US Futures, Global Markets Jump On Tariff Exemptions, Renewed Hopes For Ukraine Ceasefire

US equity futures are – what else – higher, and rapidly approaching a new all time high, boosted by exemptions in Trump’s plans for 100% tariffs on chips that are seen as bullish ways for most big tech firms to avoid levies. The mood was also cheered by a report that Trump and Putin are expected to meet for summit talks in the next few days while

hopes for a rate cut rise some more as additional Fed officials have dovish pivots. As of 8:15am ET, S&P futures are up 0.6% and Nasdaq 100 futures gain 0.7% with Mag7 higher led by AAPL while Semis are the global standout. Eli Lilly & shares plunged after the drugmaker reported underwhelming study results for its weight-loss pill. Shares of its main European rival, Novo Nordisk A/S, soared. Cyclicals are poised to rip, although as JPM notes “today appears to be setting up for an ‘Everything Rally’.” Bond yields are down 1bp across the curve but 10Y is +1bp; USD is flat but has erased ~25bp of overnight losses. Today’s macro data focus is on Jobless Claims, 1Y Inflation Expectations, Nonfarm Productivity, Labor Costs, Consumer Credit, and Inventories. While none, ex-Claims, are market moving it will help sharpen the macro picture on the labor market and consumer. At 12pm, Trump will sign an executive order that aims to allow private equity, real estate, cryptocurrency and other alternative assets in 401(k)s.

{kind=link}

In premarket trading, Mag 7 stocks are all higher (Apple +2%, Nvidia +1.4%, Meta +0.9%, Alphabet +0.6%, Microsoft +0.6%, Tesla +0.5%, Amazon +0.1%)..

Airbnb (ABNB) is down 6% after warning that growth rates may not keep up later this year due to tough year-ago comparisons.

Aris Water Solutions (ARIS), which helps manage water produced from oil drilling, climbs 20% after the company agreed to be bought by Western Midstream Partners in a ~$1.5b equity-and-cash transaction.

Corning (GLW) gains 5% after Apple said it’s planning to onshore 100% of iPhone and Watch cover glass production to the US as part of an expanded $2.5 billion partnership with the high-tech glassmaker.

CRH (CRH) jumps 8% after the building materials company narrowed its full-year adjusted Ebitda guidance to the high end of its prior range.

Crocs (CROX) falls 13% after forecasting that 3Q revenue will be down about 11% to 9%.

DoorDash (DASH) gains 8.9% after the food-delivery company reported second-quarter results that beat expectations and gave a positive forecast for Marketplace gross order value.

Duolingo (DUOL) soars 23% after the language-learning software company reported second-quarter results that beat expectations on key metrics and raised its full-year forecast.

Dutch Bros (BROS) is up 18% after the restaurant chain lifted its total revenue forecast for the full year.

Eli Lilly & Co (LLY) plunges 12% after the company gave disappointing data from a late-stage trial of its new weight-loss pill.

Fortinet (FTNT) tumbles 21% after the software company gave an update to its firewall refresh cycle. At least three analysts downgraded their rating on the stock saying the product refresh cycle is now looking like a “much smaller catalyst than expected.”

Intuitive Machines (LUNR) gains 2% after the space services company said it would buy privately held aerospace company KinetX, expanding its deep-space navigation and flight dynamics capability.

Peloton Interactive Inc. (PTON) gains 12% as the company preached confidence in a turnaround plan under new management.

Sarepta (SRPT) is up 7% after the drugmaker reported second quarter revenue that beat the average analyst estimate.

SharkNinja (SN) rises 5% after the home-appliance maker boosted its adjusted earnings per share forecast for the full year.

Sunrun (RUN) jumps 18% after the solar energy company reported second-quarter revenue that beat the average analyst estimate.

Upwork (UPWK) shares are up 12% after the online recruitment company reported second-quarter results that beat expectations and raised its full-year forecast.

Vistra Corp. (VST) falls 7% after the residential electricity provider operating posted revenue for the second quarter that missed the average analyst estimate.

Market sentiment got a boost earlier after Trump announced that companies producing goods in the US, such as Apple, would be eligible for exemptions from his proposed 100% levy on chip imports. Increasing bets on a Federal Reserve interest-rate cut are also fueling optimism in stocks as sweeping new tariffs to reshape global trade officially took hold Thursday. Ironically the only major US semiconductor stock, Intel, plunged after Trump sa id on Truth Social CEO its has to resign.

“Risk sentiment is positive with a focus on peace deal hopes for Ukraine,” said Bob Savage, head of markets macro strategy at Bank of New York Mellon. “Also supporting the dollar down/stocks up narrative is ongoing September rate cut expectations for the FOMC. However, investors still face a pushback from the uncertainty over tariffs ahead.”

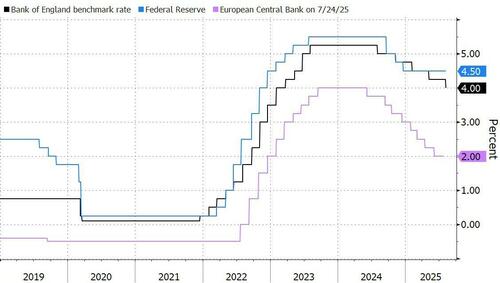

This morning, the BoE delivered a hawkish 25bps cut, with the vote split 5:4 for 25bps vs hold, and the statement noting that timing/extent of further cuts will be based on continued improvements in underlying inflation. The vote was the first ever revote in 28 years after the 4:4:1 vote in the first round failed to reach a majority.

Europe’s Stoxx 600 benchmark advanced more than 1%, with the the travel and leisure sector outperforming. A basket of equities exposed to Ukraine rose, while defense shares dropped, after the Kremlin said that presidents Vladimir Putin and Donald Trump will meet for summit talks within the next few days. Upbeat earnings from some of the region’s biggest companies helped boost sentiment, even after German industrial production suffered its biggest drop in almost a year in another setback for Europe’s largest economy. Here are the biggest movers Thursday:

InterContinental Hotels jumps as much as 9.2%, to the highest level since March, after the company reported that revenue per available room for the first half of the year increased 1.8%. Pretax profit topped the analyst consensus

Maersk gains as much as 6%, the most since May, after the Danish shipping and logistics giant boosted its full-year guidance and beat second-quarter estimates. Analysts say the guidance raise, while somewhat expected, is welcome

Allianz gains as much as 4.3%, the most since April, after the German insurance group posted a strong second-quarter showing, with operating profit coming in ahead of expectations

KBC jumps as much as 6.1%, trading at their highest level since 2007, after the Belgian bank beat expectations in the second quarter and improved its guidance for the full year, which analysts say will lead to consensus upgrades

Harbour Energy shares rise as much as 21%, the steepest gain since December 2023, after the UK oil and gas company boosted guidance for production and cash flow, while announcing announcing a $100m buyback

LINK Mobility gains as much as 9.7% after DNB Carnegie “significantly” raised its estimates for the Norwegian communications technology firm and reiterated its buy rating, while nearly doubling its price target

Serco shares jump as much as 8.8%, to the highest since November 2014, after the outsourcing company reported earnings ahead of expectations and a strong order intake, accompanied by a new £50 million share buyback

European defense stocks slump, while stocks with exposure to Ukraine and Russia gain, as traders take a cue from President Donald Trump’s diplomatic push to end the Ukraine war and US efforts to punish buyers of Russian crude. Rheinmetall shares fall as much as 7.2%, the most in two months, after analysts described the German defense firm’s results as weak. Jefferies points to soft orders and sales below expectations

Carl Zeiss Meditec shares plunge as much as 14% to the lowest since August 2017 after analysts said the German health-care supplier’s 3Q Ebita miss was weighed down by its microsurgery business

Hikma shares drop as much as 10% in London, the most intraday since February, after the pharmaceutical company missed core Ebidta estimates and lowered the margin guidance for its Injectables division for the full year

Freenet shares fall as much as 9.5%, the most since May, after the German-listed mobile communications service provider cut its average revenue per user. Analysts at Berenberg note a marginally disappointing set of results

Deutsche Telekom shares slide as much as 6.1% after the telecom operator reported sales and Ebitda that missed estimates in its home market Germany, with the company flagging intense rivalry in the local broadband market

Siemens shares fall as much as 1.9% after the German industrial company posted what analysts called mixed results, highlighting a weaker performance in the Digital Industries division. Shares are still up almost 16% YTD

Scout24 shares drop as much as 6.1% after the classifieds company reported detailed 2Q results. The shares had gained earlier in the week when the company raised its full-year guidance in a pre-release

Earlier in the session, Asian stocks rose, led by technology stocks as some of the region’s largest chipmakers were expected to win exemptions from Donald Trump’s threatened 100% chip tariff. The MSCI Asia Pacific Index advanced 1%, rising for the fourth straight day. Taiwan’s benchmark rose more than 2%, with notable gains in most other markets around the region. Thailand’s key index was on the brink of entering a bull market. Chipmakers TSMC and Samsung were among the biggest boosts to the MSCI index as investors saw their US manufacturing operations as freeing them from Trump’s newest levies. A gauge of regional tech stocks climbed by the most since June 24. Meanwhile, Indian equities fell after the US moved to double the tariff on imports from the South Asian nation to 50%. The higher rate is seen further hurting sentiment on a market already underperforming Asian peers on disappointing corporate earnings.

In FX, the Bloomberg Dollar Spot Index falls 0.1%. The Antipodean currencies outperform their G-10 peers, rising 0.4% each against the greenback. EUR/USD briefly extended gains on news that Putin and Trump would meet within days, hitting a session high of almost $1.17, before falling back to $1.1648. GBPUSD rose, putting it on track for a fifth day of gains against the dollar, its longest winning streak since April.

In rates, treasuries are steady, with yields broadly within one basis point of Wednesday’s close, despite slide in gilts which sharply underperform following a 4-4-1 Bank of England vote to cut rates by 25bp. US yields steady, marginally cheaper on the day with 10-year near 4.245%, outperforming gilts by around 4bp in the sector. UK 2-year yields higher by around 6bp on the day up to around 3.88% following the announcement. Bunds outperform, pushing German 10-year yields down 2 bps to 2.63%. In the US, focus turns to early data and then a $25 billion 30-year new-issue bond sale at 1pm New York time, which follows a 1.1bp tail on Wednesday’s 10-year note auction.

In commodities, oil prices erase an earlier drop following the Putin-Trump meeting news, with Brent now up 0.5% near $67.22 a barrel. Gold rises $8 to around $3,377/oz.

Looking ahead today, Trump will sign an executive order that aims to allow private equity, real estate, cryptocurrency and other alternative assets in 401(k)s. Data-wise we have 2Q preliminary nonfarm productivity and unit labor costs and weekly jobless claims (8:30am), June final wholesale inventories (10am), July NY Fed 1-year inflation expectations (11am) and June consumer credit (3pm). Fed speakers scheduled include Bostic in a virtual fireside chat on monetary policy (10am)

Market Snapshot

S&P 500 mini +0.6%

Nasdaq 100 mini +0.7%

Russell 2000 mini +0.8%

Stoxx Europe 600 +0.8%

DAX +1.7%

CAC 40 +1.2%

10-year Treasury yield little changed at 4.23%

VIX -0.6 points at 16.13

Bloomberg Dollar Index -0.1% at 1202.97

euro +0.2% at $1.1678

WTI crude +0.6% at $64.73/barrel

Top Overnight News

Trump said, regarding the Fed pick, that the interview process has started and it is probably down to three candidates, while he added that the two Kevins are very good, and a temporary governor is to be named in the next few days.

U.S. trading partners are lobbying the White House for exemptions to sweeping new tariffs that went into force on Thursday, as countries seek ways to muffle the impact on their economies of President Trump’s push to reorder global trade. The diplomatic effort shows months of trade talks are far from over despite the run of agreements trumpeted by the White House in the past month. WSJ

President Trump has claimed that his sweeping tariff regime will reshore American companies and revive manufacturing in the U.S. So far, that hasn’t happened. Economic activity tied to manufacturing has shrunk for most of Trump’s second term. From March to July, U.S. manufacturing activity contracted. The Manufacturing PMI last registered at 48, below the 50 score that differentiates growth and decline. WSJ

The Kremlin said Thursday that a meeting between presidents Donald Trump and Vladimir Putin has been agreed in principle and will happen in the “coming days,” teeing up their first in-person encounter of Trump’s second term. NBC

Trump said he may punish China with additional tariffs over its purchases of Russian oil. Trade adviser Peter Navarro played down the likelihood, saying higher duties “may hurt the US.” BBG

Trump will sign an executive order today that aims to allow private equity, real estate, cryptocurrency and other alternative assets in 401(k)s. BBG

China’s exports grew at a faster clip in July, showing that U.S. tariffs so far haven’t curtailed China’s export machine, although trade with America has fallen. Trade numbers for Jul come in ahead of expectations, including exports (+7.2% vs. the Street +5.6%) and imports (+4.1% vs. the Street -1%). WSJ

Japan cut its growth forecast for the current fiscal year as US tariffs and persistent inflation weigh on the economy. BBG

Caught between rising costs from tariffs and belt-tightening consumers, big retailers are clashing with the producers of consumer brands such as Nivea-maker Beiersdorf and brewer Heineken as they look to avoid sticker shock that could hurt sales. The disputes – which have dented some brands’ sales – underscore the challenge for consumer goods makers and sellers, with inflation and tariffs pushing up input costs and price spikes in commodities such as coffee. RTRS

Fed’s Daly (2027 voter) said there’s cautiousness which is tempering growth but not stalling out, while she commented that they will likely need to adjust policy in the coming months and can’t wait for perfect clarity to act. Daly also commented that tariffs are unlikely to boost inflation persistently in a way that monetary policy would need to offset. She also noted that the labour market has softened and additional slowing would be unwelcome. Furthermore, Daly said they need to recalibrate monetary policy to match risks to the Fed’s goals.

Trade/Tariffs

US President Trump said they are going to be putting a very large tariff on chips and semiconductors, which will be at approximately 100%, but added “if you’re building in the US, there will be no charge.”

US President Trump posted late on Wednesday that “RECIPROCAL TARIFFS TAKE EFFECT AT MIDNIGHT TONIGHT! BILLIONS OF DOLLARS, LARGELY FROM COUNTRIES THAT HAVE TAKEN ADVANTAGE OF THE UNITED STATES FOR MANY YEARS, LAUGHING ALL THE WAY, WILL START FLOWING INTO THE USA.”

US official said the 15% tariff will stack on top of pre-existing tariff rates applied to imports from Japan, unlike in the case of the European Union, according to Kyodo.

South Korea claimed Samsung Electronics (005930 KS) and SK Hynix (000660 KS) will not be subject to 100% US tariffs, while Taiwan said TSMC (2330 TT) is exempt from US President Trump’s 100% chip tariff.

Apple (AAPL) suppliers are reportedly betting on a tariff carve-out for India-made iPhones, according to Nikkei sources.

Maersk (MAERSKB DC): “The effective container-weighted import tariff on US imports is estimated at 24% as per the Presidential Executive Order dated 31 July, up from 5% in 2024”

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed as reciprocal tariffs took effect overnight and following the latest tariff threat from US President Trump who plans to impose ‘approximately 100%’ tariffs on chips and semiconductors unless manufacturers build in the US. ASX 200 pulled back from record highs despite the surprise growth of imports from Australia’s largest trading partner. Nikkei 225 pared initial losses and briefly reclaimed 41,000 amid a busy slate of earnings and as markets shrugged off comments from a US official that the US will not exempt Japan from stacking 15% tariffs on top of existing levies. Hang Seng and Shanghai Comp ultimately kept afloat after the latest Chinese trade data which showed stronger-than-expected exports and surprise growth in the nation’s imports.

Top Asian News

BoK Governor Rhee said the US trade deal takes a huge burden off monetary policy at the August meeting.

SoftBank Group (9984 JT) Q1 2025 (JPY): Net Sales 1.82tln (exp. 1.82tln), Net Income 421.82bln (exp. 158.23bln), sees FY dividend at 44.0 (exp. 44.00)

Baidu (9888 HK) to launch new advanced reasoning model by end of month, according to WSJ.

Magnitude 6.2 earthquake hits sea off Taiwan’s north-eastern coast, according to central weather administration.

Japan Government Official says, a private-sector member of Government Economic Council, says, are worried that the BoJ being behind the curve vs inflation, which is already affecting the livelihood of people.

S&P affirms China’s Sovereign rating at A+/A-; Outlook Stable. Overview: Strong fiscal stimulus will help keep China’s economic growth resilient amid continued headwinds from the weak property sector and new pressures on external trade. “We affirmed our ‘A+’ long-term and ‘A-1’ short-term foreign and local currency sovereign credit ratings on China.” The stable outlook on the long-term rating reflects our view that the Chinese economy will return to self-sustaining growth of above 4% over the next few years, paving the way for smaller annual increases in net general government debt. Downside scenario: “We could lower the ratings if we believe the government will continue with larger fiscal stimulus measures than we currently expect over the next three to five years. This would likely stem from more persistent downward pressure on economic growth than we currently expect. The resulting fiscal impact would cause the net change in general government debt to stay close to, or above, 6% of GDP annually.” Upside scenario: “We may raise our ratings on China if fiscal consolidation is faster than what we anticipate, resulting in a persistent decline in net general government debt to below 30% of GDP, or government interest payments falling below 5% of revenue consistently, or both.”

European bourses (STOXX 600 +0.9%) opened mostly higher, albeit with very modest gains. Since then, indices gradually edged higher, then followed by a more pronounced bid following commentary from a Russian Kremlin aide, who said an agreement had been made for a Presidential meeting between Trump and Putin, in the next few days.

European sectors opened mixed but now hold a slight positive bias. Insurance takes the top spot, lifted by post-earnings strength in the likes of Allianz (+2%) and Zurich Insurance (+1%). Elsewhere, Travel & Leisure has been buoyed by upside in IHG, after it reported strong H1 metrics; European gambling names are also broadly higher today, in tandem with upside in US-peer DraftKings which reported a record rev. and EBITDA. The Tech sector finishes off the top 3, benefiting from a) the risk tone and, b) US President Trump announcing that the US will slap 100% tariffs on imported chips, but will exempt those firms who manufacture in the US/have committed to do so. On this, ASML (+2%) has gained, given the proposition incentivises relocating to the US, which may boost demand for manufacturing units.

Top European News

Germany’s VDA says the EU-US trade deal has brought no clarity or improvement for the German auto industry.

FX

DXY is down for a second day in a row and extending its move below its 200DMA at 98.21. The USD is continuing to be hampered as markets contemplate Trump’s next move with regards to personnel at the Fed. Note, the USD may also be losing ground as geopolitical tensions recede a touch with the Russia and Ukraine conflict potentially nearing a conclusion. Today’s data docket includes weekly claims data, the Atlanta Fed GDPNow Tracked and the NY Fed SCE release. Next downside target for DXY comes via the 29th July low at 97.49.

EUR is a touch firmer vs. the broadly weaker USD in a week that has been lacking in incremental drivers for the Eurozone. Some positivity for the bloc may be gleaned from developments on the geopolitical front following Wednesday’s discussion between the US and Russia, which was said to have made progress and with President Trump intending to meet Russian President Putin as soon as next week. EUR/USD has extended its rise on a 1.16 handle but is yet to crack the 1.17 mark with the pair topping out at 1.1698.

In what has been an indecisive start to the week for USD/JPY, the Yen is eking out mild gains vs. the greenback. This comes in spite of comments from a US official that the now-effective 15% tariff will stack on top of pre-existing tariff rates applied to imports from Japan, unlike in the case of the European Union. USD/JPY delved as low as 146.70 overnight but has since made its way back onto a 147 handle.

GBP is relatively steady vs. the USD as markets brace for the upcoming BoE rate decision, minutes and MPR. Analysts are virtually unanimous in expecting the BoE to lower the Base Rate by 25bps to 4.0% with markets assigning a 93% probability of such an outcome. The move would follow the MPC’s preference for cutting at a quarterly pace and alongside MPR meetings. With regards to the decision to lower rates, consensus looks for a 7-2 outcome. With the likes of Mann and potentially one of Pill or Greene to vote for an unchanged rate. However, when looking at the magnitude of the vote split, this could lead to a three-way split in the event that MPC dove Dhingra and one of Ramsden or Taylor backs a larger 50bps reduction.

Antipodeans are both are building on the gains seen on Wednesday vs. the USD with upside today following on from encouraging Chinese trade data which showed a surprise growth in imports and a larger-than-expected increase in exports.

PBoC set USD/CNY mid-point at 7.1345 vs exp. 7.1709 (Prev. 7.1409)

Fixed Income

USTs are flat and ultimately awaiting today’s risk events which include; jobless claims, unit labour costs, Atlanta Fed GDP Now and then a 30yr auction. As a reminder, the prior day saw a soft 10yr outing after a poor 3yr earlier. No further insight into the potential fat finger in USTs seen on Wednesday in the run-up to supply, where 30 minute volume spiked to over 300k from sub-100k throughout the session to that point. As a reminder, the move also occurred alongside a move in the implied odds (via Polymarket) for the next Fed Chair, with NEC Director Hassett’s jumping by just under bp and overtaking former Fed Governor Warsh as the front-runner. his morning, action (and volumes) has been much more minimal with USTs in a very narrow 112-03+ to 112-07 band.

Bunds are a little lower. No reaction to the morning’s Industrial and Trade data from Germany for June. Though, Bunds did pick up a little bit a handful of minutes after the data came through. The soft set of Industrial data, to the lowest since May 2020, potentially influenced; a series that may have factored into the pressure seen in the DAX 40 future at the time. Since, newsflow has slowed a little but more recently Bunds have edged a little lower back towards lows.

Gilts were flat but more recently some pressure has been seen. The BoE is expected to cut rates and likely via a 7-2 split to ease. However, the full vote breakdown could see a three-way split. Mann and potentially one other (possibly Pill or Greene) likely to vote for unchanged, while Dhingra and possibly the likes of Taylor and/or Ramsden voting for a 50bps cut. Leaving a majority of Bailey, Lombardelli, Breeden and then possibly one or more of Pill, Green, Taylor or Ramsden; depending on the above. Benchmark opened lower by 14 ticks before extending another six to a 92.45 trough. Since, it has reverted back towards Wednesday’s 92.65 close into the BoE.

Spain sells EUR 5bln vs exp. EUR 4.0-5.0bln 2.40% 2028, 3.20% 2035 & 3.45% 2043 Bono and EUR 0.49bln vs exp. EUR 0.25-0.75bln 1.0% 2030 I/L Bono.

France sells EUR 10.499bln vs exp. EUR 8.5-10.5bln 1.25% 2034, 1.25% 2036, 0.50% 2040, and 4.00% 2055 OAT.

Commodities

Crude futures are firmer after choppy trade earlier. This follows the decline on Wednesday amid Russia/Ukraine optimism following the discussion between the US and Russia, which is said to have made progress and with President Trump intending to meet Russian President Putin as soon as next week. Russia’s Kremlin this morning confirmed that US President Trump and his Russian counterpart, Putin, will meet, and preparations for a summit in the next few days are underway. WTI currently resides in a 64.12-65.08/bbl range while Brent sits in a USD 66.70-67.58/bbl range.

Precious metals are rebounding following the prior day’s losses, with spot gold marginally gaining after recent dollar weakness and as reciprocal tariffs took effect. Some pressure seen on the aforementioned Trump-Putin meeting announcement, which saw the yellow-metal swing from highs back towards overnight ranges. Currently in a USD 3,365.30-3,397.58/oz range.

Copper futures are rangebound with a slightly firmer tilt amid the softer dollar, risk appetite in stocks, and the encouraging Chinese trade data overnight, which showed stronger-than-expected exports and surprise growth in the nation’s imports. 3M LME copper prices reside in a USD 9,672.90-9,740.00/t range.

Kuwait’s oil minister expects crude prices to remain above USD 72/bbl; says the market is healthy with moderate demand growth.

Geopolitics: Ukraine

Kremlin Aide Ushakov says an agreement has been reached to hold a meeting with US President Trump and Russian President Putin in the next few days. Meeting venue has been agreed and will be announced later. US Envoy Witkoff touched on an idea of a three-way meeting between Trump-Zelensky-Putin; Moscow left it without comment.

US President Trump said they had very good talks with Russian President Putin and there’s a good chance that there will be a meeting very soon, while he also commented that more secondary sanctions are coming regarding Russia.

US Secretary of State Rubio said it was a good day regarding efforts to end the Ukraine war but there is still a lot of work ahead and many impediments to overcome.

Ukrainian President Zelensky said he discussed Witkoff’s visit to Moscow in a call with Trump and said that Russia should end this war, while he also commented that pressure on Russia is working and it’s crucial they do not deceive them, as well as commented that it looks like Russia is more inclined to a ceasefire.

Ukrainian President Zelensky calls on Russian President Putin to hold meeting to ‘end war’, via Al Arabiya.

Geopolitics: Other

South Korean military said South Korea and the US are to conduct major joint military exercises beginning on August 18th although an official stated that some parts of the joint drills are postponed to September, while the military drills will test an upgraded response to a heightened North Korea nuclear threat.

US Event Calendar

:30 am: 2Q P Nonfarm Productivity, est. 2%, prior -1.5%

8:30 am: 2Q P Unit Labor Costs, est. 1.5%, prior 6.6%

8:30 am: Aug 2 Initial Jobless Claims, est. 222k, prior 218k

8:30 am: Jul 26 Continuing Claims, est. 1950k, prior 1946k

10:00 am: Jun F Wholesale Inventories MoM, est. 0.2%, prior 0.2%

3:00 pm: Jun Consumer Credit, est. 7.5b, prior 5.1b

Central Bank Speakers

10:00 am: Fed’s Bostic Speaks on Monetary Policy

DB’s Jim Reid concludes the overnight wrap

Tech stocks have continued to drive a buoyant mood in markets, with the Mag-7 (+1.93%) reaching a new all-time high. Momentum was also supported by strong earnings and rising hopes of imminent rate cuts as Fed speakers turned more dovish in response to last Friday’s weak payroll print. The upbeat tone has continued overnight despite Trump outlining a plan for 100% tariffs on semiconductors, with the impact of these mitigated by carveouts.

US equity markets had a strong day yesterday with S&P 500 (+0.73%) and Nasdaq (+1.21%) closing less than 1% from record highs, while the Mag-7 (+1.93%) was lifted by a +5.09% spike in Apple’s shares. That came as the company announced additional $100bn of investments into the US, particularly in new manufacturing. This comes on top of an earlier pledge of $500bn investment over four years and as the company has sought to reduce tariff risks. During a White House event with Apple CEO Tim Cook, Trump then said that “we’ll be putting a tariff of approximately 100% on chips and semiconductors”. However, he added that companies that are building, or “have committed to build”, capacity to move production to the US would face no charge. Imports of electronics have so far been exempt from tariffs.

While it’s not clear exactly how it will work, the new floated exemption has added a sense of relief for markets overnight, with Taiwan’s chip giant TSMC up +4.44% and Korea’s Samsung +1.74%. In terms of the major indices, the Nikkei (+0.68%) and the KOSPI (+0.72%) are visibly higher, while the Hang Seng (+0.52%) and the Shanghai Composite (+0.12%) are seeing more modest gains. Futures on both the S&P 500 (+0.27%) and the NASDAQ (+0.31%) are also higher overnight.

The other major tariff news yesterday was a new US executive order outlining an additional 25% tariff on India in response to its purchases of Russian oil, which would bring the total levies on Indian exports to 50%. India’s government called the latest tariffs “unfair, unjustified and unreasonable”. The executive order also leaves the door open for tariffs on other countries “directly or indirectly importing Russian Federation oil”. Trump said there could be “a lot more” secondary sanctions related to Russian oil, including potentially on China, but that this would depend on how talks proceed. Brent crude fell for a fifth consecutive session (-1.11% to $66.89/bbl) yesterday, the longest such run since May, though it is up +0.8% this morning. In addition to India being the only target so far, the sanguine oil reaction came as the additional 25% tariffs will kick in only after 21 days, leaving ample time for negotiations.

Later in the day we heard that Trump could meet Russia’s President Putin as soon as next week, with reports citing a call that Trump had with European leaders after his envoy Steve Witkoff met with Putin in Moscow. Trump himself said there was a “very good chance” he would meet soon with Putin and Ukraine’s President Zelenskiy to try and broker peace, though he was more ambiguous on the likely timing. Secretary of State Rubio said that “a lot has to happen” before Trump meets with Putin.

In the latest news on the Fed’s leadership, Trump said he will likely nominate a temporary Fed governor after Kugler’s departure on August 8, adding that the decision would come “over the next two, three days” and that there were “probably” three candidates for the role. A temporary replacement for the remainder of Kugler’s term until January would avoid the person being seen as a likely candidate for Fed Chair once Powell’s term ends in May.

Meanwhile, Fed officials on Wednesday struck a more dovish tone in response to Friday’s soft jobs report. Fed Governor Cook said the report was concerning, with significant downward revisions “somewhat typical of turning points” in the economy. Minneapolis Fed President Kashkari suggested that in case of a slowdown in the economy, a cut might be appropriate “in the near term”, whileSan Francisco President Daly said “we will likely need to adjust policy in the coming months” as additional labour market slowing was “unwelcome”. Pricing of a September Fed rate cut ticked up from 90% to 95% amid the shifting rhetoric, with 60bps of cuts priced by the December meeting (+2.0bps on the day).

In turn, 2yr Treasuries rallied by -1.0bps, but yields moved higher at the long end, with the 10yr up +1.5bps to 4.23%, and 30yr up +3.8bps to 4.82%. That came amid a soft 10yr auction that saw $42bn of bonds issued +1.1bps above the pre-sale yield, with the bid-to-cover ratio at its lowest level in 12 months. 10yr yields are another +1.5bps higher overnight.

Increased rate cut expectations saw the dollar index (-0.61%) fall to its lowest level in nearly two weeks. Meanwhile, the Swiss franc has been the worst performing G10 currency this week as Switzerland’s President Karin Keller-Sutter left Washington yesterday without securing any easing of the 39% US tariffs that came into force along with other new country rates overnight.

Back to yesterday’s equity moves, there was some softness beneath the headline gains with more than half of the S&P 500 constituents lower on the day, led by a decline in healthcare stocks (-1.52%). The Philadelphia semiconductor index (-0.20%) underperformed following underwhelming results from AMD (-6.42%) and Super Micro Computer (-18.29%). Other notable post-earnings movers included McDonald’s (+2.98%), whose same store sales grew more strongly (3.8% yoy vs. +2.6% expected), and Walt Disney (-2.66%), which saw profit guidance weighed down by its movie and TV businesses. Over in Europe, the Stoxx 600 (-0.06%) was again dragged down by another decline for Novo Nordisk (-5.36%) as it released its latest earnings. The pharma giant’s shares are now down -36% since its profit warning last Tuesday. However, most European indices gained with the DAX (+0.33%), CAC (+0.18%), FTSEMIB (+0.65%) and FTSE 100 (+0.24%) all in the green. In one of the more unusual stories, pharma conglomerate Bayer AG (-9.92%) was the worst performer in Stoxx 600 in part as it revealed that its earnings had been recently inflated by football player transfer receipts stemming from its ownership of Bayer Leverkusen. I will let Jim opine on whether Liverpool’s club record signing of Florian Wirtz in June which boosted Bayer’s bottom line was a good deal.

European government bonds saw a modest sell off on Wednesday, with yields on 10yr bunds (+2.7bps), OATs (+2.7bps) and BTPs (+2.1bps) all higher. Pricing of ECB rate cuts ticked lower, with amount of easing priced by year-end down -1.3bps to 15bps as outgoing Austria central bank governor Holzmann said he saw no reason for another rate cut.

Staying with central banks, today the Bank of England is expected to deliver a 25bp rate cut to 4.00%, which would mark the fifth cut in the BoE’s gradual easing cycle. Our UK economist Sanjay Raja expects divisions on the committee, foreseeing a 2-5-2 vote across no change, -25bp and -50bp options. You can see Sanjay’s full preview here.

Turning to the data, yesterday was quiet in the US but investors will be dissecting today’s jobless claims for whether evidence of US labour market deterioration is visible outside of payrolls. In Europe, June factory orders in Germany surprised to the downside at -1.0% mom (vs. +1.1% expected), with components such as transport equipment (-23%), autos (-7.6%) and fabricated metal products (-13%) slumping. The moves suggest a drag from tariffs with foreign orders weighing while domestic orders rose by almost 4%. On a more positive note, euro area retail sales pointed to a resilient consumer, rising by an expected +0.3% mom in June but with the yoy reading at a stronger +3.1% thanks to revisions (+2.6% expected).

In goods trade data out of China this morning, both exports (+7.2% yoy vs +5.6% exp.) and imports (+4.1% vs -1.0% exp.) grew more strongly than expected in July. So suggesting a resilient aggregate trade performance of the world’s primary manufacturing hub, even as China’s exports to the US fell by -22% yoy.

To the day ahead, the main highlight in Europe will be the Bank of England’s latest policy decision, along with the subsequent press conference with Governor Bailey. In terms of data, we’ll have the initial and continuing jobless claims out in the US, while in Germany the highlight is June industrial production. Looking at earnings, the focus will be on Eli Lilly and Toyota

Tyler Durden

Thu, 08/07/2025 – 08:30