US Producer Prices Cooler Than Expected In March Despite Surge In Energy Costs

The month-over-month change in producer prices had accelerated for five straight months ahead of today’s March data, which is expected to surge thanks to Iran-war impacts on energy costs.

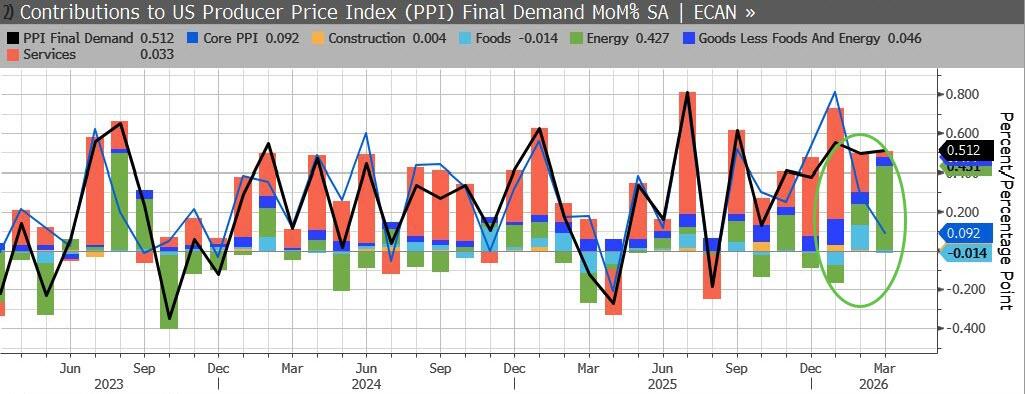

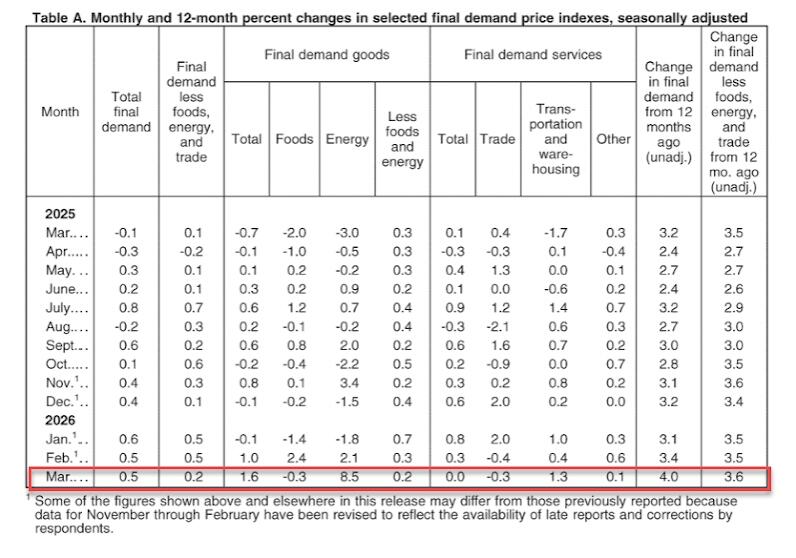

Against expectations of a 1.1% MoM rise, March’s Headline PPI shocked everyone by rising only 0.5% MoM (equal to the revised lower 0.5% MoM rise in both of the last two months). This pushed PPI up 4.0% YoY (the highest since Feb 2023) but well below the +4.6% YoY exp…

{kind=link}

Source: Bloomberg

Energy dominated the increase…

{kind=link}

But the Energy PPI index appears to have ‘underperformed’ relative to oil…

{kind=link}

Source: Bloomberg

PPI Final demand goods: The index for final demand goods increased 1.6%, the largest rise since August 2023. Most of the March advance can be traced to prices for final demand energy, which jumped 8.5%. The index for final demand goods less foods and energy increased 0.2% In contrast, prices for final demand foods declined 0.3 percent.

Product detail: Nearly half of the March advance in the index for final demand goods is attributable to a 15.7% rise in gasoline prices. The indexes for diesel fuel, jet fuel, home heating oil, meats, and primary basic organic chemicals also increased. Conversely, prices for fresh and dry vegetables fell 10.7%. The indexes for natural gas and for carbon steel scrap also decreased.

PPI Final demand services: The index for final demand services was unchanged in March following a 0.3% advance in February. In March, price increases of 1.3% for final demand transportation and warehousing services and 0.1% for final demand services less trade, transportation, and warehousing offset a 0.3% decline in margins for final demand trade services.

Product detail: Within final demand services in March, prices for airline passenger services rose 2.8%. The indexes for food retailing; apparel, jewelry, footwear, and accessories retailing; outpatient care (partial); and truck transportation of freight also moved higher. In contrast, margins for food and alcohol wholesaling fell 6.0%. The indexes for fuels and lubricants retailing; securities brokerage, dealing, and investment advice; deposit services (partial); and brokerage fees and commissions for residential property agreements also decreased.

{kind=link}

However, in a similar manner to CPI, we see Core Producer prices (ex-food-and-energy) rising just 0.1% MoM (dramatically cooler than +0.4% MoM exp). This pulled the Core PPI YoY down from +3.9% to +3.8%…

{kind=link}

Source: Bloomberg

So that’s all ‘good news’.

Here’s the bad news… the pipeline for inflation is accelerating significantly…

{kind=link}

Source: Bloomberg

It seems the panic over energy fears sparking massive inflation (in March) was overdone (again).

For now, the market continues to price in a higher chance of a rate-cut next than rate-hike.

Tyler Durden

Tue, 04/14/2026 – 08:40