Walmart Inc. (NYSE: WMT) has sustained its growth momentum this year despite cautious consumer spending and cost headwinds. The retail behemoth’s ability to successfully navigate through market headwinds and economic uncertainties differentiates it from others. When it reports second-quarter results next week, investors will look for updates on demand trends and the company’s growth strategy.

Q2 Report Due

In a recent statement, the Walmart leadership said it expects sales to grow 3.5-4.5% year-over-year in the second quarter, in constant currency. Analysts’ consensus revenue estimate for Q2 is $174.21 billion, representing a 3.8% year-over-year increase. They are looking for earnings of $0.74 per share, adjusted for one-off items, compared to $0.67 per share in Q2 2025. The report is expected to be out on Thursday, August 21, at 7:00 am ET.

Market sentiment toward Walmart is strongly bullish this week, with analysts across the board recommending a buy. The consensus target price suggests a potential upside of over 10% from the last closing price, signaling confidence in the retailer’s near-term growth trajectory. After pulling back from its February peak, the stock has been trending upward in the past few months, outperforming the broader market. The value has grown nearly 50% in the past twelve months.

Q1 Outcome

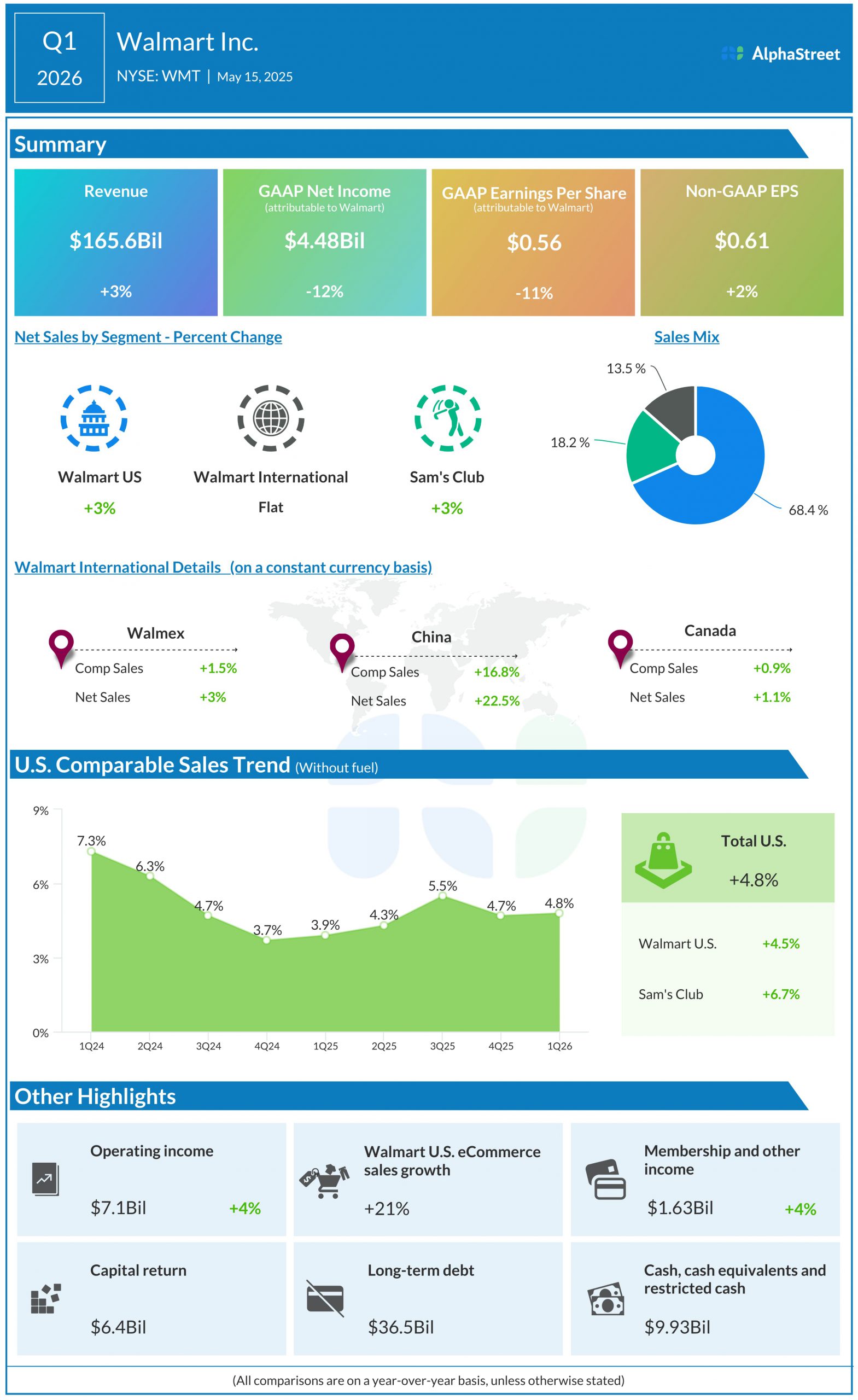

In the first three months of fiscal 2026, Walmart’s revenue rose 2.5% year-over-year to $165.6 billion — up 4% in constant currency. The growth was driven by continued strong sales at Walmart US, which accounts for nearly 70% of the total business. Sales grew in China and Canada, where the company has a significant presence.

Total US comparable sales, excluding fuel, moved up 4.8%. At $0.61 per share, adjusted earnings were up 1.7%. Both earnings and the top line beat analysts’ expectations. Meanwhile, unadjusted net income declined around 12% to $4.48 billion or $0.56 in Q2.

“As we continue to diversify our profit streams through our eCommerce offering, our marketplace, membership, and advertising, we have some room to absorb costs. We’re committed to growing profit faster than sales. There isn’t anything about this quarter or anything about this coming year that shakes our confidence about growing profit faster than sales over the term of our long-range plan. The strategy and business model are set up to do that,” Walmart’s CEO, Douglas McMillon, said during his post-earnings interaction with analysts.

Road Ahead

The company has consistently outperformed quarterly earnings and sales estimates over the years, demonstrating a strong track record of execution. For fiscal 2026, it forecasts a 3-4% increase in net sales, in constant currency. Full-year adjusted income is expected to range between $2.50 per share and $2.60 per share.

Currently, the main challenge facing Walmart is the impact of new import tariffs, particularly on China, considering its heavy reliance on goods imported from that country. The situation demands effective measures to strike the right inventory balance and keep prices low to remain competitive.

The average price of Walmart’s stock for the last 52 weeks is $90.79, and its all-time high closing price was $104.51 in February this year. On Wednesday, the shares traded mostly lower during the regular session.

The post Walmart likely to post strong Q2 results amid e-commerce, membership growth first appeared on AlphaStreet.