Shares of The Wendy’s Company (Nasdaq: WEN) fell 6.5% to $6.80 in Friday afternoon trading as the fast-food chain’s disappointing 2026 financial guidance overshadowed a slight beat in fourth-quarter earnings.

The stock is currently trading near its 52-week low of $6.75, having declined approximately 46% over the past year. The recent downward trend accelerated following the company’s announcement of a “rebuilding year” and a system optimization plan that includes closing hundreds of underperforming domestic locations.

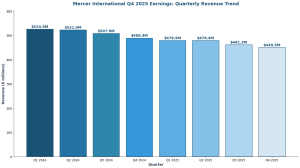

Quarterly and Full-year Results

For the fourth quarter ended Dec. 28, 2025, Wendy’s reported total revenues of $543.0 million, a 5.5% decrease from $574.3 million in the prior-year period. Despite the decline, revenue narrowly exceeded the analyst consensus of $537.6 million.

Fourth-quarter adjusted earnings per share (EPS) came in at $0.16, down 36% from $0.25 a year ago but ahead of the $0.15 expected by Wall Street. Global systemwide sales dropped 8.3% to $3.4 billion, driven largely by a 11.3% plunge in U.S. same-restaurant sales.

Operating profit for the quarter fell 33.3% to $64.0 million, while adjusted EBITDA declined 17.6% to $113.3 million. U.S. company-operated restaurant margins contracted by 380 basis points to 12.7%, pressured by lower customer traffic, commodity inflation—specifically beef prices—and higher labor costs.

For the full year 2025, total revenues fell 3.1% to $2.18 billion. Full-year net income dropped 15.1% to $165.1 million, with adjusted EPS of $0.88 compared to $1.00 in 2024.

2026 Outlook and Strategy Shift

The company issued 2026 guidance that fell significantly short of market expectations. Wendy’s projects 2026 adjusted EPS between $0.56 and $0.60, well below the analyst estimate of $0.85. Global systemwide sales growth is expected to be approximately flat.

Interim CEO Ken Cook detailed “Project Fresh,” a turnaround plan focused on brand revitalization and system optimization. As part of this strategy, Wendy’s plans to close 5% to 6% of its U.S. restaurant base—roughly 300 to 360 locations—in the first half of 2026 to improve average unit volumes and franchisee economics.

International operations remained a rare bright spot, with systemwide sales growing 6.2% in the fourth quarter and 8.1% for the full year. The company added 121 net new international restaurants in 2025.

Sector Context

The results reflect broader macro pressures facing the Quick Service Restaurant (QSR) sector. While not a software or SaaS entity, Wendy’s faces similar headwinds to consumer-facing platforms, including decreased discretionary spending among lower-income households and intense price competition. Rival McDonald’s (NYSE: MCD) also recently noted a more cautious consumer environment, though it has maintained higher operating margins through superior scale.

Wendy’s returned $329.6 million to shareholders in 2025 and ended the year with $340 million in cash and a net leverage ratio of 4.8x.

The post Wendy’s shares tumble on weak 2026 outlook, U.S. sales slump first appeared on AlphaStreet News.