested that UK PM Starmer is to convene with US President Trump at his Turnberry golf resort in Scotland. Starmer is reportedly to bring up steel tariffs with Trump, but the US President said on Sunday that the trade deal with Britian is “concluded”.

Commodities

WTI and Brent are modestly higher in what has been a choppy session so far, currently higher by around USD 0.50/bbl. Earlier upside was driven by the broader risk tone, but as that deteriorated a touch (in equities), the complex also waned off best levels. Nothing energy-specific of note for the complex today, so attention now turns to developments in Sweden, where US-China are to discuss trade. For energy specifically, the OPEC+ JMMC are set to convene, but are unlikely to make any alterations to the group’s output plans. Brent Oct’25 currently trades in a USD 68.35-69.11/bbl range.

Spot gold initially gapped lower at the open, as the yellow-metal digested the latest EU-US trade deal, which boosted sentiment. However, overnight trade saw the prices entirely pare that downside, to currently trade around the unchanged mark.

Base metals are mixed/marginally firmer, failing to benefit from the on the early trade-related euphoria heading to a slew of risk events this week. 3M LME copper currently incrementally higher and trades in a USD 9,779.05-9,820.4/t range.

Iran’s Foreign Ministry spokesman says IAEA visit is to take place within two weeks.

Geopolitics: Middle East

Israel’s military announced a pause of military activity in designated areas in Gaza where it is not operating until further notice, with the pause in fighting to be daily in three areas of Gaza.

Two Jordanian air force planes and one Emirati plane dropped a total of 25 tonnes of aid in Gaza in the first air drop in months, according to a Jordanian official source. Furthermore, the World Food Programme said it hopes Israeli humanitarian pauses will allow for a surge in urgently needed food for Gaza and it has enough food in or on its way to the region to feed the entire Gaza population for almost three months.

US President Trump said he doesn’t know what is going to happen regarding Gaza and Israel is going to have to make a decision, while he added we will see what happens and the US is going to do more aid.

Hamas’s exiled chief Khalil al-Hayya said ceasefire negotiations with Israel are meaningless under a continued blockade and starvation, while he added the immediate and dignified delivery of food and medicine to our people is the only serious and genuine indication of whether continuing the negotiations is worthwhile.

Yemen’s Houthis said they will target ships that belong to companies which deal with Israeli ports, regardless of their nationality and ships will be attacked regardless of their destination if shipping companies don’t heed their call.

Houthis say that, as part of the “4th phase” of action, they will be targeting “any ship coming from Israeli ports, regardless of nationality.”, via journalist Berman.

Geopolitics: Russia-Ukraine

Kremlin spokesperson said Russia prefers political and diplomatic means to resolve the conflict in Ukraine, although Kyiv and the West rejected that path.

Poland scrambled aircraft to ensure airspace security after Russia launched a missile attack on Ukraine, according to the Polish armed forces.

European Commission President von der Leyen said following a conversation with Ukrainian President Zelensky that the EU will continue to support Ukraine on its European path.

An Emergency Alert has been declared this morning throughout the Lithuanian capital of Vilnius, after an unknown drone, believed to likely be Russian, crossed into the country from Belarus, according to OSINTdefender.

Geopolitics: Other

Thailand’s military noted clashes continue in several areas on the border with Cambodia, while it was separately reported that Thailand’s acting PM agreed in principle to have a ceasefire but wants to see a sincere intention from Cambodia and wants bilateral dialogue as soon as possible.

Malaysia’s Foreign Minister said that Cambodia’s PM and Thailand’s acting PM will visit Malaysia on Monday to discuss the conflict, while a Thai Foreign Ministry spokesperson confirmed there will be a meeting on Monday.

US President Trump spoke with the leaders of Cambodia and Thailand, while he stated that both are looking for an immediate ceasefire and peace, as well as stated that they are looking to get back to the trading table with the US.

US Secretary of State Rubio spoke with the leaders of Cambodia and Thailand and urged both sides to deescalate tensions immediately and agree to a ceasefire, while he said the US is prepared to facilitate talks.

North Korea said it has no interest in any new policy of South Korea and will not sit down for dialogue, while it rejects conciliatory overtures by South Korea and said North Korea and South Korea have moved irreversibly past the concept of one nation.

South Korea Presidential Office said it is to continue to take actions needed for peace after North Korea’s rejection of peace overtures, while the South Korea Unification Ministry said North Korea’s reaction is an indication of the challenge in inter-Korea ties.

US Event Calendar

10:30 am: Jul Dallas Fed Manf. Activity, est. -9.5, prior -12.7

DB’s Jim Reid concludes the overnight wrap

This week’s key August 1st trade deadline is rapidly becoming a non-event. The last of the significant agreements was concluded yesterday, with the US and EU reaching a deal that mirrors the structure of the recent US-Japan accord. European stock futures are up around a percent in Asia as a result. The agreement includes a 15% tariff on autos, excludes pharmaceuticals, and maintains the existing 50% tariffs on steel and aluminium. In a significant gesture, the EU has pledged to import $750 billion worth of energy, invest $600 billion into the US economy, and purchase “vast quantities” of military equipment. Additionally, the EU has committed to opening its markets to US goods at zero tariffs. On pharma there was some confusion as to whether the EU will be exempt from the upcoming Section 232 investigation on the sector. For now, there is mixed commentary on this from both sides.

Meanwhile, US-China negotiations are underway in Stockholm today and tomorrow. Although their bespoke August 12th deadline looms, early reports — so far only from Chinese press headlines — suggest a 90-day extension has been granted. This development, if confirmed, would further reduce the urgency surrounding this week’s trade calendar. So expect the White House stationery cupboard to take a hit this week, with a flurry of letters flying out— but in the context of most of the big trade understandings having already been agreed.

Adding a curveball to the week though, Thursday (July 31st) will see the Federal Appeals Court hear the International Trade Court’s ruling that President Trump’s use of an emergency declaration to impose tariffs was unlawful. Frankly, it’s hard to gauge the outcome or the potential impact if the policy is indeed struck down—so this is one to watch. It feels like the agreements made with other countries would likely stand even if the court ruling continues to go against Mr Trump. For others he will pivot to different methods of imposing tariffs. So perhaps no major impact now, but we will see.

Turning to central banks, the Federal Reserve meets on Wednesday. The key question is whether enough uncertainty has lifted for the Fed to signal a clearer policy direction for September. Our US economists preview the meeting here and expect the Fed to hold rates steady for a fifth consecutive meeting, maintaining its current guidance without offering new clues about September. Notably, they anticipate two governors will dissent—something that hasn’t happened since 1993—at a time when political pressure on Chair Powell is intensifying. Also meeting this week are the Bank of Canada (Wednesday) and the Bank of Japan (Thursday), both expected to keep rates unchanged.

The Fed isn’t the only focus in the US this week. It’s a packed schedule for data and earnings, culminating in Friday’s payrolls report. Deutsche Bank forecasts a headline gain of just +75k (vs consensus +109k and last month’s +147k), and +100k for private payrolls (matching consensus and up from +74k last month). The difference reflects a reversal in strong state and local hiring seen in the previous month. Both DB and consensus expect the unemployment rate to tick up to 4.2%. Importantly, our economists believe that with lower immigration, even payrolls in the 50–100k range could still tighten the labour market. Other labour indicators this week include the JOLTS report tomorrow and ADP data on Wednesday.

Also on Wednesday, Q2 US GDP is expected to show a +2.1% print, rebounding from -0.5% in Q1. Thursday brings the crucial June core PCE data, alongside personal income and consumption figures. Rounding out the US data highlights, we’ll see the Conference Board’s consumer confidence index for July tomorrow (DB forecast 96.1 vs 93.0 in June), the Q2 employment cost index, and the ISM manufacturing gauge for July on Friday (DB forecast 49.5 vs 49.0 in June).

In other US news, the Treasury refunding announcement is due Wednesday, following today’s borrowing estimate. Remember that a couple of summers ago this announcement shocked markets with unexpectedly large long-term debt auctions. However, since then, the Treasury has managed the process to avoid such surprises.

In Europe, July CPI and preliminary Q2 GDP figures will be released across major economies. Spain’s inflation report comes Wednesday, followed by France, Italy and Germany on Thursday, and the Eurozone on Friday. GDP prints begin with Spain on Tuesday, then Germany, France, Italy and the Eurozone on Wednesday. Labour market data will also be released throughout the week. Tomorrow, the ECB will publish its consumer expectations survey for June.

In Asia, key releases include July PMIs in China on Thursday and Friday, and Japan’s June industrial production, retail sales and July consumer confidence on Thursday. Bloomberg’s median estimates suggest China’s manufacturing PMI will remain unchanged at 49.7, while the non-manufacturing index is expected to dip slightly to 50.3 from 50.5 in June.

Corporate earnings will be intense, with 159 S&P 500 and 113 Stoxx 600 companies reporting. The spotlight will be on Microsoft and Meta (Wednesday), followed by Apple and Amazon (Thursday)—together representing 20% of the S&P 500. Expect plenty of focus on AI capex and monetisation prospects. See the full week ahead in their day-by-day calendar at the end as usual.

In Asia this morning markets are relatively subdued outside of DM futures with the Nikkei (-0.99%) the main decliner. Mainland Chinese stocks are largely flat but with the Hang Seng +0.4% higher and the KOSPI up +0.25%. USTs are flat but 10yr JGBs are -4.3bps lower. S&P (+0.42%) and Nasdaq (+0.57%) futures are higher.

Looking back at last week now, the US reached significant tariff agreements with the Philippines (19%), Indonesia (19%) and Japan (15%). Mr Trump’s deal with Japan was notably lower than expected (15% vs 25%), including a reduced tariff on Japanese automobiles. This helped the Nikkei gain +4.11% over the week, with its best daily performance (+3.51%) since the 90-day extension announced in April. Globally, markets responded positively, buoyed by optimism that more deals would be finalised before August 1. Mr Trump stated on Friday that most deals were done and that “some letters will say 10%, 15% tariff rate.” The S&P 500 rose +0.49% on Friday to a new record high (+1.88% on the week), despite Mr Trump’s comments about limited negotiations with Canada and potential unilateral tariffs.

In Europe, markets started the week lower amid concerns over stalled US-EU negotiations, but sentiment improved as reports suggested a deal centred around a 15% tariff rate was close. The STOXX 600 and FTSE 100 both ended the week up +0.57%, though Germany’s DAX slipped -0.32%.

Elsewhere, ECB President Christine Lagarde struck a surprisingly hawkish tone on Thursday as the ECB held rates steady for the first time this year. This led investors to reassess the likelihood of further cuts, with only 16bps of easing now priced by year-end (-8.1bps on the week). Two-year bund yields rose +7.8bps. On Friday, ECB’s François Villeroy de Galhau said the bank should “remain completely open on future decisions,” and highlighted the euro’s rise, noting its “significant disinflationary effects.” The euro gained +0.82% against sterling, reaching its highest level since late 2023.

Meanwhile, in the US, the Treasury curve flattened sharply amid easing trade concerns, strong data and reduced fears that Mr. Trump might dismiss Fed Chair Powell. Data highlights included the lowest weekly jobless claims since April (217k vs 226 expected) and the strongest composite PMI since December (54.6 vs 52.8). The two-year yield rose +5.4bps on the week, while the ten-year yield fell -2.8bps—marking the steepest flattening of the 2s10s curve since February. On Friday, the ten-year yield dipped -0.8bps as Mr Trump reassured markets he wouldn’t fire Powell, quoting Powell as saying “the country is doing well,” which Mr Trump interpreted as a signal for lower rates. Still, Fed futures continue to price in less than 1bp of easing for this week’s FOMC meeting.

Tyler Durden

Mon, 07/28/2025 – 08:04